Being financially independent means having enough passive income to cover your essential or desired living expenses. A common guideline is to aim for a net worth equal to 25 times your annual expenses, often used as a baseline for achieving financial independence. However, this approach is overly simplistic because it depends on the composition and liquidity of one’s net worth.

If your net worth consists entirely of liquid, income-producing assets, 25 times your expenses should suffice. But if much of it is tied up in a primary residence or illiquid private investments, you may not be able to generate enough passive income or readily sell assets for true financial independence. Liquidity and cash flow are paramount for retirement.

For those retiring at the traditional age of 65, a net worth of 25X your annual expenses, supplemented by Social Security, is usually sufficient for a comfortable retirement. However, the 25X rule becomes more precarious for those seeking early retirement. The multiple should be a target for your liquid, income-producing assets, not your net worth. And your liquid portion of your net worth needs to generate income.

Longer time horizons, inflation, and lifestyle changes—like growing families—can quickly erode a seemingly adequate net worth.

Couldn't Stay Fully Retired For Long On 25X Expenses

When I revisited my finances after a 2013 financial consultation, I was reminded of the limitations of the 25X rule for achieving FIRE (Financial Independence, Retire Early).

Although I retired in 2012 at age 34 with a net worth of roughly 38 times my annual expenses, I couldn’t sustain full retirement beyond 18 months. The challenge lay in the composition of my net worth—much of it tied up in my primary residence—and the rising costs of maintaining a growing household. These factors made early retirement far more complex than I had initially anticipated.

My original plan was to embrace a simpler life with my wife on my grandparents' farm in Waianae, Oahu. The vision was idyllic: we’d source most of our food from the land and live comfortably on $80,000 a year. However, detaching ourselves from San Francisco, a city we’ve called home since 2001, proved difficult. Life pulled us in a different direction.

Our journey took an even bigger turn with the births of our children in 2017 and 2019, further anchoring us to San Francisco. The vision of a quiet life on the farm shifted to balancing the demands of raising a family in one of the most expensive cities in the world. Early retirement, it turned out, required more than a high net worth—it demanded greater cash flow and a willingness to adapt to life’s unexpected turns.

Diversify Into Real Estate

If you want to build greater wealth that's less volatile and generates more income, diversify into real estate. The combination of property price appreciation and rental income growth is a powerful wealth creator. Invest 100% passively in real estate through Fundrise, with an investment minimum of only $10. I’ve personally invested over $270,000 in Fundrise so far.

Why A Net Worth Equal To 25X Annual Expenses Is Not Enough To Retire Early

Today, our net worth is even greater than the 38X expenses we had in 2012. Yet, I don't feel financially independent because our passive income doesn't fully cover our current living expenses. I subscribe to the legacy retirement philosophy of leaving some wealth to my children and charities versus dying with nothing.

We had exchanged a large amount of productive investments generating passive income for a home that, although paid off, requires ongoing expenses such as property taxes, maintenance, and utilities—costs that stocks and bonds don’t have.

My goal now is to recoup the productive investments we allocated to our home over the next three years.

Rollover IRA as a Case Study on Net Worth Composition

Let’s take my rollover IRA as a simple example of why 25X annual expenses falls short as a retirement net worth target. 25X is the inverse of 4%, the safe withdrawal rate popularized in the 1990s by Bill Bengen, creator of the 4% Rule.

Imagine my IRA were my only asset, with a balance of $1,300,000. This means that my entire net worth consists of my rollover IRA, a 100% productive, income-producing asset.

Coincidentally, according to a Northwestern Mutual survey from late 2023, this amount aligns with what Americans believe they need to retire comfortably. Let’s assume I live off $40,000 a year in expenses. If we multiply $40,000 by 25, that equals $1,000,000, suggesting I could be financially independent.

However, due to the type of investments in my portfolio, it doesn't come close to providing enough dividend income to live on.

Low Passive Income Due to a Growth-Focused Portfolio

Ninety percent of my Equities – $826,191- is allocated to growth stocks. Microsoft offers the highest dividend yield in this category at about 0.78%, followed by Apple at 0.48%. This brings my average dividend yield across all my growth stock holdings to around 0.2%, resulting in just $1,653 in dividends annually.

The bulk of my ETF holdings – $476,000 – is in VTI, the Vanguard Total Stock Market Index, which has a dividend yield of roughly 1.33%. Consequently, my blended yield for the entire portfolio is around 0.6%, translating to about $7,800 in annual passive income.

With post-tax annual expenses at $40,000, I’d need a portfolio approximately 6.4 times larger—$8,320,000—to generate $50,000 in gross passive income to cover expenses after taxes.

It may seem excessive to need an $8,320,000 portfolio to achieve financial independence with annual expenses of $40,000. And it is. However, few people hold their entire net worth in liquid, income-generating assets. For many, their equity is not as readily accessible as it might appear.

Adjusting Your Net Worth Composition Isn’t Always Easy

Astute readers may suggest that the straightforward way to achieve financial independence on a $1,300,000 net worth is to adjust the investment composition: sell enough growth stocks and purchase enough dividend stocks or ETFs to generate $50,000 a year, which would require a 3.8% dividend yield.

To do this, I would have to rebalance the majority of my portfolio. If my retirement portfolio was in a taxable brokerage account, I would incur significant capital gains tax.

Thus, a rational investor is unlikely to sell stocks they are positive on unless absolutely necessary. Instead, they would continue working or find supplemental retirement income to support their lifestyle. Any surplus cash flow could be directed toward dividend-paying stocks or ETFs over time.

The Benefit Of A Roth IRA For Early Retirees

Fortunately for Roth IRA holders, investments can be traded within these accounts without triggering capital gains taxes. This allows for adjustments without an immediate tax bill, offering more flexibility for portfolio restructuring. Hence, for those who can build a large enough Roth IRA for retirement, the flexibility in repositioning your portfolio without tax consequences can be a great benefit.

For those who wish to retire before 59.5, you can always withdraw your original contributions tax- and penalty-free, regardless of your age or how long the account has been open. Since contributions are made with after-tax dollars, they’re not subject to penalties or taxes. After 59.5, you can then withdraw earnings tax- and penalty-free, provided your Roth IRA has been open for at least five years.

For those planning to retire early, the process requires meticulous planning. After years of following a particular investment strategy, you’ll need to adjust the composition of your portfolio to align with your new financial needs. On top of that, you’ll face the challenge of transitioning from accumulation to withdrawal, starting with tapping into your contributions. This shift is easier said than done and requires a clear strategy to avoid unnecessary taxes, penalties, or liquidity issues.

Housing Is A High Percentage Of Net Worth

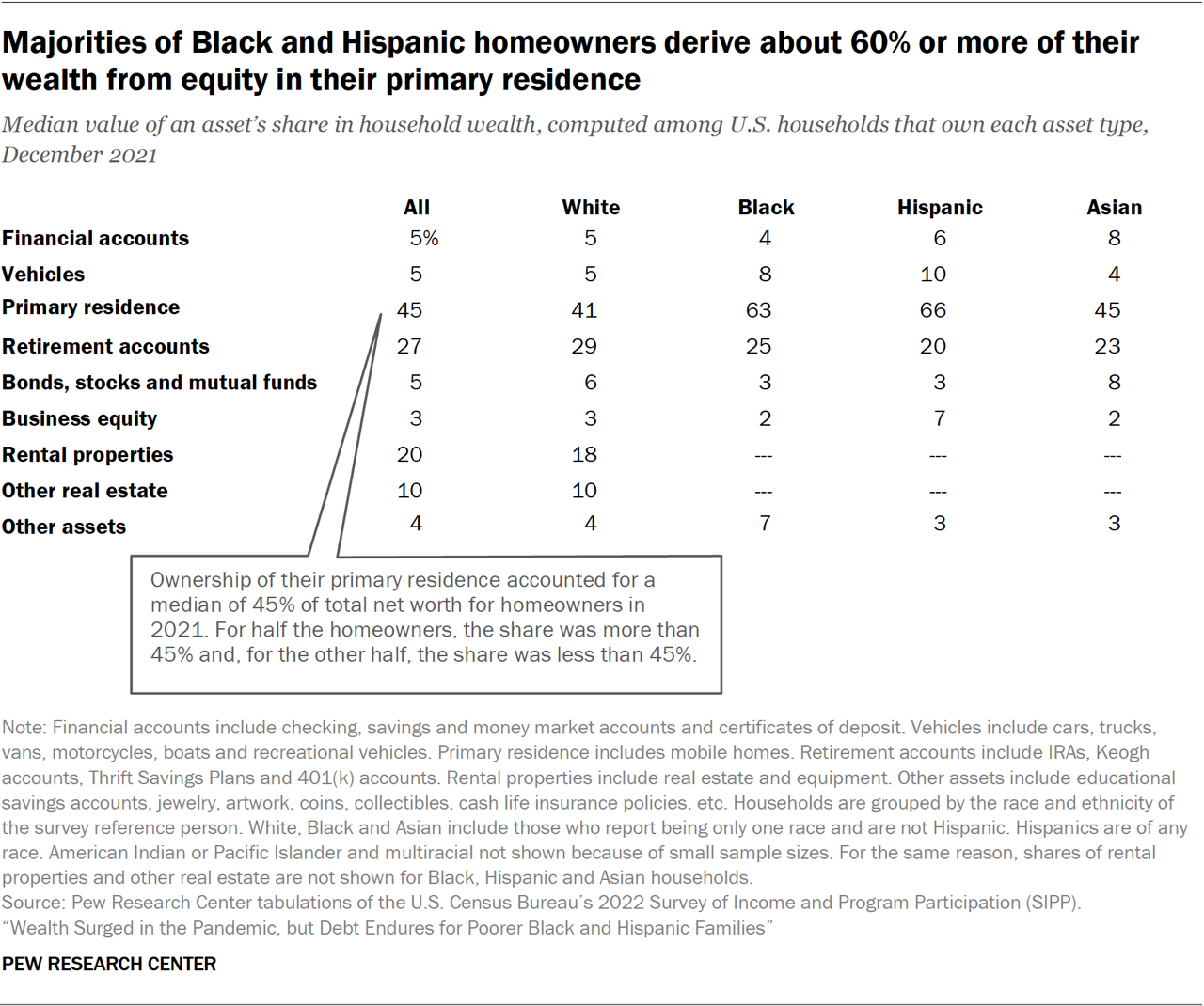

Another reason why a net worth of 25X annual expenses may not be sufficient to retire early is the high percentage of net worth tied up in housing. According to Pew Research, in 2021, the median net worth of U.S. households stood at $166,900, including all assets, with home equity accounting for a median of 45% of this net worth. The percentage is likely similar today.

However, when examining Pew’s article, they state, “In 2021, homeowners typically had $174,000 in equity in their homes,” alongside the national median net worth figure of $166,900. This discrepancy suggests home equity may represent an even larger share of net worth for many households. Many American homeowners got crushed during the global financial crisis due to real estate concentration risk.

Assuming 45% of one's net worth is in their primary residence is accurate, that still leaves the typical household with only 55% of their net worth in other assets, such as vehicles, financial accounts, retirement funds, business equity, rental properties, and other real estate.

Taxable Brokerage Accounts: A Small Slice of Net Worth

Within this remaining 55%, Financial accounts—which I interpret as taxable brokerage accounts—make up a modest 5% for all races surveyed. These are the assets that can be tapped before 59.5 without penalty. Clearly, these accounts alone aren't enough to sustain early retirement for most.

Interestingly, Pew’s data reveals that for White households, rental properties and other real estate represent 30% of total net worth, indicating that many White Americans generate rental income as landlords.

Perhaps Pew’s survey sample didn’t capture sufficient data from Black, Hispanic, and Asian households to reflect their ownership of rental properties and other real estate. Yet, real estate is a favored asset class for many Asians, including myself.

But is a combined 5% in financial accounts plus 30% in rental properties and other real estate sufficient to generate livable passive income for early retirement? Realistically, it’s highly unlikely.

So let's be generous. Let's assume the entire 55% of net worth is 100% allocated to productive income-generating assets like stocks and real estate. Further, there is no penalty to sell any of these assets. What would the more realistic net worth target based on annual expenses be?

45.5X Annual Expenses May Be A More Reasonable Net Worth Target For The Typical Household

Applying some basic math, with only 55% of the typical American household’s net worth outside of their primary residence, the typical household would need a net worth equal to 45.5X annual expenses to achieve early retirement.

I can already hear the complaints from readers saying that a 45.5X annual expenses target is both unrealistic and demoralizing. But if the data about the typical net worth composition of Americans is accurate, then this target is grounded in simple math.

To understand why, imagine if 100% of your net worth were tied up in your primary residence. Every room is occupied, and you can’t rent out any part of the house for income. How would you fund your retirement with such a net worth composition? Even if your home were worth 100X your annual expenses, it wouldn’t help you cover your living costs unless you took out a Home Equity Line of Credit (HELOC), did a cash-out refinance, or conducted a reverse mortgage.

In early retirement, you need to rely on passive income or liquidating assets to cover your expenses. In traditional retirement, Social Security benefits and pensions provide additional support, reducing the reliance on these strategies.

Letting Go of a Strict Definition of Financial Independence

A final approach to the 25X annual expenses debate on whether it is enough is to let go of a rigid definition of FIRE: your investments generate enough income to cover your living expenses. Instead, build a net worth of at least 25X your annual expenses and simply withdraw at a 4% (or potentially higher) rate, regardless of what anybody thinks.

Bill Bengen’s 4% rule, established in his 1994 study, assumes retirement at age 65. Bengen found that retirees beginning at this age could safely withdraw 4% of their retirement portfolio in the first year, then adjust annually for inflation, expecting the portfolio to last for at least 30 years—until age 95—without running out.

If you plan to retire at 65, you could confidently withdraw at a 4% rate or even a 5% rate, as Bill now suggests. Lowering the traditional retirement age to 55 for society might even be possible if workers only need to accumulate 20X their annual expenses (inverse of 5%).

However, if you want your wealth to endure for generations after you retire early, consider lowering your safe withdrawal rate to ensure the sustainability of your financial legacy. You can also generate supplemental retirement income.

Formula to Calculate Your True Annual Expense Multiple Needed to Retire Early

To determine the true multiple of your annual expenses needed to retire early, you’ll need to assess two key factors:

- The minimum annual expense multiple you believe is necessary for early retirement. 25X can be a baseline.

- The percentage of your net worth held in income-producing, liquid investments.

Here’s how it works:

Let’s assume you believe that a net worth of 25X your annual expenses, the inverse of 4%, is sufficient for early retirement. However, only 70% of your net worth is in income-producing, liquid investments. To adjust for this, you can use the following formula:

True Annual Expense Multiple = Baseline Annual Expense Multiple ÷ Percentage of Net Worth in Income-Producing, Liquid Investments

For this example:

True Annual Expense Multiple = 25 ÷ 0.7 = 35.7

If 70% of your net worth is in income-producing, liquid assets, you would need a net worth of 35.7 times your annual expenses to achieve the same financial security as someone with 100% of their net worth in such assets.

This is because the 30% of non-liquid, non-income-producing assets won't contribute directly to generating income for expenses, so you need a higher overall net worth to compensate. Of course, as you change your net worth composition, you can re-calculate your true annual expense multiple for early retirement.

Focus on Building Net Worth First, Then Cash Flow

If you want to retire earlier, logically, you must find a way to achieve a net worth target equal to your true annual expense multiple sooner. This usually requires working longer, saving more, and taking on more risk. It may also mean forsaking homeownership to boost your liquid percentage.

Further, the government taxes income more heavily than investment gains, making it more advantageous to prioritize growing your net worth over generating cash flow in the early stages of your financial journey. While there’s ongoing debate about a potential wealth tax, it’s unlikely to become a reality anytime soon.

Only when you’re ready to stop working entirely, or your active income sources significantly dwindle, should generating passive income take center stage.

In our unusual case, my wife and I don’t have traditional jobs, yet we remain aggressive investors. Financial Samurai, our “X Factor,” provides supplemental income that we didn’t fully anticipate when we left our corporate roles in 2012 and 2015. This additional income has allowed us to take on more investment risk, such as focusing on growth stocks and allocating capital to venture funds for private market exposure.

As we’ve increased our investments in illiquid assets, the trade-off has been slower passive income growth. One day, Financial Samurai will come to an end, and when that time arrives, we’ll pivot to prioritize liquidity and income-generating investments.

Don't Take The 25X Multiple For Financial Independence At Face Value

Just as focusing solely on revenue instead of profit can mislead in evaluating a business, so can assuming that 25X annual expenses is all one needs for financial independence. Many people have net worth tied up in homes, growth stocks, private companies, commodities, or collectibles that don’t generate income.

Based on my early retirement experience and that of countless others pursuing FIRE since 2009, a net worth equal to 25X expenses is often not enough. You’ll likely find yourself still working or seeking new income sources once you achieve this financial milestone. You may even crack the whip on your spouse to continue working as you kick back!

To feel genuinely free, consider aiming for 50X expenses or 20X your average gross income over the last three years. Better yet, do the simple math to find your unique multiple as I proposed in my formula above. While these net worth targets may seem ambitious, don’t underestimate the power of compound returns and disciplined saving.

If you don’t reach these multiples, that’s okay too. Many people continue to earn active income to fund their lifestyle goals. But now, I'm even more emboldened by my net worth targets due to national data from Pew Research and my logical formula.

Readers, do you think a net worth equal to 25X your annual expenses is enough to retire early on? Have you ever met someone who did retire early on 25X expenses and doesn't generate any active income?

Use The Best Retirement Planner: Boldin

If you’re serious about building wealth and retiring comfortably, sign up for Boldin’s powerful retirement planning tools. They offer a free version and a PlannerPlus version for just $120/year—far more affordable than hiring a financial advisor.

Boldin was designed specifically for retirement planning, offering a holistic approach to financial management. Beyond just focusing on your stock and bond portfolio, Boldin integrates real estate investments, guides you through Roth conversions for tax minimization, and addresses many other real-life financial scenarios we all face.

There's no more powerful retirement planning tool to help you finish rich than Boldin today.

Diversify Into High-Quality Private Real Estate

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential. Real estate along with negotiating a severance package were my main reasons for being able to retire early.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

I’ve personally invested over $270,000 with Fundrise, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

Join 60,000+ others and subscribe to my free weekly newsletter here. Financial Samurai was founded in 2009 and is the leading personal finance website today. Everything is written based off firsthand experience as money is too important to be left up to pontification.

Sam,

As always thanks for a great weekly informative email; I looked back to when I retired at age 59 in 2014 and expenses equal very close to 25x. Since that time, portfolio growth has been great and value has more than doubled; expenses have grown as we spend a lot of time traveling overseas, but expenses have not doubled, much less; All investments self-managed, and mostly growth tech stock oriented;

your statement:

…but your investments also need to generate enough passive incometo cover your living expenses.

Most of my retired friends do not self manage investments at all, some say they do but really a lot is “check up calls” from their broker of what he is buying or changing in their accounts; Their brokers seem to be into large cap “big dividend” stocks or ETFs or the dividend aristocrats, etc their training is older or retired people get dividend stocks.

I have always focused on total annual return of a stock or ETF or really any investment, IE growth in value for the year ‘plus’ dividend paid; what is wrong with selling a few shares or whatever you need for expenses, no issue in my book esp in a growth portfolio; income can come from selling shares you are using for expenses, why not esp if you like and believe in the stock or ETF you own over selling and buying another that just happens to pay a larger dividend but little growth potential (utility stock, etc); Am I missing something?

Seems like there was a story about someone asking Warren Buffet at an annual meeting years ago why Berkshire did not pay dividends; I think his answer was something similar to “Because I can make more on the income than you can or something similar. Sell a share or two if you need money for expenses”. (Hope this was a real story, but let’s face it, he could make more than me for sure.)

All that being said, Expenses don’t have to actually equal passive income for me.

Also one of my favorite saying is “One size does not fit all”, comparing your home cost and operating expenses/taxes in SF with mine in rural GA would be very different; but you will enjoy some great value increases in SF for sure I hope, much less so for me; “although I did pay a plumber a minimum call cost of $150 and that was for about 10 minutes of work…and well worth it.

All the best and thanks for all the info and ideas you share,

FS

So, let’s just be clear and realistic – no one is ever going to be able to retire early in this country and economy, even with a net worth significantly higher than the astoundingly low median US net worth indicated. Seriously, what’s the point? Sigh.

Never say nobody. There are people retiring early every month. But they are probably doing so by saving more than 25 times their annual expenses.

They probably also have supplemental retirement income, relocated to a lower cost area of the country or the world, or even have a working spouse.

It’s always worth the effort. Even better if you know what to expect before taking the leap!

Related: The negatives of early retirement nobody likes talking about

In your letter, you asked if I agreed on your assessment if the 4% rule works for early retirees.

1. Include primary residence = No. Agreed with you.

2. Does your 4% stack need to be liquid = Yes. With the added requirement of you need enough in brokerage to cover you through 59.5.

3. Does this liquid stack need to be limited to dividends = No. Selling capital gains is great as well. And, there are some tax advantages to capital gains.

Key Hedges = Social Security/Medicare, Kids moving out of the house and getting independent, selling primary home late in life.

Thanks for all of your content. David

I just start with what i want to spend in retirement. that is 200k per year, 160k after taxes. then i calculate my liquid savings needed by assuming it will all be in SPY. SPY yield has remained in the 1.8%ish area for a long time. so need 11.2M to generate 200k. so that means saving 55x annual expenses. that is the most conservative scenario possible from the standpoint that it’s assuming no other income streams but dividends but also the most risky in that it provides for the most possible growth (and temp loss) of principle.

using the same exercise with BND at 3.76% yield means need 5.35M to yield 200k. or about 27X annual expenses.

that helps me see the incredible range of the ways you can look at and it results in tremendously different financial goals. if you have 5.35M and you just stick it in BND for the rest of your life you probably never need to tap

principle and you die with at least 5M.

The caveat is I have about 50k in necessary expenses. the rest of the 110k is all discretionary so there is slot of flexibility if real

hard times arise.

All very logical approaches. Although, I don’t think the S&P 500 dividend yield is 1.8% after such huge growth. I think it’s closer to 1.4%.

Based on your approach, what is your target Liquid net worth?

current liquid NW is 6.8m. Fully paid off primary residence on top of that. i am 60 and still working. so i consider myself completely free to retire tomorrow or work half heartedly or whatever i want. even bought a convertible recently..

There are already similar comments here, but personally, I’ve always found the concept challenging where dividend incomes are considered more passive/better than the appreciation of a stock or ETF. My preference leans towards investing in ETFs that reinvest dividends automatically due to the more favorable tax treatment it offers in my region. For me, financial independence is defined as having 25 times my annual expenses invested in equities/bonds, adjusted for capital gains tax. I completely agree that primary house should be excluded from net worth while i have no plans to sell or rent it.

It’s true. Some companies pay their dividends out to investors, others reinvest them by building new products/facilities or buying back stock. Either way, it’s “passive income”, the only difference is whether it goes automatically into your bank account, or you have to sell shares to get it. (Thought experiment: How much Berkshire Hathaway would you have to own to retire early? Probably less than ∞% :)

Very good point about payouts.

Hi Sam,

How about splitting the net worth into two parts: a) illiquid real estate that will be passed onto our children and b) stocks/bonds at least 25x expenses. Is this overly simplistic?

Your kids are assured an inheritance of real estate that can provide income forever. Guilt free spending of part b that can deplete the principal (or not). Would love to hear any thoughts.

You are missing the concept of total return: instead of loading up on income producing stocks or bonds and selling at ordinary income, an investor can sell growth equities and pay capital gains to cover expenses. Research shows it will produce greater returns and capital gains are less than ordinary income.

Could be. Check out my recent post: Clearing Up Misconceptions About The 4% Rule

“The Safe Withdrawal Rate it is computed on a “total return” basis: It makes no distinction between principal, capital appreciation, dividends, interest, and other forms of income. For example, if you have a $1 million portfolio that generates $20,000 a year in income, a 5% withdrawal rate would mean withdrawing $50,000, not $50,000 + $20,000.”

****

The issue is, a lot of retirees don’t want to draw down Principal and pay taxes. They also want to leave a legacy by leaving money to their children and foundations, instead of dying with zero.

get an SBLOC and borrow against your assets in your brokerage portfolio. Never pay taxes on the debt and never sell your assets until you die. Pass them on to your heirs and they won’t pay taxes on your portfolio if they decide to sell at your time of death because of step-up basis

It’s a good plan and something I should have considered doing in 2023 when I bought my house. But the rates were high. Need to check how high they are now. If I couldn’t borrow the entire amount to pay cash for the house, I would’ve had to have paid an extra $10,000 or more to get a mortgage which I didn’t wanna do.

I have my SBLOC in place now. Rate is currently at 8% so I’m waiting for it to come down before I tap into it. Thinkikg of using it to buy a primary residence.

What are your rhoughts on doing this?

There is something fundamentally wrong about this type of article. Seems sponsored by the financial industry, whose primary purpose is to convince people to save as much as possible to generate fees. There is no denying that the living cost is in the US is high and it may be worth moving overseas in a country with lower property taxes and decent healthcare. I have no intent to build generational wealth. I inherited barely anything from my parents and I had no choice to work hard to become financially independent (in my book). My (young) daughters will learn not to expect anything from me except love, a good education and the drive to achieve great things in a complicated world. I’ll also teach them to spend sparingly in a world soon to be devastated by climate change. It is ludicrous to spend the amount of money you spend every year. It is also morally wrong. Millions of people around the world know how to live with barely anything. They can teach us a lot.

You could be right. But holdings stocks and bonds is pretty much free nowadays.

At what age did you retire and with what multiple of annual expenses?

What do you think is the right annual expense multiple to retire early, before the age of 55. It’s always great to get perspective from different people who have achieved financial freedom.

To learn from people who have actually quit their jobs and followed a set safe withdrawal rate or strategy is always insightful.

I am in my early 50s. I have not retired yet, but I’m thinking about it. I do like my job and I’m not sure what I would do if I had to quit suddenly. My goal at the beginning of my career was to achieve financial independence. By financial independence I mean I can quit my job today and not worry about having to find another job immediately. It took me 20 years of living within my means and investing regularly. I avoided the trappings of wealth and kept my expenses low. I paid off my mortgage on my primary residence and acquired another property to generate rental income. I have no credit card debt and healthy investments. My investments are diversified (stocks, bonds, crypto and real estate). I particularly like municipal bonds, which generate income free of federal and state taxes. Particulate valuable for those in a high tax bracket. If I do retire early, then I will start selling off my investments to cover basic expenses. Again, my goal was never to generate generational wealth. It will be up to my daughters to figure out how to do it, with my guidance of course.

Thanks for sharing.

“ By financial independence I mean I can quit my job today and not worry about having to find another job immediately.”

This is the first time I have heard of this definition. If we use this definition, perhaps millions more people in America alone or financially independent, which is cool. A lot more people can kick back and not work as much.

What is your Liquid net worth calculated by a multiple of annual expenses, if you think 25 times is enough to retire early?

Consider taking a leap of faith and retiring given you believe the financial industry and my post are pushing people to save and invest too much for their financial security. Add 50, hopefully most of your children’s expenses are behind you. It generally feels good to be consistent with thought and action.

Can I ask how do you factor in say social security or an annuity into this? For example, let’s say I expect to get 30,000 a year from Social Security and another say 50,000 from an annuity but I want my total expenses before taxes or income before taxes to be 150,000. I assume I’m deducting the 80,000 from the 150 and then that’s what I would need to live off of the 70K and times that by 25 or 45 or whatever we want to use?

agreed mostly with this. Easy heuristic: 50x NW excluding home after 40, 40x NW ex home after 50, 30x after 60, 25x after 70

Yes, the capital for the 25X rule doesn’t include your owner-occupied primary residence. Otherwise you would have to add implicit rent to the expenses you are multiplying by 25.

What a polite way to tell me not to quit my day job. :-p

No one I know would include the home in retirement 25x type analysis or rental property or social security or pensions. This should comprise of cash (emergency fund); taxable brokerage account; and retirement accounts. If all the big 3 equal 25x annual spending then following the 4% rule you are historically going to be fine assuming not relocating in retirement to a HCOL area like the Bay Area If retiring early I would reduce rule to 3.75 if between 55-60 and 3.5 if between 50-55. Also, the retirement account should really be less than 1/3 due to delayed access.

100% agree. I also think that allocation of 50% of net worth to FIRE candidates is too high – from reading the article above it seemed aimed at the average retiree which includes the larger, older population.

The best article I have read on retirement planning for FIRE reperformed the 4% test (based on a 30 year retirement) with a 40 and 50 year horizon. The result of the article was that regardless of the length of retirement, 3.5% was the magic number to never run out of money. This was not hypothetical – it was based on a 50/50 equity bond investment and used actual historical returns. So the article suggests a 45.5x savings and the actual research suggests 28.5%.

Bill Bengen has suggested a 4.3% withdrawal rate for a 50-year horizon in my podcast with him.

Although I helped kickstart the modern-day FIRE movement in 2009 when I started writing about retiring early and negotiating a severance package, Financial Samurai is not solely focused on FIRE. So my audience are not the hardcore FIRE aspirants that you might see on other forums or sites.

The other thing to note is that math and life often conflict. You can do the math all you like, but unless you’ve actually walked away from a steady paycheck and don’t have a working spouse supporting you, strictly following the withdrawal rate will be tough. I try to share the nuances of FIRE, good and bad, since I left work in 2012.

Where are you on your financial independence journey? If you’ve been retired for a while, have you been able to follow a SWR? If so, what has it been? Thanks

“No one I know would include the home in retirement 25x type analysis or rental property…”. I am assuming you are talking about not including rental property equity. The cash flow from a rental property should be included in FIRE calculations.

Great post! It’s helpful to clarify to folks pursuing FIRE that liquid assets is needed to fund RE and also circumstances will change in the future which will require more or less money to fund retirement.

We are heading into RE with a mindset of being flexible and if we need to adjust our lifestyle we will and/or go back to work part time if needed. We just retired this year at the age of 40 & 42 (no kids in HCOL). We have passive income – rental income, dividends & interest, plus we are planning on withdrawing up to 4% of our liquid investments (brokerage, ROTH, IRA to ROTH conversion strategy). Based on our planning we are aiming to keep our taxable income below the income limit to take advantage of the 0% capital gains tax. We are comfortable but not extravagant and mindful of what we spend our money on. Our biggest expenses include our mortgage, food, healthcare)

We also have equity on our home but we plan to keep it because we have an ADU that generates rental income. If needed we can rent out the primary home to fully or partially offset our housing cost and move to a MCOL or LCOL city.

It definitely took a lot of planning and consistency to get to this point. I remember reading a Financial Samurai article back in 2012 with <$100k NW thinking…how do retire early and how do I even maximize my 401k and brokerage each year to achieve our financial goals. It seemed like a mountain to climb at the time but I got my husband on board, made some hefty lifestyle changes, and here we are. Enjoying the RE life!

Hi Sam, on the topic of leaving something for children and charities, I have a superannuation fund which I cannot take money out of until I am 65 and start receiving government pension as well. Therefore, I have designated this fund to be used for charities and my nieces and nephews on my demise in my will. Covers me leaving them something and free to enjoy my retirement.

Hi Sam –

I am 59 and have a retired husband and 15 year old/high school freshman son. I have $5M in mostly 401K with some minor amounts in HSA, small IRA funds all with Fidelity and fees paid for by employer. I need plan to diversify. I would like to retire at age 62 when son is out of high school. Are you available for a personal consult session?

I very much disagree with the definition of Financial Independence as living off passive investments alone. I think it means living off your investments into perpetuity. I’m working towards a 50:50 split when I enter retirement between risk assets and “safe” assets. My risk holdings are diversified across global equities, private equity, real-estate development deals, infrastructure, hedge funds (e.g., macro and relative trading strategies). My safe assets are anchored on bonds. I am fully comfortable selling assets as needed (or not reinvesting returns from private closed ended funds) to sustain the 4% withdraw rate. My expectation is that I would get a real return of ~6% from this portfolio which should allow the investment to support until 100+ years old even if I’m able to retire in my 40’s (my target). Just because C-suites of public companies decided to return value to shareholders through buy-backs instead of dividends due to tax efficiency should change my FIRE number.

The term is subjective because it partly depends on what type of legacy you want to leave others. There are two main retirement philosophies to consider. Legacy or YOLO.

“ I am fully comfortable selling assets as needed (or not reinvesting returns from private closed ended funds) to sustain the 4% withdraw rate.”

Have you actually started selling down assets to fund your expenses? In my experience, a lot of people say they can do this, but then when it comes time to do so, most can’t after decades of saving and investing for the future.

I retired nearly three years ago at age 57 and I sell assets every single month to pay the bills which include making Roth conversions to the top of the 24% tax bracket. Not selling assets would mean not enjoying our retirement.

I actually found it easy to transition into the selling phase because I developed a objective strategy to decide which mutual funds to sell based on percentage of portfolio rebalancing and asset allocation.

This is great to hear! I completely agree that not selling assets is suboptimal in retirement. It means you will die with too much and will have wasted your younger years stressing and working too much.

You retired at what could be the new traditional retirement age!

How do think about leaving money to your children and other organizations after you pass? I’m constantly thinking about these factors at the moment. Thanks.

I’m not too charitably minded, but outside of a disaster, our daughter will inherit quite a bit of money.

We’re gifting her shares of stock every year, NFLX in particular with a cost basis of $1.96 which she can sell at no capital gains due to her lower income. This way, she is learning about managing investments and getting to enjoy the money while we’re still around and she’s not making much.

By definition, “you will die with too much” is your legacy philosophy, of which you subscribe.

Yes. How about you?

I agree. I currently give to charity (Paul Anderson Youth Home), but the bulk of my estate will go to family.

How do you reconcile this with your acts of decumulation?

It’s a tough balance. Got to proceed carefully every year and recalculate. I’m trying to get back to financial independence by 2027. So the pace of decumulation is going to slow.

How about you?

Balance is a good concept. I lean toward legacy.

I think of it this way: even with the traditional 25x retirement level, you have a good chance of leaving your kids a boatload of money.

I retired earlier this year at age 41 with 23x my annual expenses, or $1.4M, in liquid net worth. Running cFIREsim assuming my wife and I live to 100, and assuming Social Security still exists, yields a 97.85% success rate, which I’m comfortable with for my own retirement.

But in that same simulation, the median end portfolio value (when I am 100 years old) came out to $8.2M, meaning there is a greater than 50% chance that I will leave my son a pretty nice pile of money!

Great way to look at it and great feedback. You seem very confident, which is great. I did not feel as confident when I left in 2012 with 31 times liquid net worth, and could not last past 18 months with the desire to earn active income through part-time consulting and online income.

I’m curious what your financial concerns are now, if any? Any second-guessing or growing desire to generate active income as well? Are you able to get subsidized healthcare insurance? Any kids? Having kids really jumped my motivation to earn into overdrive in 2017.

I do believe between the ages of 41 to 45 are the ideal ages to retire early. So your datapoint is very helpful and supporting it. Thx

This is an article you might find interesting: the negatives of early retirement nobody likes talking about

Also, some good commentary in the post: Misconceptions of the 4% Rule, where I also chat with Bill Bengen.

I am probably suffering from overconfidence if anything, having been originally schooled by the “optimist FI” writers like MMM and Millennial Revolution, though I have read a lot of your stuff as well (including the above two) for a balancing perspective.

For health insurance I am paying out of pocket for a bronze plan that was $1750/month this year and will go up to $2100/month next year (insane right?) But I expect to receive subsidies to get it down to about $800/month, at the end of next tax year (I am paying premiums upfront with no APTC since my “income” is just Roth conversions and dividends so will vary from month to month).

My biggest financial concern is that the Roth conversions will not quite bridge the gap, since I can only withdraw principal penalty free, so I may find myself at age 55 or 56 with only appreciation in the Roth… but that should be a solvable problem if it happens.

No second-guessing the decision to FIRE yet (Wall Street is a tough place to work, I don’t miss it!) but the issue now is figuring out how to fill the day with meaningful activities. I do have a kid in elementary school but while he’s at school I have 6-7 hours a day without any demands being made on my time and attention. So I may end up going back to consulting or something part time.

Very insightful that you follow MMM and MR as a Wall Street guy in NYC, when those too live so spartanly. What do you think the appeal is? Your feedback may give me inside into whether I should focus more on frugal, living and budgeting in the upcoming years. Focus on easy mode instead of hard mode for financial independence.

Thx!

The part of their thesis that appeals to me is that spending less doesn’t need to mean enjoying life less and in fact can often mean the opposite. Which is the main gripe I have with the Bill Perkins / Die with Zero school of thought: the unquestioned assumption that spending more means living better. It’s not always true. We love restaurants, but cooking at home 6 out of 7 nights is better for our stomachs and long term health. We love travel, but $800-a-night resorts feel sterile, while $80 a night gets you a very nice hotel for a true cultural immersion experience in a small town in Mexico. We love having a comfortable home, and living in a nice garden apartment saves us on taxes and car ownership vs. a suburban house, etc.

Makes sense. Although, I do believe we tend to justify what we can spend. In other words, if we cannot spend as much as others, we will justify that what we are spending is the perfect life.

It is nice to see people who live so cheaply tell us how great their lives are. Because it gives us hope that we can make less and spend less and potentially be as happy.

At the same time, I think we need to be honest with ourselves that anybody telling the world how great their lives are while spending so little might be trying to make up for not having as much.

Fair point! And if I were to expand in one area, it would be business class plane tickets. Not gonna lie and say I wouldn’t spring for those if I could justify it from a budget perspective! :)

It’s painful to pay 3 to 5 times more for business class tickets when you get to the same place at the same time and the food ain’t much better!

I think this was just a long overly complicated article to say that the 4% rule should only apply to your liquid net worth and not factor in your primary residence. I think most people in the FIRE community agree with that.

Perhaps. I stated the argument in the introduction. Then I followed it up with real life examples and a formula to help people calculate their true expense multiple they should use for their net worth targets.

The idea is to get to the point for those who are unwilling to do a deeper dive analysis, and then do a deep divan analysis for those who are willing.

I do not agree that everybody in the FIRE community thinks that the 4% rule only applies to liquid net worth. Based on the constant feedback that I’ve gotten since 2009, a lot of people simply just multiply their expenses by 25 times and that’s it. I would be careful to assume that everybody is as into this stuff as we are.

But the biggest thing you did not touch upon is one’s net worth composition. That is just as important as the percentage of one’s net worth in liquid, income producing assets. If you continue to read the article, you will see the point with my rollover IRA.

Where are you on your financial independence journey and what do you think is the correct multiple if you disagree with my formula? My hope is that more people will share their examples and what they have discovered so that we can all learn from each other. Thx

Can you explain what you mean in the rollover IRA point a bit more?

I think the multiple to focus on would be to have your liquid investments cover 25x your living expenses after any additional income in retirement.

If you have net income from properties, pension, blog etc, you would be able to use that “first” to cover expenses. Then you’d need a portfolio of stocks & bonds worth 25x the remaining expenses.

The ratio of stocks and bonds is relative to your risk tolerance. Also if you felt very risk adverse you could bump it up to 30x. But like Bill said the other day, that’s probably too conservative.

Does that make sense?

Sure, makes sense. Where are you on your financial independence journey?

I’m right about at 25x expenses and still working, while debating on when to pull the plug.

Thanks for sharing. What stops you from negotiating a severance now and retiring?

Mostly the fear of giving up the paycheck and not really knowing what I’d rather do with my time.

Good points. We need to remain flexible so we can adapt. Whether it’s during retirement or changing course during planning. 4% isn’t gospel, but it’s a great starting point.

It’s also challenging to predict the future. So to account for the inevitable variables, I’d like 30-35x my annual expense to feel comfortable/confident in RE.

Call me nerdy, but I love retirement planning. Thanks for covering such a relevant and fascinating topic.

Very helpful example highlighting how portfolio composition has such an important impact on how much passive income it generates for cash flow purposes. And how tax considerations also should be taken into account.

I need to revisit my dividend yielding holdings and calculate my latest projected output since my allocations have shifted in the last year.

I find myself in this bucket. 49 yrs old, I have around $8m in equity in rental real estate and my primary home. We make around 300k a year in consulting work but our household falls around 100k in expenses short annually.

Aching to sell the RE and live the good life (like Sam mentions!), but I don’t want to take the huge tax and recapture hit. Guess I will let it ride another 5 years before I cash it all up.

The problem is, in five years, chances are high you’ll have an even greater net worth with an even larger tax bill. As a result, it may be even harder to sell assets and retire early.

Changing one’s investment habits and lifestyle truly is hard after decades of doing the same thing.