Some people often argue that the 10-year Treasury bond yield has no correlation with investment returns or safe withdrawal rates (SWRs) in retirement. However, this belief is incorrect. The 10-year Treasury yield, often viewed as a proxy for the risk-free rate in America, significantly influences SWRs, and the relationship is undeniable.

The 10-year Treasury bond yield is the single most important financial figure to follow. It gives insights into inflation, monetary policy, economic growth expectations, and risk sentiment. As a result, all these factors also play a part on your expected investment returns and how much you plan to draw down from your retirement portfolio. Let me explain in more detail.

For background, I've been investing in stocks since 1996 and real estate since 2003. I got my MBA from UC Berkeley, worked at Goldman Sachs and Credit Suisse for 13 years, and have written over 2,500 personal finance articles on Financial Samurai since its founding in 2012. In 2012, I retired at the age of 34 with a net worth of about $3 million, and passive investment income of around $80,000. I have been studying and implementing the risk-free rate of return for almost 30 years.

1. The Risk-Free Rate as a Baseline for Returns

The 10-year Treasury yield serves as a benchmark for setting expectations about future returns on both bonds and stocks. Since safe withdrawal rates hinge on the real rate of return (investment returns adjusted for inflation), changes in the risk-free rate impact portfolio performance, particularly for retirees holding bonds.

- Low 10-Year Yield: When the risk-free rate is low, bond returns are likely to follow suit, reducing overall portfolio returns. This limits how much a retiree can safely withdraw without depleting their portfolio too quickly.

- High 10-Year Yield: In contrast, when the risk-free rate is higher, bonds deliver better returns, potentially boosting overall portfolio performance and supporting a higher withdrawal rate.

2. The Risk-Free Rate's Relationship with Stock Returns

The 10-year Treasury yield doesn’t only affect bonds; it also influences stock valuations through the equity risk premium—the extra return investors demand for holding stocks over bonds. A higher risk-free rate can lead to:

- Lower stock valuations: A higher discount rate lowers the present value of future earnings, potentially reducing future stock returns.

- Shifting preferences toward bonds: As bonds become more attractive, retirement portfolios might allocate more to fixed-income options, reducing reliance on stocks.

When stock returns are expected to decline alongside low bond yields, retirees must often lower their withdrawal rates to account for diminished portfolio growth.

The Equity Risk Premium And Risk-Free Rate

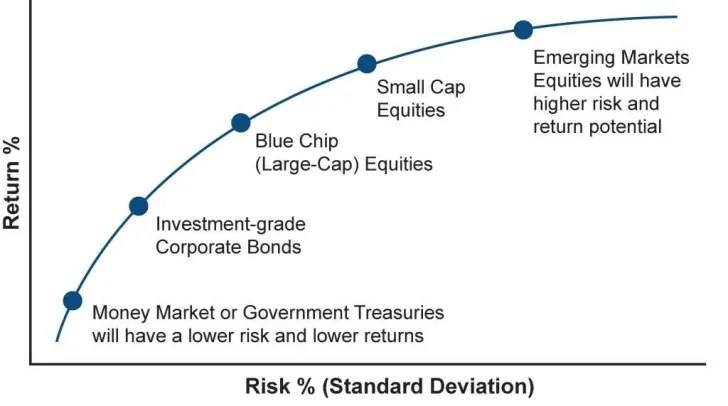

The equity risk premium (ERP) is the additional return investors expect to earn from investing in equities (stocks) over the risk-free rate, which typically refers to the yield on government securities like U.S. Treasury bonds. This premium compensates investors for taking on the higher risk associated with equity investments compared to risk-free assets.

Unlike government bonds, which are backed by the full faith and credit of the government and carry negligible default risk, equities are subject to market volatility, economic fluctuations, and company-specific risks.

The relationship between the equity risk premium and the risk-free rate is fundamental to understanding expected returns in financial markets. The risk-free rate serves as the baseline return investors could earn with virtually no risk. The ERP quantifies the excess return required to entice investors to accept the uncertainty and variability of stock market investments.

For instance, if the risk-free rate is 4% and the expected return on a stock market index is 9%, the ERP is 5%. This differential reflects the trade-off investors make: taking on more risk in exchange for potentially higher returns.

3. Historical Correlation and SWR Adjustments

The original 4% Rule assumes a balanced portfolio (typically 60% stocks, 40% bonds) with a long-term real return averaging 4%-5%. However, historical data shows:

- Low-yield environments: When the 10-year Treasury yield is historically low (e.g., post-2008 or during 2020-2022), studies suggest that a 4% withdrawal rate may be too aggressive. Lower bond yields shrink the margin of safety for retirees.

- High-yield environments: In times of elevated yields (e.g., the 1980s), retirees could withdraw at higher rates due to robust fixed-income returns bolstering their portfolios.

Ultimately, a retiree should adopt a dynamic safe withdrawal rate that changes with the economic times, and personal financial condition.

4. Monte Carlo Simulations and Yield Assumptions

Monte Carlo simulations are widely used to assess Safe Withdrawal Rate sustainability, and the starting bond yield is a critical input:

- Low starting yields: These often lead to reduced SWR projections because bonds are unlikely to provide a reliable buffer if stocks underperform.

- High starting yields: These increase confidence in SWR projections, as bonds provide a stable income even during periods of stock market volatility.

If you could choose the best time to retire, it would be during a bear market. If you are able to retire in a bear market, this means your retirement portfolio and your investor psyche is battle tested for a difficult environment. Given bear markets only last between 1-3 years, long-term, your retirement portfolio should have return upside.

5. The Risk-Free Rate And Its Practical Implications for Retirees

- Dynamic Withdrawals: In a low-yield environment, retirees may need to start with a withdrawal rate closer to 3% or lower to ensure portfolio longevity. During the first year of retirement, it will feel jolting not to have a day job to go to for 40 hours a week anymore. As a result, it's best to stay conservative with your SWR.

- Portfolio Adjustments: To offset the impact of low bond yields, retirees might consider alternative income-generating assets, such as dividend-paying stocks, real estate, or annuities.

- Inflation Consideration: Rising bond yields due to inflation expectations can erode the real returns of fixed-income securities, requiring retirees to adapt their withdrawal strategies accordingly.

Podcast Interview With Bill Bengen On Risk-Free Rates And Its Affect On SWR

Here's is my conversation with Bill Bengen, creator of the 4% Rule on safe withdrawal rates for retirees to live securely. You'll hear us also discuss about how the risk-free rate affects safe withdrawal rates.

The 10-Year Treasury Bond Yield Must Be Followed

There is a meaningful correlation between the 10-year Treasury yield and safe withdrawal rates. Understanding this relationship is critical for retirees and financial planners aiming to optimize withdrawal strategies and maintain financial security in retirement. Let's use an example to demonstrate further.

Example: John’s Retirement Dilemma Using The 10-Year Treasury Yield

John, a 65-year-old retiree, has a liquid $1 million portfolio. He plans to use it to cover living expenses alongside Social Security. His financial planner advises him to consider the current economic environment, particularly the 10-year Treasury bond yield, when setting his withdrawal rate.

Step 1: Assessing the Current 10-Year Treasury Yield

The 10-year Treasury yield is currently 4%. Historically, this is considered moderate and offers better fixed-income returns compared to the near-zero yields from 2008-2020. However, it’s not as high as the yields seen in the 1980s, when bonds generated double-digit returns.

Step 2: Calculating Real Returns

John’s financial planner reminds him that the 4% yield is nominal, not adjusted for inflation. If inflation is 3%, the real return on his bond allocation is just 1%. For his stock allocation, the planner estimates a 6% nominal return, translating to a 3% real return after inflation.

Step 3: Portfolio Allocation And Real Returns

John’s portfolio is 60% stocks and 40% bonds—typical for a retiree following the 4% Rule. The weighted real return for his portfolio is:

(60%×3%) + (40%×1%)=2.2%

This 2.2% real return serves as a baseline for how much his portfolio might grow over time, adjusted for inflation.

Step 4: Determining the SWR

Given the 10-year Treasury yield of 4%, John realizes the traditional 4% Rule might be aggressive in the current environment. His planner uses Monte Carlo simulations to test the sustainability of different withdrawal rates:

- At a 4% withdrawal rate: There’s a 75% chance John’s portfolio lasts 30 years.

- At a 3.5% withdrawal rate: The probability increases to 85%.

- At a 3% withdrawal rate: The success rate is over 95%, giving him more confidence in his financial security.

Based on these results, John decides to start with a 3.5% withdrawal rate, or $35,000 annually, while monitoring his portfolio performance.

Step 5: Dynamic Adjustments

To remain flexible, John adopts a dynamic withdrawal strategy. If the 10-year yield rises above 5%, boosting bond returns, he may increase his withdrawal rate slightly. Conversely, if yields fall or stocks underperform, he’s prepared to reduce spending temporarily.

Practical Takeaways

- John’s financial decisions highlight how the 10-year Treasury yield serves as a proxy for the broader investment climate, influencing safe withdrawal rates.

- By understanding the yield’s impact on portfolio returns, John avoids overestimating his portfolio’s ability to sustain withdrawals.

- He mitigates risks by starting conservatively and adjusting his withdrawals based on economic conditions.

This example illustrates the real-world application of tying the 10-year Treasury yield to SWRs, helping retirees make informed decisions in a changing economic environment.

Always Compare Any Withdrawal Or Investment Decision With The Risk-Free Rate Of Return

Comparing every withdrawal or investment decision to the risk-free rate is essential for maintaining financial discipline and making informed choices. Understanding opportunity cost is vital for investors and retirees.

The risk-free rate acts as a baseline, helping retirees and investors evaluate whether the potential returns of riskier investments justify their added uncertainty. By using this benchmark, individuals can avoid overextending into speculative assets or making withdrawals that might deplete their portfolio prematurely.

For retirees, the risk-free rate is particularly useful for preserving capital and assessing the sustainability of withdrawal strategies. Aligning withdrawals with returns that exceed the risk-free rate ensures a more stable financial future while helping to mitigate the risk of outliving one’s savings. Similarly, investment decisions grounded in this benchmark can balance the need for growth with the need for security, fostering a well-rounded and resilient portfolio.

In short, the risk-free rate is a practical tool that anchors financial decision-making. Whether you’re withdrawing funds, reallocating assets, or assessing portfolio risks, referencing the risk-free rate ensures your choices are aligned with both your risk tolerance and long-term goals. It’s a simple yet powerful way to promote financial stability and independence.

Diversify Your Retirement Investments

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the risk-free rate declines, real estate becomes more affordable, putting upward pressure on pricing.

I’ve personally invested over $270,000 with Fundrise, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Your shares, ratings, and reviews are appreciated.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009. Everything is written based on firsthand experience and expertise because money is too important to be left up to the inexperienced.