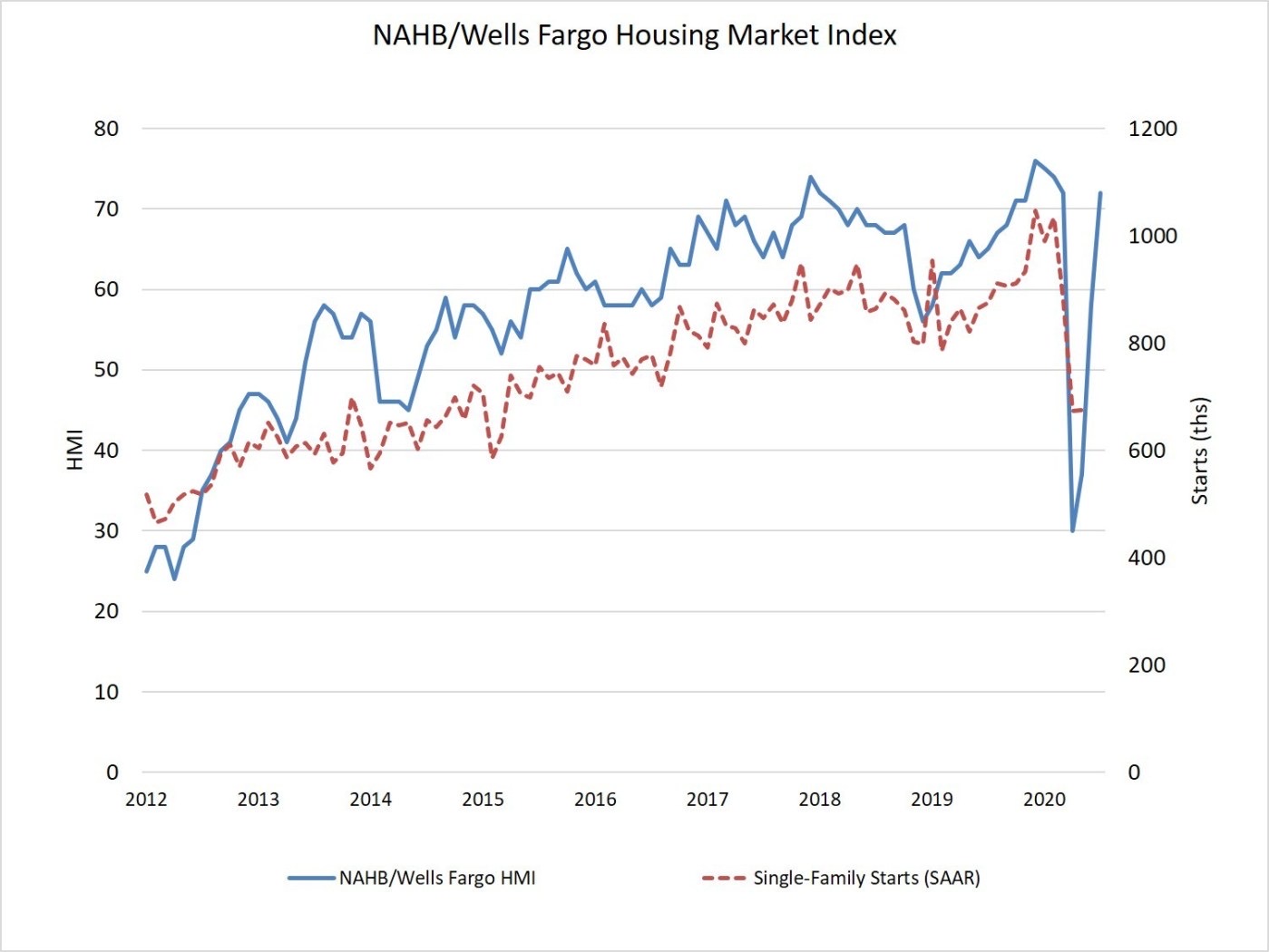

For the longest time, I’ve been a proponent of the adjustable rate mortgage (ARM). Paying a higher rate for a longer duration than necessary doesn't make economic sense. However, when the average 30-year fixed mortgage was under 3% in 2021, I no longer was as biased against 30-year fixed-rate mortgages.

A sub-3% average 30-year fixed mortgage rate was so low, it must have spurned more people to buy homes. Unfortunately, in 2022, the average 30-year fixed rate mortgage reached almost 6% due to high inflation and an aggressive Federal Reserve.

Now in 2024, rates are finally starting to come back down again.

If you're looking to refinance, check the latest mortgage rates with an online mortgage lending rate marketplace. You’ll get real, no-obligation quotes from competing lenders in minutes. Take advantage of getting multiple rates in one place.

When the global pandemic was in full effect in 2021, I was curious to know who was buying a home then. Let's read some homebuyer profiles of people who were taking advantage of record low mortgage rates.

Average 30-Year Fixed Mortgage Rate At Record Low: Buyer Profiles

The one thing every homebuyer or potential homebuyer has in common is that all of them have not been financially hurt by the pandemic. Instead, most are now wealthier during the pandemic than pre-pandemic.

These people are taking advantage of the record low average 30-year fixed mortgage rate. Financially savvy people are also focused on buying up as many rental properties in big cities again.

Here are their stories of people buying homes during the middle of the global pandemic.

Who Is Buying Real Estate #1: Big Tech Employee

The NASDAQ closed up over 45% in 2020. As a result, many of my tech colleagues are all looking to buy their first homes or upgrade homes. I work at Apple and Apple stock is up around 28%. As a result, my colleagues and I feel much richer today than we did before the pandemic began. It's weird.

One of the best moves I ever made was not going to a small start up three years ago. They were gonna give me huge equity that would’ve made me tremendously wealthy today if things panned out. However, the start up is struggling with cash flow, while Apple continues to dominate.

With our net worth up ~20% in just six months, we decided to buy a bigger house for our family of five. The average 30-year fixed-rate mortgage rate at under 3% is just icing on the cake. I’m gonna follow your advice and get a 7/1 ARM for 2.375% since we plan to pay off the home in 7 years.

Turning stock market gains into a real asset feels great to me. We are not unique. Most of my tech friends are diversifying their stock gains into real estate.

Who Is Buying Real Estate #2: Sick & Tired Of Being Overly Frugal

For over 10 years, I’ve been saving between 20% to 50% of my after-tax income. My income has also gone from $80,000 to $165,000 during this time frame. But I’m still renting a studio apartment from when I was 25 years old. I'm sick and tired of hoarding so much cash. What's the point if I'm not going to spend it?

Living in a studio apartment has helped me save about $160,000 in living expenses. At the same time, the studio apartment has also cost me money. If I had just bought a property I was looking at back in 2010 for $300,000, it would now be worth more than $500,000 today. I would have also gotten to enjoy a nicer place for all these years as well.

Although I’m happy to have saved a lot over the past 10 years, I feel it’s now time to use my savings to improve the quality of my life. I’m 37 years old and want more space. I want to get married and start a family too. The average 30-year fixed mortgage rate under 3% is too enticing to ignore.

Who Is Buying Real Estate #3: Parents Who Plan To Permanently Work From Home

With work from home likely becoming a permanent trend, I think it’s smart to try and buy a home now before open houses go back to the norm. Eventually, the economy will open up and buyers will return in droves.

All of my friends with kids are fearful of venturing outside. They don't want to get sick or their children sick. I have friends who are too scared to even set up a private showing because they don’t want to breathe the indoor air that other people have breathed.

I can understand the fear, but come on. The death rate is so low, I think some people are being overly precautious. Absolutely wear a mask out in public though. Be respectful of other people's health.

Now with the average 30-year fixed-rate mortgage so cheap, I feel more people will eventually come around to buying.

This debilitating mentality of not wanting to venture outside is eventually going to dissipate. When it does, I think bidding wars will be the norm again.

We are looking to buy a home that has two separate areas where my husband and I can work privately. We are also looking for a home with a nice yard or deck. If there’s a view, even better.

Finally, we already refinanced our existing primary home mortgage to get the lowest rate possible. Once we settle into our new home, we will then rent out our old home and generate passive income.

Who Is Buying Real Estate #4: It's Now Cheaper To Buy Than To Rent

The media likes to talk about a decline in rent prices without talking about a bigger decline in mortgage prices. Maybe this asymmetric reporting is a way for the media to try and “stick it to landlords” since the media knows that's what readers like.

However, if rent prices are down 10% and the average 30-year fixed-rate mortgage rate is down 30%, then owning has become relatively more affordable. Like duh. Such an obvious comparison that everybody seems to be missing.

In my city, buying is now cheaper than renting because mortgage rates have declined so much. There is a buying frenzy for starter homes and homes around our city's median price.

I've moved up the price curve, along with several of my friends to find better value. With more people spending time at home, there is logically going to be more demand for homes.

Who Is Buying Property #5: Homes For My Children

I have older friends whose adult children decided to break their lease and move back in with them. Frankly, after four months of sheltering-in-place, they are sick of their children!

They want them out, paying their own rent, and experiencing more hardship. It's this hardship that's going to help make them get stronger in the future. One friend regrets letting his son back home at all. Now, every time he faces a hardship, he fears his son will just want to come home.

I figure, if rolling lockdowns are going to be the norm, then I would rather invest in properties today. The properties will be viewed as investments now and places for my children to stay in 15-20 years if needed. My kids are 7, 9, and 11.

In 15-20 years, when my kids have jobs, I think they are going to wish I had bought more property today. In 15-20 years, I will probably have paid off at least one property as well. I'd like to lock an average 30-year fixed-rate for under 3% before an economic rebound.

Given I'm investing for a 20+-year time horizon, I'm not worried about short-term price volatility. I know there's risk to buying property now. But I'm seeing some relatively good deals.

Who Is Buying Housing #6: We Found Our Dream Home

We live in a neighborhood with incredible ocean views. However, not all homes have ocean views. Only homes on the west side of the block do. If your home is on the east side of the block, you're usually facing homes on the west side of the block, unless you built an addition.

In the past, every time a home with views went on the market, it would be snatched up within days. Even run down homes on the west side of the block would be purchased quickly. Thankfully, we stumbled upon a home that curiously decided to list in April, 30 days into shelter-in-place! Because April was the scariest and most uncertain month so far, few people were buying homes.

There was little competition and we were able to buy our dream home with views and more space for about 10% less than what the home would have sold for before shelter-in-place began. The home is also remodeled and ready to go.

After waiting for three years, we can't believe our luck. Even if it takes a while for the housing market to recover, we're thrilled to live in a nicer home for the next 10 years. Our finances are strong because we both are working from home. Our investments are also back to where they were at the beginning of the year.

Who Is Buying Property #7: I'm Going To Propose To My Girlfriend

I'm 26 years old and plan to propose to my girlfriend later this year. As a result, I am buying a two bedroom, two bathroom condominium for $560,000. The asking price was $580,000.

I came up with $30,000 of the downpayment, and my parents came up with the remaining $82,000. My uncle even offered $20,000, but I refused.

My girlfriend currently rents a room for $1,300 a month. She'll move in with me and we'll see if we can rent out the second bedroom for extra income.

Who Is Buying #8: We See Investment Opportunity

Whenever there is some sort of financial crisis, there is investment opportunity. We are buying single family homes in San Francisco that are 50% higher than the median price point because there is better value. Jumbo loans are harder to get at the moment, so we are taking advantage of less competition.

We're also looking for distressed commercial real estate opportunities on platforms like Fundrise and CrowdStreet. These companies are working with sponsors who are looking for the same opportunities. If priced low enough, some office buildings and hotels could be very attractive if the economy opens back up.

I especially like searching for deals in 18-hour cities with CrowdStreet. There should be a permanent trend of Americans relocating to lower-cost cities.

We've surveyed thousands of employees who say the ideal work environment would be 2-3 days in the office a week, 2-3 days at home. Office buildings are here to stay and travel will return.

The Wealth Gap Will Likely Widen

The pandemic was an incredibly weird time to buy real estate. Hopefully these stories and the subsequent comments in this post provided you with more insights on who was buying.

On the one hand, there were tens of millions of people unemployed or underemployed. On the other hand, the average mortgage rate for all durations hit record-lows. Meanwhile, millions of stock investors who held on had record-high or close to record-high portfolios.

After the recession was over, sadly, the wealth gap will likely continue to widen even further. If you're out of a job, there's no way you're going to buy a house, let alone get preapproved for a mortgage. But if you have a job, you can take advantage of such great discounts. These opportunities are the reasons why we financially prepare for so long.

The cities that continue to have strong job prospects will likely get even more expensive over time. For every one person who leaves, there is likely going to be 1.2 people who take their place. The decision to relocate to the middle of nowhere to save money is now being over-hyped.

Instead, we are creatures of habit. We like familiarity. If necessary, we will first look for cheaper places to live in our current cities. And we will find cheaper accommodations if we bother to look.

The Best Type Of Mortgage To Get

I've been a long-time advocate for getting an adjustable rate mortgage because interest rates have been coming down for over 35 years. With the average duration of homeownership around 8 years, it's not optimal to pay a higher interest rate with a 30-year fixed or 15-year fixed term.

However, there can be mortgage market anomalies. The average 30-year fixed and 15-year fixed rate mortgages were offering better deals than the typical 5/1 ARM. Similar anomalies could surface again so be on the lookout.

To pay off your loan quicker and save, consider getting a 15-year fixed mortgage. If you have the cash flow, you're going to feel great paying off your mortgage quicker. Less interest payments always is nice.

With stock market wealth near all-time, it almost feels like investors are on cheat mode. Add on the fact that millions of people now get to make the same amount of money working from home, the housing market is likely to stay buoyant.

Achieve Financial Freedom Through Real Estate

Real estate is my favorite way to achieving financial freedom because it is a tangible asset that is less volatile, provides utility, and generates income. Stocks are fine, but stock yields are low and stocks are much more volatile.

The combination of higher rents and higher asset values make real estate a tremendous long-term investment. Further, high inflation provides a positive tailwind for real estate.

Take a look at my two favorite real estate crowdfunding platforms that are free to sign up and explore:

Fundrise: A way for accredited and non-accredited investors to diversify into real estate through private eFunds. Fundrise has been around since 2012 and offers a super low $10 entry point for investors. Their vertically integrated real estate platform manages over $3.5 billion in assets and has over 500,000 investors.

CrowdStreet: A way for accredited investors to invest in individual real estate opportunities mostly in 18-hour cities. 18-hour cities are secondary cities with lower valuations, higher rental yields, and potentially higher growth due to job growth and demographic trends.

I've personally invested $954,000 in real estate crowdfunding across 18 projects to take advantage of lower valuations in the heartland of America. My real estate investments account for roughly 50% of my current passive income of ~$300,000.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009. Everything is written based off firsthand experience.

This article contains references to products and services from one or more of our advertisers. Fundrise is a sponsor of Financial Samurai and Financial Samurai is an investor in Fundrise. When you sign up through links on our site, your information stays private. We may also earn a commission at no additional cost to you. Thanks for your readership and support.

I am a little torn between 7/6m and 30y fixed refi now. For a jumbo loan, I get 2.125% 7/6m w/ quite some lender credit, and 2.625% for 30 yr fixed. I am a big proponent of ARM and having a 10/1 for just a year. But the 30y is so low and 0.5% spread is hard to justify.

Just bought my first rental property for $185K, $150K loan in total, my interest on the loan is 2.2% fixed! Should I buy another one?

Depends on your income, net worth, and percent of net worth currently in real estate.

Income: $100K per year

Net worth: $150K

Net worth currently on real estate: 25%

Any advice would be great: currently renting a family home at only $650 a month. No debt. I don’t know if I should wait to buy!

I. I’m a 40 year old single earner living in Central MA and have been saving money for years, but was quickly outpaced by the market. In hindsight I should have bought years ago.

I am planning on retiring in 20 years because I already have health issues that are not going to age well, so while I will take a 30 year mortgage but I plan on paying it off in 20 years.

My income is 4500 take home, and I have excellent benefits and 11% of my gross income goes to my pension. I also have some money in a brokerage account I opened in April, when I scooped up some cheap stocks and also opened a ROTH IRA and maxed it out for the year.

I have done my budget several times and have figured i shouldn’t do more than a 200,000 mortgage after my downpayment. (Planning for a new car soon). So I can afford a 280,000 home, but nothing in MA is listed around my area in that price range.

Do I wait to buy? Will the foreclosures be coming?

I did a refi at 2.25% for a 30 yr fixed rate mortgage.

Awesome! How much did it cost you? Because it’s impossible to get that rate without paying points. Thanks

Total of all closing cost was just shy of $12k for a $245K loan. Points cost me $3684 and establishing a new escrow was another $3500. My monthly payment went down by just under $200/month. My old loan was at 3.5%.

It was nice looking at an amortization schedule and none of the payments had more going to interest than principal.

This was a VA streamline loan.

Yes, please tell us which lender you used

Don’t forget people leaving high population areas because of the pandemic! I know multiple NYC residents who’ve moved to more rural areas

For sure. I’m looking to buy in bigger cities like SF, NYC. Less people makes city living better. And if there is a vaccine, there is going to be a rush of graduates and veteran professionals back bc big cities have the most opportunity.

I know from family in VT that Boston & NYC folks (called “panic buyers”) Are buying up there- but have no community, activities for their families or even understand what it means to own rural property in the real North. They’re lost up there & it shows. I’m betting they’ll get a few months of a real winter (Oct-Jan w/all the Dark & mice, etc) & be done with VT by February, with no spring in sight yet. (that’s in May)

Will they sell or rent?

Who would buy then at these inflated prices?

Wrote my real estate love letter two days ago, and traded up the primary residence today. Scored a 6300 sf home home on .7 acre- room without immediate neighbors in a gated community. Will lock on Monday in the 2.625 to 2.75% 30 year fixed. Big time trade up and in the process, refinanced a rental property with a cash out of 40k to pay off one rental. Took the rate from 4.125 to 3.25 (investor property a little higher than owner occupied but still a great rate). I will take 50k out of savings to pay off a second rental and be left with a single rental property mortgage of 120k, two owned free and clear, and cash flow to cover 66% of the new mortgage. Sam, couldn’t have done it without some tips/ideas from your site. Thank you!

Jim

Any tips for finding such a low rate for a rental property? When I asked around this spring, I was quoted 1% higher for a rental property than an owner-occupied home.

Thanks,

Colin

Rates are just lower now than this spring. I encountered the same thing with my rentals this spring, but am currently starting the refi process for them at 3.25% also. I suggest looking at rates again.

We are retired and living off our investments, savings, ss, etc. We bought in 2016 in SF to hedge our assets and secure housing for offspring. We have a 30yr fixed – 3.5% loan. However, even when we pay off our mortgage, there is that nagging SF property tax. This year it was $18k. And it increases every year. Might have to go back to work . . . :(

Why not sell, cash-in and relocate to a low-cost state like AZ… just like CA (in the winter time)…

Another fantastic article Sam! Agree with your buyer categorization and perspective.

Wife and I are conservatively building a portfolio of properties and we close on our 4th home in 10 days. This property is located in Scottsdale, AZ – single family designed by FLW apprentice and will serve as our winter home in retirement. We scored 2.875% with 20% down which yields a total payment @ $3,100 with taxes and insurance. The home is currently rented for $8K/month (through 7/31) given its location and proximity to Old town Scottsdale. We plan to move in for a few months and then convert back to a rental.

We live in the Bay Area and considering to sell our primary home in SV and relocate to Carmel or Marin area since we predominately work from home. In preparation for this potential move, our lender offered us 2.75% with .6 points assuming 30% down. Should we stay, we plan to refi at the same rate with similar points. We’ll see…

Again thanks for your sharing your knowledge…

-ModScooter

Hello ModScooter,

I also live in the Bay Area and considered moving to Scottsdale one day. I have some rental properties in Goodyear. Was wondering which area of Scottsdale did you buy your latest property in, since it’s rented out for 8k. Thanks!

Hey Lovematcha!

McCormick Ranch (MCR) and specifically zip code – 85258. Rentals are super hot in this area especially for snowbirds. MCR is the greenest part of Scottsdale situated in the heart of Scottsdale. Family friendly, safe, short walking distance to parks, trails, retail and quick drive/bike to Old Town.

This property rents between $8500-$12000/month and has been rented by a few families since 2017 – 100% full every month. The AVG in this neighborhood is $7K for fully furnished 3-4 bedrooms. We are also purchasing it off-market from a family that owns several properties including one in Paradise Valley where they rent for $30K month. All of their properties are fully rented. They are also from the Bay Area and super RE astute.

Where do you live in the Bay? Looking to buy a place near Apple? :)

Best

ModScooter

Hi! Always love reading your stuff! What is your recommendation for people who live in Hawaii? Average price of a single family home is over $800k. We’re trying to buy our first home. Husband is a veteran so we can use VA loan. I just don’t feel like the 30/30/3 makes sense for here because cost of living is so high. You’re lucky if you find a 2 bed 1 bath for under $2,000 month for rent here.

I love following the real estate market. It’s so great for buyers that mortgage rates are so low and also good for refinancing. It takes a lot of patience to deal with the banks because of the amount of underwriting and lower staffing due to the pandemic, but it’s worth it for the savings.

Glad to see people are buying and taking advantage of good prices and low mortgage rates. It’s crazy how low the average 30-year fixed mortgage rate is now!

Great to read through all the comments on this post. To share my experience, we live outside of the US currently, but hold 2 investment properties in US (formerly were primary residences which we converted to rentals when we moved out).

Investment 1 – In a NYC metro area – 10% price reduction (based on zillow estimates) in this area. 1 bed 1.5 bath condo. Rental still going strong for now, but I fear how long will it be.

Investment 2 – In a small town suburbia in a Mid-Atlantic state .. prices are up about 1.5% since this time last year! Has taken us 10 years to recover (at least on paper) from the destruction of 07-08 on this property.

Following your lead and going in realestate investments through fundrise now since its easier to do.

My wife and I were days away from purchasing a home with my mother-in-law’s help when lockdowns started happening in March. Our rate was pretty low, around 3.5% (I know they’re lower now), and we were quite happy that we’d be able to get a new home at such a (then) great rate.

Unfortunately, the deal fell through due to the pandemic, but in the end it worked out for all of us. This is still an excellent time to buy and if rates don’t rise in the near future, we may take another shot at purchasing a home.

We bought property to build in last year in Idaho. We are sitting on our hands for the foreclosure market to raise its head to buy a rental that we can live in while our house is being built. Patience. We don’t think interest rates will go up any time soon.

Hi Sam,

Just left a review on itunes for you! Hope it helps you out per your call to action an episode or 2 ago.

Appreciate it Kevin! Always motivating to hear supportive feedback to keep on going.

“long term investing” At my age “long term” is 5 to 8 years. Fortunately, I have made my money. “long term” shortens with age. There is freedom in this. When I make an investment decision which loses money, I don’t have to live with the consequences for 30 years.

Thirty years from now young investors will criticize themselves by thinking I knew I should have bought that stock 30 years ago, I knew I never should have sold my rental. A piece of advice. If those are the worst decisions you make in your life, you got off easy.

We recently bought a duplex. Because it is partly an investment property, the rates for a 30 year mortgage were higher than what is quoted in the typical figures for SFH. Banks ultimately offered us around 3.5% for a 30 year fixed and 2.875% on a 10/1 ARM, so we went with the ARM.

We made the upgrade from condo in Hayes Valley to single family home in Noe at the lower end.

We were remodeling to sell the condo when virus hit and were scared to put it in market until couple of weeks ago. But ton of inventory hit the market same time, and media did not help (SocketSite) We had a lower listing price and got it off hands quickly without waiting due to that.

We got the SFH in early June and there were 8 offers and we overpaid, it was on an ideal block. We were only able to buy it or justify buying it due to low mortgage rates.

Overall the flipping of condo should have paid off better than tech stocks in normal circumstances but return is similar now. It was a lot of work and stress doing remodel, as it was our first time. We never thought we would sell that property but dealing with HOA and renters wasn’t gonna work for us as we originally thought.

And now we have our own backyard but need to finish basement and start on a remodeling project all over again! The SFH is smaller than our condo and payments are 50% higher :)

Would love to hear your thoughts!

Great anecdote. Thanks for sharing. We’re in the East Bay and in a condo – trying to figure out if we keep it after an upgrade or sell it and upgrade. We have seen a robust market for SFHs but I don’t think things are as crazy as some would say (and it’s always been pretty crazy in the bay area anyway…). We’re very much of the “be fearful when others are greedy and be greedy when others are fearful” mindset, even though that seems to be out of style these days…

Good that you can add some value to the home – that is huge!

Hi Sam,

Been following you for many, many years. We own our own home. During this crisis we purchased a 6 unit building (off market) and closed March 20, 2020 with no problems other than signing docs, the bank was on board and so was Title….a few logistical hoops otherwise uneventful and got the signatures electronically…We have been remodeling (with contractors) doing leasing of two units through April and another remodel in May/w showing and Lease ups…Now starting another remodel of another unit…Not sure what everyone else is doing but the sky is not falling here. people are working and want to work, no tenant issues, all paying and on-time, and just common turnover of one unit. We are just plugging along build up assets and looking to buy more and rotate out of and step up with 1031’s…We are cautious when around big groups but we always have been. Common sense here. Oh, I we stopped listening to most of the news….Its getting out of hand…Retired in early 50’s from 30 yrs in aviation…We live between Denver and Boulder, and we buy in Loveland, Fort Collins and Greeley, Colorado Springs, CO. Keep up the great work! Cheers! Scott

Sam

Phoenix area is still very strong with low inventory under 500k in used homes. Houses go at list price or 1-3% below at most.

New homes in any range are still being built in great amounts and big developers like Shea are buying more land. They have brought back most of their sales force even though everyone is in masks. We are in the normal hottest and slowest time of the year due to heat but in real estate it is not slow.

All the trades are busy. Title and mortgage companies swamped.

You are correct: people are saying, “I am moving on somehow, someway!”

God Bless

Sam,

Great topic and timely – I’m a huge reader of yours and was at one point Leary of this market. Last year I negotiated my severance out of a bad work situation and am now using the partial windfall to investment in a home my wife and I negated a side deal with a seller who hadn’t marketed the home.

I think we are seeing an inversion with coastal property with lower inventory driving up prices in the highly desirable suburbs which are price immune. In the other part o the market here in NJ owners are holding out on selling so inventory is low. In the lower parts of the market where people cannot get mortgages due to income or other situation there is ample stock being bought up by investors.

I would agree with you having a place to live and buying for the next generation is key. Our daughter needs a nice home neighborhood to live and at the least with low interest rate I look at our new home as a family investment our chlldren and maybe grandchildren will own something in a nice town. After renting for 4 years, our patience has paid off!

From one toddler parent to another, Thanks for all that you do.

Best Regards,

Hey Sam,

Great content as always. The real estate market is super hot in Northern NJ, which is super annoying for us as buyers, ha!

It depends on the area ofc, but those particular ones with great school systems or favorable property tax rates are selling like hot cakes.

In the past month or so, most of the homes we visit have received multiple offers. Which means none of them are going below asking, and most of them going above.

What’s wild is that people are now OK with what the majority of people typically werent OK with before, such as being on busy main roads, being near power lines, etc.

Demand is increasing because of people leaving NYC and NJ cities for more space and COVID safety.

But we are still keeping it level-headed and only buying what’s worth our value. Don’t want to be stuck with an overpriced home.

Stay safe Sam.

Best,

AK

Sam- I feel a bit dumb now as our strategy to expand doesn’t seem so certain now. We bought a 1 bd condo in the city 2 years ago and had a kid last year. The plan was to buy a single family house this year and have our condo as a rental. However, prices in my current area are less than they were 2 years ago and lots of available units to rent.

Would it be wise to stretch our budget now and purchase another house, or to sell our current property at a loss and use whatever equity is left towards a new house? Thanks.

Nobody could have expected we’d be in this situation today, so don’t feel too bad about your strategy.

It’s tough to say. Taking on more debt now after taking a likely loss feels like unnecessary risk. Has it become untenable for 3 of you to live in the one-bedroom? That seems tough. On the bright side, it’s getting max utilization.

I’d first test out the rental market or see what comps are renting for.

I can’t really provide good guidance without knowing your full financial situation.

I don’t think stretching your budget with a newborn and a new mortgage (like a new born) is wise.

Thank you. Our place is definitely being utilized to the fullest, especially with no daycare now. It’s doable, but tough.

As far as rents, the average asking rent for a place like mine is the same amount as our monthly expense (mortgage, HOA, insurance, tax), but almost all of the listings have been sitting for weeks. At best, we’ll “break even” but since we live in the city (Santa Monica), renters are moving to cheaper areas once they assess their job situation.

We currently have about 3 years of living expenses in cash, which would be enough for a 20% down payment for the suburbs we’re looking at. Our debts are the mortgage and 15 months of car payments left, which is the equivalent of 6 weeks of cash flow.

One of the most stressful things you might experience is buying a new property with a mortgage, and waiting to sell your old property which also has a mortgage. If your finances cannot handle two mortgages concurrently for six months to a year, I wouldn’t buy first. I would sell first, negotiate a one or t One of the most stressful things you might experience is buying a new property with a mortgage, and waiting to sell your old property which also has a mortgage. If your finances cannot handle two mortgages concurrently for six months to a year, I wouldn’t buy first. I would sell first, negotiate a one or two month lease back and then hunt for your property.

It would be very inconvenient and also stressful to sell your property, have to move into temporary housing, and then buy another property. But then again, that’s better than carrying two mortgages at the same time in my opinion.

Congratulations on your little one! I know things are difficult right now. But what a blessing to have our children! And what an honor to protect and love them.

Our house is about 1.5 miles from the beach in DE in a community with about 240 lots, of which 230 are built upon. Due to the location (east of DC and south of Phila/NJ) prices aren’t cheap and this community is considered the best in the area. House prices are high in general and within the last 3 months they are flying out the door – even houses not marketed have sold. Houses that had lanquished have sold and even a lot that had been left untouched for 30 years sold.

My wife handles the updates for the HOA website and she just received the June/July ones and we were stunned. Normally 8-10 houses are for sale – as of this update there are only 2 not under contract. People are bugging out of the metro areas here on the east coast – or at least it seems that way. Some of these deals are cash. I don’t think mortgages are even a consideration given it is nearly free money and if you take inflation into account it might as well be considered such. We know a couple who came down from near NYC in late March and stayed for 3 months – and they are considering not going back even though the husband is a NYC boy thru and thru.

Great for those selling and if it holds we might even consider taking our money and running somewhere else.

We’ve been looking for a home for my daughter here in Sacramento and anything under $500k seems to be gone within 48 hours at over ask. I assume there is much more money out there than I expected despite the CV19 pressures on everyone. I also noticed numerous of these homes are previous rentals and the owners are getting out while the market is hot – that is probably saying something as well.

Sam,

Great topic and timely – I’m a huge reader of yours and was at one point Leary of this market. Last year I negotiated my severance out of a bad work situation and am now using the partial windfall to investment in a home my wife and I negated a side deal with a seller who hadn’t marketed the home.

I think we are seeing an inversion with coastal property with lower inventory driving up prices in the highly desirable suburbs which are price immune. In the other part o the market here in NJ owners are holding out on selling so inventory is low. In the lower parts of the market where people cannot get mortgages due to income or other situation there is ample stock being bought up by investors.

I would agree with you having a place to live and buying for the next generation is key. Our daughter needs a nice home neighborhood to live and at the least with low interest rate I look at our new home as a family investment our chlldren and maybe grandchildren will own something in a nice town. After renting for 4 years, our patience has paid off!

From one toddler parent to another, Thanks for all that you do.

Sam,

My Father In-Law works in a job that has been dramatically impacted over the past several months, and he has been struggling to meet his rent obligations. This has put a lot of strain on his marriage. My Mother In-law has never worked; and he is struggling to make ends meet alone while keeping their relationship intact.

After some discussions with my wife, we decided to purchase a home near us and it rent back to her parents at a small cash-on-cash loss. Providing a stable living situation they can afford is going to be a lot better for our family.

As we started researching our options, a mortgage broker informed us of the Family Opportunity Mortgage. This program allows us to purchase a 2nd home at the same rate as our primary residence for elderly parents who cannot qualify on their own. This is a powerful incentive. I’m curious now if I can purchase them a new house every year and accumulate a rental portfolio at primary residence mortgage rates.

Matt

Good to know Matt! I’ll look into this more. Glad your in-laws are getting support from you guys in this difficult time. Best of luck and fight on.

We just refinanced to a 20 year back in February at 3.29% and cashed out $25k. I of course did a no fee refinance… so we got a slightly higher rate but no closing costs. Now I’m looking to refinance again… but oddly the 20 and 30 years rates are being quoted the same 2.75% no fee rate. I was considering refinancing to a 30 year and paying it down like a 20 year. This way if we have a job loss if Covid gets worse… I have more wiggle room.