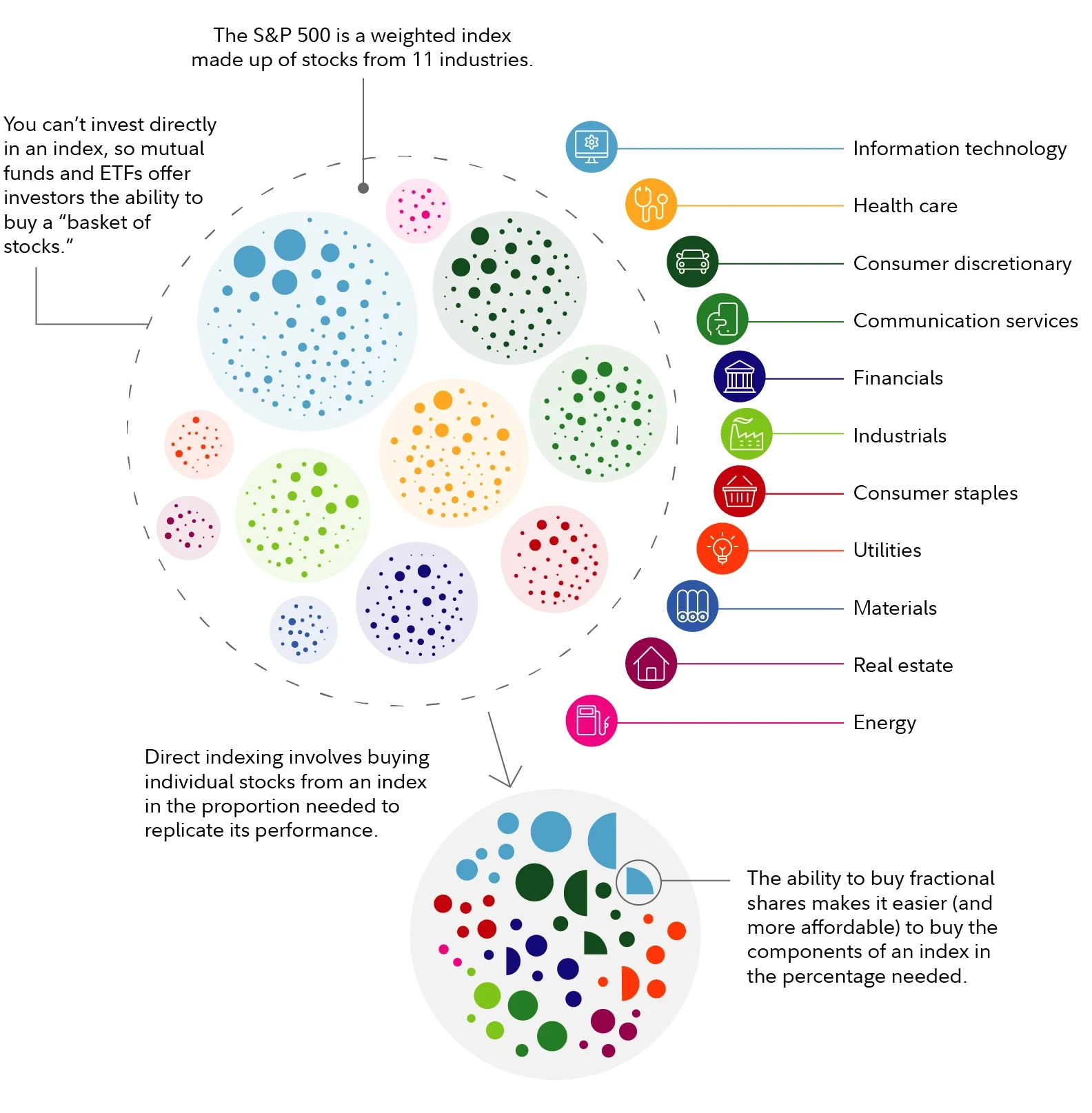

One of the investing strategies growing in popularity with the wealthy is Direct Indexing. Before my consulting stint at a fintech startup in 2024, I had never really heard of Direct Indexing. If I did, I likely assumed it simply meant directly investing in index funds, which many of us already do.

However, Direct Indexing is more than just buying index funds. It is an investment strategy that allows investors to purchase individual stocks that make up an index rather than buying a traditional index fund or exchange-traded fund (ETF). This approach enables investors to directly own a customized portfolio of the actual securities within the index, providing greater control over the portfolio's composition and tax management.

Let's look at the benefits and drawbacks of Direct Indexing to get a better understanding of what it is. In a way, Direct Indexing is simply a new way to package and market investment management services to clients.

Benefits of Direct Indexing

- Personalization: Direct Indexing allows you to align your portfolio with your specific values and financial goals. For example, you can exclude all “sin stocks” from your portfolio if you wish. It depends on how comfortable you are profiting from sin.

- Tax Optimization: This strategy offers opportunities for tax-loss harvesting that may not be available with traditional index funds. Tax-loss harvesting helps minimize capital gains tax liability, thereby boosting potential returns.

- Control: Investors have more control over their investments, allowing them to manage their exposure to particular sectors or companies. Instead of following the S&P 500 index managers' decisions on company selection and weighting, you can set sector weighting limits, for example.

Drawbacks of Direct Indexing

- Complexity: Managing a portfolio of individual stocks is more complex than investing in a single fund. Therefore, most investors don’t do it themselves but pay an investment manager to handle it, which leads to additional fees.

- Cost: The management fees and trading costs associated with Direct Indexing can be higher than those of traditional index funds or ETFs, although these costs may be offset by tax benefits.

- Minimum Investment: Direct Indexing often requires a higher minimum investment, making it less accessible for some investors.

- Performance Uncertainty: It's hard to outperform stock indices like the S&P 500 over the long term. The more an investor customizes with Direct Indexing, potentially, the greater the underperformance over time.

Who Should Consider Direct Indexing?

Direct indexing is particularly suited for high-net-worth individuals, those in higher tax brackets, or investors seeking more control over their portfolios and willing to pay for the customization and tax benefits it offers.

For example, if you are in the 37% marginal income tax bracket, face a 20% long-term capital gains tax, and have a net worth of $20 million, you might have strong preferences for your investments. Suppose your parents were addicted to tobacco and both died of lung cancer before age 60; as a result, you would never want to own tobacco stocks.

An investment manager could customize your portfolio to closely follow the S&P 500 index while excluding all tobacco and tobacco-related stocks. They could also regularly conduct tax-loss harvesting to help minimize your capital gains tax liability.

However, if you are in a tax bracket where you pay a 0% capital gains tax rate and don't have specific preferences for your investments, direct indexing may not justify the additional cost.

This scenario is similar to how the mortgage interest deduction was more advantageous for those in higher tax brackets before the SALT cap was enacted in 2018. Whether the SALT cap will be repealed or its $10,000 deduction limit increased remains to be seen, especially given its disproportionate impact on residents of high-cost, high-tax states.

More People Will Gain Access to Direct Indexing Over Time

Thankfully, you don’t need to be worth $20 million to access the Direct Indexing strategy. If you're part of the mass affluent class with $250,000 to $2 million in investable assets, you already have enough. As more fintech companies expand their product offerings, even more investors will be able to access Direct Indexing.

Just as trading commissions eventually dropped to zero, it’s only a matter of time before Direct Indexing becomes widely available to anyone interested. Now, if only real estate commissions could hurry up and also become more reasonable.

Which Investment Managers Offer Direct Indexing

So you believe in the benefits of Direct Indexing and want in. Below are the various firms that offer Direct Indexing services, the minimum you need to get started, and the starting fee.

As you can see, the minimum investment amount to get started ranges from as low as $100,000 at Charles Schwab and Fidelity to $250,000 at J.P. Morgan, Morgan Stanley, and other traditional wealth manages.

Meanwhile, the starting fee ranges between 0.20% to 0.4%, which may get negated by the additional investment return projected through direct indexing tax management. The fee is usually on top of the cost to hold an index fund or ETF (minimal) or stock (zero).

Now that we’re aware of the variety of firms offering Direct Indexing, let's delve deeper into the tax management aspect. The benefits of personalization and control are straightforward: you set your investment parameters, and your investment managers will strive to invest according to those guidelines.

Understanding Tax-Loss Harvesting

Tax-loss harvesting is a strategy designed to reduce your taxes by offsetting capital gains with capital losses. The greater your income and the wealthier you get, generally, the greater your tax liability. Rationally, all of us want to keep more of our hard-earned money than giving it away to the government. And the more we disagree with the government's policies, the more we will want to minimize taxes.

Basic tax-loss harvesting is relatively simple and can be done independently. As your income increases, triggering capital gains taxes—more advanced techniques become available, often requiring a portfolio management fee.

Basic Tax-Loss Harvesting

Each year, the government allows you to “realize” up to $3,000 in losses to reduce your taxable income. This reduction directly decreases the amount of taxes you owe.

For example, if you invested $10,000 in a stock that depreciated to $7,000, you could sell your shares at $7,000 before December 31st to reduce your taxable income by $3,000. You can carry over $3,000 in annual losses until it is exhausted.

Anybody who does their own taxes or has someone do their taxes for you can easily conduct basic tax-loss harvesting.

Advanced Tax-Loss Harvesting

Advanced tax-loss harvesting, however, is slightly more complicated. It can't be used to reduce your income directly, but it can be applied to reduce capital gains taxes.

For instance, if you bought a stock for $100,000 and sold it for $150,000, you would have a realized capital gain of $50,000. This gain would be subject to taxes based on your holding period:

- Short-term capital gains: If the stock was held for less than a year, the gain would be taxed at your marginal federal income tax rate, which is the same rate as your regular income.

- Long-term capital gains: If the holding period exceeds one year, the gain would be taxed at a lower long-term capital gains rate, which is generally more favorable than your marginal rate.

To mitigate capital gains taxes, you can utilize tax-loss harvesting by selling a stock that has declined in value to offset the gains from a stock that has appreciated. There is no limit on how much in gains you can offset with realized losses. However, once you sell a stock, you must wait 30 days before repurchasing it to avoid the “wash sale” rule.

When To Use Tax-Loss Harvesting

In the example above, to offset $50,000 in capital gains, you would need to sell securities at a loss within the same calendar year. The deadline for realizing these losses is December 31st, ensuring they can offset capital gains for that specific year.

For instance, if you had $50,000 in capital gains in 2024, selling stocks in 2025 with $50,000 in losses wouldn't eliminate your 2024 gains. The capital gains tax would still apply when filing your 2024 taxes. To offset the gains in 2024, you would have needed to sell stocks in 2024 with $50,000 in losses.

However, let's say you had $50,000 in capital gains after selling stock in 2025. Even if you didn't incur any capital losses in 2025, you could use capital losses from previous years to offset those gains.

Maintaining accurate records of these losses is crucial, especially if you're managing your own investments. If you hire an investment manager or financial professional, they will track and apply these losses for you.

Crucial Point: Capital Losses Can Be Carried Forward Indefinitely

In other words, capital losses can be carried forward indefinitely to offset future capital gains, provided they haven't already been used to offset gains or reduce taxable income in prior years.

During several years in my 20s, I was unaware of this. I mistakenly believed that I could only carry over a $3,000 loss to deduct against my income each year. As a result, I paid thousands of dollars in capital gains taxes that I didn't need to pay. If I had a wealth manager to assist me with my investments, I would have saved a significant amount of money.

While the ideal holding period for stocks may be indefinite, selling occasionally can help fund your desired expenses. Tax-loss harvesting aims to minimize capital gains taxes, enhancing your overall return and providing more post-tax buying power.

The higher your income tax bracket, the more beneficial tax-loss harvesting becomes.

Tax Bracket Impact And Direct Indexing

Your marginal federal income tax bracket directly influences your tax liability. Shielding your capital gains from taxes becomes more advantageous as you move into higher tax brackets.

For instance, if your household income is $800,000 (top 1% income), placing you in the 37% federal marginal income tax bracket, a $50,000 short-term capital gain from selling Google stock would result in an $18,500 tax liability. Conversely, a $50,000 long-term capital gain would be taxed at 20%, amounting to a $10,000 tax liability.

Now, let's say your married household earns a middle-class income of $80,000, placing you in the 12% federal marginal income tax bracket. A $50,000 short-term capital gain from selling Google stock would incur an $11,000 tax liability—$7,500 less than if you were making $800,000 a year. Meanwhile, a $50,000 long-term capital gain would be taxed at 15%, or $7,500.

In general, try to hold securities for longer than a year to qualify for the lower long-term capital gains tax rate. As the examples illustrate, the higher your income, the greater your tax liability, making direct indexing and its tax management strategies more beneficial.

Below are the income thresholds by household type for long-term capital gains tax rates in 2025.

Restrictions and Rules for Tax-Loss Harvesting

Hopefully, my examples explain the benefits of tax-loss harvesting. For big capital gains and losses, tax-loss harvesting makes a lot of sense to improve returns. I'll always remember losing big bucks on my investments, and using those losses to salvage any future capital gains.

However, tax-loss harvesting can get complicated very quickly if you engage in many transactions over the years. By December 31st, you need to decide which underperforming stocks to sell to offset capital gains and minimize taxes. This is where having a wealth advisor managing your investments becomes more beneficial.

For do-it-yourself investors, the challenge lies in the time, skills, and knowledge needed for effective investing. If you plan to engage in tax-loss harvesting, let's recap the essentials to make things crystal clear.

Annual Tax Deduction Carryover Limit is $3,000

- If you have $50,000 in capital losses and $30,000 in total capital gains for the year, you can use $30,000 in capital losses to offset the corresponding gains, leaving you with $20,000 in remaining capital loss.

- You can carry over the remaining $20,000 in losses indefinitely to offset future gains. In years without capital gains, you can use your capital loss carryover to deduct up to $3,000 a year against your income until it is exhausted.

No Expiration Date on Capital Losses

- If you have $90,000 in capital losses from selling stocks during a bear market and zero capital gains that year, you can carry those losses forward to offset future income or capital gains. Fortunately, capital losses never expire.

The Wash Sale Rule Nullifies Tax-Loss Harvesting Benefits

- A loss is disallowed if, within 30 days of selling the investment, you or your spouse reinvest in an identical or “substantially similar” stock or fund.

Losses Must First Offset Gains of the Same Type

- Short-term capital losses must first offset short-term capital gains, and long-term capital losses must offset long-term gains. If losses exceed gains, the remaining capital-loss balance can offset personal income up to a limited amount. For detailed advice, consult a tax professional.

Direct Indexing Conclusion

Personalization, control, and tax optimization are the key benefits of Direct Indexing. With this approach, you don't have to invest in sectors or companies that don't align with your beliefs. Nor do you have to blindly follow the sector weightings of an index fund or ETF as they change over time. This represents the personalization and control aspects of Direct Indexing.

If you're focused on return optimization, the tax-loss harvesting feature of Direct Indexing is most attractive. According to researchers at MIT and Chapman University, tax-loss harvesting yielded an additional 1% annual return on average from 1928 to 2018. Even if Direct Indexing costs up to 0.4% annually, the benefits of tax-loss harvesting still outweigh the cost.

The best way to avoid paying capital gains taxes is to refrain from selling. Borrow from your assets like billionaires to pay less taxes. However, when you need to sell stocks to enhance your life, remember the advantages of tax-loss selling, as it can significantly reduce your tax liabilities.

Direct Indexing offers a compelling way to optimize returns through tax-loss harvesting and portfolio customization. As tax laws become more complex and investors seek ways to align their portfolios with personal values, Direct Indexing provides a powerful tool for both advanced and everyday investors.

Free Wealth Management

Empower is the best free wealth management platform for investors. You can x-ray your portfolio for excessive fees and get a snapshot of your asset allocation by portfolio. Empower's free tools also let you easily track your net worth and plan for your retirement.

Think about Empower as a sophisticated version of Mint or an interactive version of Excel. I spent two years consulting for them in their San Francisco and Redwood City offices.

When there is so much uncertainty in the world, you absolutely must stay on top of your finances. Understand where your risk exposure is and stay on top of your cash flow. Empower's free tools will help you bring calm to the chaos.

Once you link your portfolio(s) that have at least $100,000 in assets, you can also get a free portfolio analysis session with one of their advisors ($799 value). If you wish, you can also hire Empower to manage your money for a fee. I've used Empower's free tools since 2012 to grow my wealth.

Diversify Into High-Quality Private Real Estate

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With around $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

I’ve personally invested over $400,000 with Fundrise, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009.

Good read Sam.

Two thoughts, first, I still don’t trust that direct indexing (DI) is really a winner over the long term (5, 10, 15, 20 years…). Certainly, results should only be compared on an after-tax basis, and I understand the tax savings can (perhaps SHOULD) be quite substantial (like I have heard numbers of 6%+), however, there is a lot to be said IMO for simplicity. Complexity opens the door to all kinds of execution risks, potential fee gouging/churn, and just simple errors. There is a lot to be said for a super low-cost passive index fund. Not sure where Warren Buffet comes down on direct indexing, even for the top 1% of “normal” investors. To me, DI sounds more like a theoretical optimization strategy, than an actual successful routine practice, and sometimes optimizing the last dollar is actually adding risk in return for very little gain.

Second, I don’t love conversations about capital gains taxes that do not also include discussions of the sneaky and not immaterial Net Investment Income Tax (NIIT). The ADDITIONAL 3.8% you have to pay for more or less being…..too successful?

I tend to balance my own tax exposure by investment location, like inside a 401k vs inside a taxable account. For taxable accounts, I just roll with muni income as much as possible, and forget about squeezing the last 2% out of every possible dollar. Keeps tax time a little more chill too.

Cheers.

My Schwab advisor also pitched their DI service as a way to aggressively harvest tax losses. I also worry about the complexity that might results from directly owning shares of so many different stocks. I am not sure how one can easily unwind the DI arrangement with the service provider.

I’d ask about the unwind. It’s easier than you think actually. Basket trading, pretty easy to unwind.

Hi Sam, just a clarification on the Empower Special Promo. Looks like this promo is only applicable for those who have not had prior account with Empower (and PersonalCapital). There may be a way to skirt around it, but just want to clarify.

Yes, you are right. If you are already a client, you should be having semi annual or annual check ups with a professional already.

I have used parametric dii now for 4 years – using the SP500 as the base index – because of the vol I have accumulated some strong losses that I will use in future circumstances. I am in the highest marginal tax bracket and a high state tax state – so the tax shield is real.

The main issue I have is over time the deviation from the index formation of the underlying positions gets larger over time and thus the potential for drift error becomes larger as u might miss out on those “losers” popping during the 30 day period or longer.

The idea of direct indexing is great but if you break up with the provider offering direct indexing it’s no fun. When your new provider reviews the portfolio they will have a slightly different strategy and will want to unwind certain positions. I was initially very excited about this but after changing brokerages a couple of years ago; direct indexing is a great way to capture a client. The clients portfolio becomes very complicated and difficult for the client to understand. It also means that the client can never self manage their portfolio again. I think a few index funds is still a better strategy.

Does the wash sale rule apply to selling stocks at a profit? For example, if I sell Google stock with a $5000 profit. Can I buy back right away or have to wait 30 days?

The wash sale rule does not apply when you sell a stock at a profit. You can sell Google stock at a $5,000 profit and buy it back immediately without any waiting period.

The wash sale rule only applies when you sell a stock at a loss and repurchase the same security within 30 days before or after the sale. In your case, since you’re selling at a gain, there’s no restriction, and you can buy the stock back right away without impacting your tax treatment.

More on the wash sale rule:

The wash sale rule is a tax regulation designed to prevent investors from claiming a tax deduction for a security sold at a loss if they repurchase the same or a “substantially identical” security within 30 days before or after the sale.

Here’s how it works:

If you sell a stock or security at a loss and then buy the same stock or a very similar one (like options or an ETF that tracks the same index) within 30 days before or after the sale, the IRS will disallow the loss for tax purposes.

The disallowed loss isn’t gone forever, though. Instead, it gets added to the cost basis of the repurchased stock, which affects your taxable gain or loss when you sell that stock in the future.

The wash sale rule is meant to stop investors from “harvesting” tax losses while still maintaining the same position in a stock. It only applies when selling at a loss; it doesn’t affect sales made at a profit.

So a little off topic, but how do robo-advisors such as Betterment, Weathfront, Empower, and Axos Invest get away with this? My experience using them is that they would sell on ETF at a loss and then buy another ETF tracking the same index sometimes in the same hour such as VTI and ITOT. The 1099 however doesn’t show a wash sale.

From my understanding each ETF is composed of different stock percentages so therefore it’s not exactly the same

Thanks for the intro! I had never heard of Direct Indexing until your post.

What are your thoughts on the future of Direct Indexing? Do you think it will disrupt traditional index funds and ETFs?

The future of Direct Indexing looks promising, especially as technology and personalized financial services become more accessible. Direct Indexing’s ability to offer tax optimization through strategies like tax-loss harvesting, along with customization based on personal values or investment goals, is attractive for high-net-worth investors today. As fees decrease and more fintech platforms offer these services at scale, I think Direct Indexing could gain significant traction even among retail investors.

However, while Direct Indexing may challenge traditional index funds and ETFs, I don’t think it will completely disrupt them. Traditional index funds and ETFs are simple, low-cost, and widely diversified investment vehicles that meet the needs of most passive investors.

Direct Indexing is a more complex and hands-on strategy, so while it will certainly grow in popularity, it will likely complement traditional funds rather than replace them. It’s more of a niche solution for investors seeking higher customization, especially those in higher tax brackets looking to maximize tax efficiency.

For those of you who prioritize ESG investing, how do you feel Direct Indexing compares to simply using an ESG-focused fund?

Great question! Direct indexing offers more customization compared to ESG-focused funds, which can be appealing for those who want to tailor their investments to specific ESG (Environmental, Social, and Governance) values. With an ESG-focused fund, you’re relying on the fund manager’s criteria for what’s considered ESG, which may or may not fully align with your personal values. Direct indexing, on the other hand, allows you to handpick individual stocks based on your own ethical standards—whether that’s excluding certain industries or focusing on specific sustainability metrics.

However, ESG-focused funds are simpler and generally come with lower fees, since they don’t require the same level of personalization and management. If you’re looking for a convenient, low-cost way to align your portfolio with ESG principles, an ESG fund might be sufficient. But if you want more control over which companies you’re invested in, and you’re willing to pay for the added flexibility and potential tax benefits (like tax-loss harvesting), Direct Indexing could be a better fit. It really comes down to how specific and hands-on you want to be with your ESG investments.

Sam – great info and very clear. How would this apply to margin interest? How can we use that to enhance tax deductions? Can you combine margin interest and losses to off-set capital gains and when you combine them are they still “forever” — meaning can be carried over year to year until exhausted? Enjoy your blog!

When it comes to margin interest, it’s deductible, but only against investment income, which includes things like dividends, interest, and short-term capital gains. So, if you’re using margin to enhance your investments, any interest you’re paying on that margin can potentially reduce your taxable income from investments. However, the deduction for margin interest can only offset up to the amount of your investment income in that same year.

Unfortunately, you can’t combine margin interest with capital losses to offset capital gains. They are handled separately. Capital losses can offset capital gains first, and if you have more losses than gains, you can use up to $3,000 to offset ordinary income (or $1,500 if married filing separately). The rest of the losses carry forward year after year until they’re exhausted.

Margin interest also follows a similar rule — if you can’t fully deduct the interest in one year because your investment income is lower than the interest paid, you can carry the excess interest deduction forward indefinitely to use in future years when you have more investment income.

It’s definitely a strategy to look into if you’re using margin and want to be as tax-efficient as possible! Thanks again for engaging with the content!

Direct indexing makes a lot of sense if the tax loss harvesting benefit can outweigh the cost. However, its hard to quantify the benefit of tax loss harvesting. Perhaps investment managers do a year and report highlighting how much their tax loss harvesting activities have helped improve returns.

They do

Hello Everyone – The comment system wasn’t working today, but it has been upgraded and is now working now. Let me know if there are kinks that still need working out. Thanks, Sam