It feels a lot like 2007 again. Almost every major asset class is on fire. People are leveraging up to buy things they don't fully quit understand. Investing FOMO is all over the place! Let's review why it feels like 2007 all over again so we can better protect ourselves.

Reflection helps us appreciate how far we've come. Reflection also helps us learn from our mistakes. I'd like everybody to reflect on several key items: Career, Finances, Health, Family, and Happiness. See if you can tie the five together and weave a story about who you are today.

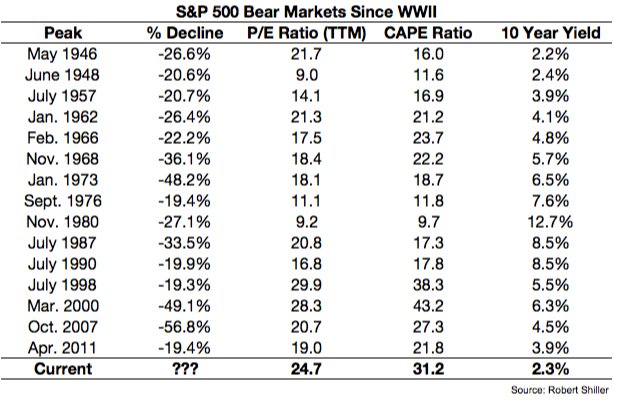

It's an exhilarating time with the S&P 500 over 6,000, a new all-time high. But it's also a perilous time for those who don't have perspective. Please don't go into major to debt to buy risky assets. Although it doesn't feel like another recession is coming, it always feels best before one does!

What Life Was Like In 2007

2007 was a most bubblicious time. Investors were feeling great! Let me go over what my situation was like back in 2007. Because just one year later, we had the 2008 – 2009 financial crisis.

Career in 2007

I was finishing up my third year as a VP at a large investment bank in San Francisco. 2007 was also the year I turned 30. Given my boss recently departed to become a client, I was left to take over the west coast business. Knowing my worth, I asked for a raise and a promotion and got them. If they lost me to a competitor, they would have been screwed for at least six months as they scrambled to find and train my replacement.

30 years old was a significant age because I finally felt like I could be taken seriously. Getting my MBA in 2006 also gave me a confidence boost. I was loving my career because I was finally my own boss in San Francisco. Sure, I had to work with the head of the office and a more senior colleague in a different department, but for the most part, I was free to control my own schedule. So long as the business was coming in, nobody could complain.

In 2007, I thought I could easily work for 10 more years and then call it quits for good. Little did I know the financial crisis would crush my industry and cause me to pursue a different path just four years later.

Thoughts for today: If you don't love your career, you better get paid. Otherwise, you're wasting your time. There are so few careers that truly provide meaning. Find something worth doing.

Finances in 2007

I received the biggest bonus of my life in 2007 due to a negotiation I had with my big boss in Hong Kong. It was a handshake agreement, so you never know until the end of the year when bonuses are paid. But he delivered as promised. From that day on, I decided to be loyal until the very end.

Although the stock market was booming, I was still hesitant to go all-in due to the dotcom bubble that began to collapse in 2000. Instead of investing everything I had in the stock market, I decided to invest most of my savings in real estate. At least with real estate, if all went to hell, I'd still have something to sleep in.

I bought my first SF property in 2003, lived in it for two years, and was renting it out to a couple in 2007. In 2005, I decided to take out a $1,200,000 mortgage and buy a single family house in the Marina district for $1,523,000. It was the cheapest house for its size in the neighborhood because it was on a busy block next to the busiest street.

Then I Made A Big Financial Mistake In 2007

Because my real estate investing experience was positive, and I had just received a big bonus, I decided to buy a $718,000, 2/2 vacation condo at The Resort At Squaw Creek, Lake Tahoe in 2007. I loved the place because that's where I took my girlfriend on our first getaway date back in 2001.

I was delirious about my financial luck and felt I just couldn't lose. In my mind, my compensation would continue to grow by 10-20% a year for the next five years. Improperly forecasting your future income is one of the biggest financial sins of all!

There were some warning signs about the stock market and real estate market getting ahead of themselves, but I didn't listen carefully. Instead, I myopically focused on my fortunate career situation. I wish someone with decades of experience sat down with me to run through the pros and cons of buying more property then.

Thoughts for today: As soon as you reach your financial target, the target will move. The desire for money is a never ending process until you decide how much is enough. Don’t just make money for money’s sake. Have a clear purpose. Personally, I want to enjoy my wealth today. As a result, I bought a forever home to take care of my family. The best time to own the nicest house you can afford is when you have children still living with you.

I think real estate is going to do well in 2025 and beyond because the Fed is cutting rates. There's also pent-up demand and a new president Trump, who comes from a real estate background. He will be focused on taming inflation and reducing mortgage rates.

If you'd like to invest in real estate without the hassle, check out Fundrise. Fundrise offers various private real estate funds to invest in residential and industrial real estate passively. I've personally invested $150,000+ in Fundrise real estate so far.

Health In 2007

Work was stressful given the 60-70 hour work weeks. But at least my chronic back pain from 2000-2003 was gone. But what replaced my chronic back pain was teeth grinding and TMJ. It hurt to speak for more than an hour. I remember paying $700 to a specialist dentist who ground down parts of my molars so I could get some relief when I closed my jaw.

I was in OK shape because I started aggressively playing tennis again. But of course, I suffered from occassional tennis elbow pain that kept me from swinging freely. I weighed between 162-165 lbs, which was a normal weight for someone 5'10” tall.

Now when I look back on my diet, I realize I ate extremely unhealthy due to frequent client entertainment. I'd often take clients to fancy steak restaurants and nice lounges. The wagyu beef and Moscow Mules tasted especially good thanks to a corporate card with a $200/head budget.

I remember telling myself that no matter what, living in San Francisco was healthier than living in Manhattan.

Thoughts for today: The Health Benefits Of Early Retirement Are Priceless. It's easy to forget how much of our health we sacrifice for money and prestige. But living a pain-free and healthy life is worth it. I’m about 168 lbs now, but still fit into the same clothes from 20 years ago. In addition, I still have all my hair and it's all black.

Family Situation In 2007

My girlfriend graduated college in 3.5 years and came out to live with me in December 2001. She was 27 in 2007, and I was unsure whether starting a family was a good idea yet. Work was extremely busy and I had all this pressure to keep the ship afloat given my boss left.

But I knew she was the one, so I proposed during the heart of the financial crisis in 2008. We got married in Hawaii in December 2008.

If the financial crisis didn't hit, I would have been more confident to start a family by 2010. It would have been nice to get parental leave and company benefits. Further, since our son is the best thing that has ever happened to us, he would have been in our lives for seven years longer.

It's so difficult to figure out when is the best time to have children. Even if you decide now is the time, it might take several years to conceive.

What I do know is that having a life partner through my entire post college journey has been priceless.

Related: When Is the Best Time To Have Children? A Physical And Financial Decision

Thoughts for today: Nothing comes close to having a family and spending time with loved ones. There is no way I'd ever take a full-time job over time with my family. Even the most meaningful job doesn't come close, yet most jobs are pretty meaningless. You can never get the time you missed away from your family back.

We currently have two young children and I'll be damned if another financial meltdown makes us have to go back to work. We want to spend as much time with our kids as possible until they go to school full time.

Happiness In 2007

I was ecstatic about getting a raise and a promotion. Part of my happiness stemmed from having gone to public high school and public university. Never in my wildest dreams had I thought I'd have a job at a respectable investment bank and earn a healthy income. If I had gone to an elite private school, I'm not sure I'd be as happy because I would have expected all these things and more.

It's funny, but the memories that stands out most from this time period were figuring out what ring to buy and the cozy little wedding on our favorite beach in Hawaii the next year.

My happiness level has never really fluctuated much since graduating from college in 1999. It's always been about a 7-8 out of 10. The happiness of getting recognized at work only lasted for maybe three months. The pressure to deliver took over.

Thoughts for today: If you're relatively happy no matter how much you have, then it's not worth sacrificing once you've reached your financial goals. The same thing goes for thinking you’ll be happier once you have more money. Happiness does not come from money. Please, know this to be true. Focus on improving your health and relationships.

Our ultimate goal is to live a purposeful and happy life. There is certainty a happiness conundrum many of us face, where we have so much yet are still unhappy. Therefore, I think maintaining happiness and raising happiness takes consistent work.

Life in 2025 And Beyond

The most important thing I learned from 2007 is thinking that I couldn't lose, and then losing big when the financial crisis hit in 2008. I remember swearing to myself in 2010 that if my investments ever came back to pre-crisis levels I would take some money off the table. I tried to do so in 2012 by selling my primary residence in order to pay off a ~$1,000,000 mortgage and live in a small two bedroom, one bathroom apartment. But nobody wanted to buy my four bedroom house.

The difference with 30 year olds in 2019 versus my 30 year old self in 2007 is that I went through the dotcom collapse in 2000. I saw paper millionaires end up with nothing within a couple years. They had to start all over, like the guy who made my breakfast croissant each morning. 70% did my analyst class was fired too. As a result, I tried to diversify as much as possible.

It's hard to really know how scary recessions can be if you've never been in one with significant money at stake. Everybody likes to say they'll hold on to their investments and buy more during a downturn. But when your investments are down 30%+ and many of your colleagues are getting fired, the first thing you do is think about survival, not dumping every last cent you have in the stock market.

I'm praying that I'll finally be satisfied with what I have today and no longer grind as hard. My health depends on it. Staying in San Francisco and being surrounded by so many success stories has finally taken its toll. My recent bout of chronic back pain reminded me not to forget the point of financial independence and owning a lifestyle business: a better life.

Some Final Thoughts On The Previous Peak

* It's easy to extrapolate explosive growth in your career and net worth in a bull market. The problem is, nobody wants to work forever and things always change. Be more conservative with your expectations. Don't confuse brains with a bull market.

* No matter how much money you make or have, your steady state of happiness won't really change. Stop thinking that if you get to X amount you will be happy. Retire by a certain age, not a financial figure. There will always be something that will make you feel bad. The good thing is, you'll likely revert back to your steady state.

* If you're relatively young (under 40), it's worth swinging for the fences during the good times with growth stocks. It's worth allocating some funny money to chase unicorns. Once the spigot shuts off, dumb ideas no longer get funded and silly job offers are no longer given.

* Learn when to cash in your chips by setting goals. You made these goals because you decided how much was enough. If you've somehow found yourself way beyond your goals, then absolutely focus on using your profits for a better life. The saddest thing is losing a massive lead or having to start over. Turn funny money into real assets like real estate.

* Even if you buy at an inopportune time, if you wait long enough, you'll likely get back to even. Just look at us now.

* The next 10 years will go by faster than the previous 10 years. Make the most of it.

Recommendation To Build Wealth

Sign up for Empower, the web’s #1 free wealth management tool to get a better handle on your finances. You can use Empower to help monitor illegal use of your credit cards and other accounts with their tracking software.

In addition to better money oversight, run your investments through their award-winning Investment Checkup tool to see exactly how much you are paying in fees. I was paying $1,700 a year in fees I had no idea I was paying.

After you link all your accounts, use their Retirement Planning calculator that pulls your real data to give you as pure an estimation of your financial future as possible using Monte Carlo simulation algorithms. I’ve been using Empower since 2012 and have seen my net worth skyrocket during this time thanks to better money management.

Diversify Into Real Estate

Real estate is a core asset class that has proven to build long-term wealth for Americans. With stock market valuations at nose bleed levels, I would diversify your investments into real estate for less volatility and more steady income. Real estate is a tangible asset that provides utility and a steady stream of income if you own rental properties.

Fundrise: A way for all investors to diversify into real estate through private real estate funds. Fundrise has been around since 2012 and now manages over $3.2 billion for over 350,000 investors. The company focuses on Sunbelt residential and industrial real estate, which is going through positive structural change.

CrowdStreet: A way for accredited investors to invest in individual real estate opportunities mostly in 18-hour cities. 18-hour cities are secondary cities with lower valuations, higher rental yields, and potentially higher growth due to job growth and demographic trends.

I've personally invested $954,000 in real estate crowdfunding across 18 projects to take advantage of lower valuations in the heartland of America. My real estate investments account for roughly 50% of my current passive income of ~$300,000. Both platforms are long-time sponsors of Financial Samurai and Financial Samurai has invested over $270,000 in Fundrise.

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Your shares, ratings, and reviews are appreciated.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009. Everything is written based on firsthand experience and expertise because money is too important to be left up to the inexperienced.

FB, Twitter have very poor leadership at each place. I am surprised they do as well as they do. The lack of leadership at these entities is bad. We have 2 year olds that got super lucky with a unicorn. Does not mean they know what they are doing. The 2 CEO’s are not worthy of their positions. They are squandering the trust and good will they once had. Look at what happened to the iconic, unsinkable Sears. When they took the trust of their customer base for granted- the once almighty Sears is shuttering stores across the USA.

Listen to Stephen Mnuchin predicts 3% GDP for next couple years. Love this guy…steady and pushes through in spite of the garbage thrown at him every day by the naysayers. I will listen to him all day long before the losers going after him in the press like NYT Krugman who site in Ivory Towers and have never run an actual business. Never listen to anyone who has not run a business successfully.

Mnuchin (who walks his talk) says we are on track for a wonderful, sustainable recovery once we get fair balanced reciprocal (key word) trade agreements in place.

Please Sam consider going to other booming prosperous cities and get out of the super depressing mess in the Bay area. The prosperity and optimism in other places will lift you.

As an entrepreneur….I would suggest more tax friendly locales for your business.

California lawmakers punish success in business at every level. Again, Sam thank you for your columns and food for thought. I look forward to your columns all the time. All the best.

Sam very much appreciate all you do and all your advice. Do not agree at all that this is like 2007. Think the doomsday thinking is not warranted at this point.

People always take profits at new highs….totally normal to see a dip at the “top” with good news

FB, TW and other FANG tech stocks are setting themselves up to be regulated due to scandals. Not surprised they are down.

Trump whether you like him or not- is re-regulating the trade contracts with multiple countries. EU just “gave in” to the tariff issue. We will see what happens with other countries. This had to happen. Things were too out of balance and there was no reciprocity for USA companies.

I do not want my personal info published or out there. I just think you have good things to say. I deeply admire what you are trying to do on your own as an entrepreneur but very much disagree with you on these things.

We will always have ups and downs but calling for doomsday scenario akin to 2007 – when things are so different is not good. San Francisco may feel like it is collapsing because it is- with the crazy out of control democrats there. Go other places that are absolutely booming and prospering and you may see things differently. I know you do not like Texas (sadly) for some reason….but if you go to Dallas- you have never seen such prosperity and optimism. Go to Plano north of Dallas – corporate headquarters from all over USA are moving there. Things feel fantastic.

I lived in CA for 15 years and completely understand why people there must feel it is 2007. Your state is being over-run with an out of control government (democratic). I am so sad to see this. I always wanted to have 2 places…one in Tx and one in CA. Now- not so much. After living in Tx- looking back- I could not see the abusive ways of the govt until I saw how good Governor Abbott and Texas politicians are (in general- also Republicans)

In CA, too much crime, state taxes are way out- of- control, profligate waste in govt., encouragement of illegal migration when we have so many USA citizens that need help now. We do not have enough resources now for our own citizens…and they encourage more burdens on the overwhelmed systems. “The rich” are tapped out and are doing their own personal “tax inversions” by moving out of CA. That is going to make it worse for the middle class. Who else is going to fund the ballooning out-of -control spending on pensions and entitlement programs….no one by you and others like me with decent jobs…..to pay the high taxes. I could never go back to CA except to visit. After you see good thing and prosperity….it is very hard to look at the mess that is sadly my beloved CA.

I think a lot of your “2007” thinking is because you are there in CA. CA is going to go over a cliff financially and I agree with your 2007 in terms of CA. I do not agree that other states are in the same mess. I travel all over the lower 48 states for my job. CA, NY, IL, CT are an absolute mess. So sad. Go to Dallas and go to Plano. It will blow you away – night and day- in terms of optimism and prosperity everywhere. There are issues…but nothing like CA and nothing like the beloved Bay area.

This message is mostly for Sam- because I deeply appreciate what he is trying to do. I want him to be super successful. I have told my nephew to watch what Sam does closely and try to emulate this….but not on this point. Thank you for all your wonderful posts and all you do!

Thanks for your thoughts! I have several investments in Texas right now. Check out this post: https://www.financialsamurai.com/focus-on-investment-trends-why-im-investing-in-the-heartland-of-america/

Please STOP talking about Texas as if it’s some kind of Utopian dreamland. Once people get slapped with a $43,000 property tax bill and experience their first endless 100+ degree summer (along with 95% humidity and $800 monthly a/c bills), reality hits that it isn’t that great.

Plano is flat and ugly, Richardson is urban sprawl with endless acres of track homes that all look the same with no trees or relief from the heat. Meanwhile in Dallas, crime is rampant due to an understaffed police force, drugs are a huge problem, and the homeless population is beginning to rival California’s. And all of this while sitting in the most horrifying traffic that you’ve ever seen, among the most angry drivers you’ve ever dealt with. Going to the DMV takes hours, completing simple local administrative government activities turns into an entire day of wasted time…there’s soooo much more.

It is NOT an easy place to live and it is NOT for everyone. Stop trying to sell “Texas” to people. Ugh.

Sam,

Your love of family over money is what I love most about your ideas. In 2007 I had just inherited about 3 mil. I am down to about 600k in assets. age 62 with MS. 1 son. 3 grand kids 2 with special needs. I just emptied my stocks at a good time to invest in a house to be close to kids. my son is single dad. Am I scared? Sure, I am. But thru these down turns I haven’t been able to get a lot of income. I always had to keep a high reserve of cash so wouldn’t have to sell on down turns. I loaned out money to individuals using their homes as security. that was the best passive incomes. I only have one left maturing in 2021. I could have been less giving to my family. My son has struggled because of his bad decisions in his early 20’s. Now he’s on the right path. I am hoping for the sale of one of my properties at the end of this month as I took cash to buy the house down the street from his. Its looking good for a closing. I just don’t know what to do with that cash of about 250k when I get it. I have gifted him 100k for his home, so he could afford to get a mortgage and we can live in a nice middle class area on the same street. No, we could not live together. I need some private time for my life. I would like to see the 250k bring in a 4% return . I don’t worry about the tax consequences at this time. And yes, I would do most of it all again, with just a few wrinkles ironed out…hindsight is 20/20

Thanks for sharing. What were some of your mistakes that you made is $3 million is a nice sum of money.

I wouldn’t be in a hurry to reinvest your windfall of $250k. I would sit on it for three months and carefully choose your investments and think about your liquidity needs.

Mistake 1 is it was inherited and I had very little preparation to know how to manage it or the people around me. Mistake 2 was in trusting a smart guy, that had been a long time friend to manage it. I had to fight a very large bank to get it away from their mismanagement. that took a lot of the funds. fighting yourself only pays attorneys. but I won. Or rather the attorneys and accounting firm won. Then the nice guy used it due to the wording of the original trust that allowed the trustee to invest as they wanted. it was mostly a GST and POD accounts. Mistake 3 not knowing about what you call stealth wealth. Other than that, I would still have helped out everyone I did. Even the small 500.00 loans that friends never paid back. And I wouldn’t have given my Ex a dime. I did, but wasn’t legally necessary as it had been inherited and I had managed to save him a good size retirement fund over the years. In my state inheritance if kept separate isn’t included as marital assets to be divided. I shouldn’t felt sorry for the him. He left as soon as his 20 years was up and my parents were dead. looking back, I think he was just waiting. Now i practice stealth wealth, and read your blog. I think I’m inclined to go with your suggestion and not be in a hurry to reinvest. my interest is piqued by Realty shares you talk about. That seems like a replacement passive income without the tenants. and I like the money I made in YY and tencent before I had to put cash on this place. I was lucky enough to have a great friend that is a CPA so she has guided me well on the tax end of it. I wish I had the business acumen that was taught to my older brother. I didn’t have any training because I didn’t know my parents were worth that much. He did as he was involved in their businesses. I was a happy mushroom. I do love your blog and sorry your over worked. I understand your wife not knowing about the finances. I always handled it for my husband and I. he only earned 48k a year, but I managed to save 25%. I think he’s blown thru it by now. I knew how to save, I never needed much.

I remember 2007 very well – I had most of my wealth – 90% of it in the stock market. I remember thinking then, can it get any higher? Still FOMO made pull back from selling, I figured I had enough cash to ride out any downturn. Still watching my investments go down 50% was a huge lesson. I had read “The intelligent Investor” but not followed its advice to maintain ratios of cash, bonds and stock – I was basically all in stocks. I didn’t like selling then and I didn’t want to pay the taxes. I had a lot of money saved, but was not making a lot of money from my work.

I learned my lessons – the stock market is doing great, so I’ve been selling. I still may have too much in perhaps at 75% in index funds, but I’ve been disciplined about selling when my ratios get out whack. I’m just a little sad that I have to pay taxes on money I may never use unless there’s an emergency.

Great post, Sam. I remember 2007 and 1999 both very well, and the euphoria that prevailed then. With a dividend stock-heavy portfolio, I have more than a 20% gain this year, and this was on top of a 13% gain in 2016. Even the tax reform has baked into the market valuation now, and with many valuation ratios in the 99th percentile or higher, I am wary now. I think it is prudent to take some (or most) of the chips off the table and re-enter sometime next year. Yes, there is opportunity cost and risk of missing the mad run-up that may still happen prior to the crash, but for those who have “won the game” with a sizable portfolio and have seen the previous crashes first hand, this may be a sensible move. For a young 20’s or early 30’s guy/gal with a long runway to retirement, staying invested is still the right move as they can recover easily. For a late 40’s or 50’s guy with the best earning years behind him, it will take painfully long to recover even from a 20-30% loss on a 7-figure stock portfolio.

I remember the early winter of 2009 very well. Talk about scary ! Here I was ,33 years old running my newly founded timber brokering business. It was the first time in my entire career ( up until that point and ever since) that you couldn’t sell raw logs to any mill…anywhere. No one would take them. Everything came to a screeching halt. With a fledgling business my assets and free cash were non-existent. It was beyond terrible. The only thing that saved me and my wife from homelessness was the fact that we exchanged rent for care-taking on a palatial estate. We ate a lot of pasta that winter.

To say that the recession changed my life for the better, is an understatement. My income dropped by 2/3rds as I was in sales and my divorce left me with ZERO retirement. So I said screw it, quit my job in 2009 and started my own company. Now, my house in San Jose is paid off, I make several six-figures, and I figure I have two years left to retire at 55.

When you have not much left to lose, you can jump in with both feet

Amazing Patrick. Nice job battling back! I do enjoy that feeling of having not much left to lose, which is why I like to start new endeavors. The thrill of the upside is exhilarating. Enjoy the next two years! And try to be more conservative with your finances now that you’re so close to the finish line.

2007:

Career:

I had just started working at a major consulting firm in NYC. It was my first real job post-school. I had almost no professional experience going in and I was excited and nervous. Excited to learn a lot of new skills, nervous about keeping up given that I had no business experience. Late at night, after long office hours in front of Excel and Powerpoint, I studied for the CFA exams to increase my business/finance knowledge and, hopefully, build career optionality for later. When the financial crisis hit, it was a stressful time at my firm but I survived it. After a couple years, I’d had enough of NYC and moved out to the Bay Area, where I’ve been ever since.

Finances:

In 2007, I think I had $40k saved in a Roth IRA and that’s it. My net worth was negative because of student loans though. I didn’t know anything about investing and had bought several oil mutual funds, which got completely hosed during the financial crisis. I lost more than half those meager savings in the fall of 2008. That stung bad and made me internalize it’s better to invest in passive index-tracking funds if you’re not a very serious public equities investing professional.

Health:

I had no notion of how to live/eat healthy. I was working really hard, didn’t exercise much (which I regret now), and often ate expensive but not very healthy takeout dinners on the firm’s dime after long working hours. (I never want to do that again.)

Family & Happiness:

I didn’t have my own family or even a significant other. It was all work and I didn’t invest nearly enough time back then meeting new friends or dating. I regret this now because I don’t have that many warm friendship memories from that time. And even though I had an abstract understanding that it takes real effort to build new friendships and relationships, and they don’t just happen on their own, and ignoring this aspect of personal life would mean that, later on, the pool of potential compatible mates/friends would shrink, I didn’t appreciate concretely enough how this might impact my happiness either back then or 10 years later. To be sure, I don’t know what life would look like now if I had prioritized work less back then and personal relationships more (for all I know, I might not have been happy 10 years later for other reasons), but what I do know is that 10 years ago was a fairly lonely time and I wish I had somehow found a better balance and spent more time just enjoying my late 20s and early 30s, building more connections and friendships and memories and stressing less about always trying to prepare for the “next thing.”

2017:

Career:

Half a dozen jobs later, having worked across several industries (consulting, PE, tech), I’ve learned it doesn’t necessarily get easier as you get older: you just become better equipped to handle new challenges. I’ve also internalized more than ever that companies and roles are never stable, you shouldn’t ever rest on your laurels (until you financially never need to work again), and the best way to maximize optionality over the long run is to keep investing in your skills, relationships, and general/industry knowledge. I now work in the tech industry, where there’s a lot of “creative destruction” and companies individually are not stable (but well-paying jobs as a whole in the industry ARE pretty stable and plentiful). I’m not sure I’ll stay in this line of work forever, but it’s a good skillset to have and is transferrable to many other things.

Finances:

These days my finances are more stable because I’ve had a decade of earnings runway and I’ve lived frugally during this time. Importantly, I also found a spouse who is aligned in terms of financial values. While I still do not feel totally financially secure, I believe we’re on the right path, we’re building passive income streams to diversify away from our jobs, and we have a real pathway to achieving our dream of early-retiring in Hawaii. Maybe we’ll see you there someday!

Health:

I have to give most of the credit on health matters to my wife. Before I met her, I ate poorly and didn’t take good care of myself. I still don’t do a great job, but she creates more balance because she ensures better nutrition in our diet. Since she is a healthcare professional, she’s also more OCD about health matters, which I appreciate, since I’m not as on top of this as she is. Now I just wish we both had more discipline about getting regular physical exercise…

Family & Happiness:

I’m definitely more content now than I was 10 years ago. Less ambitious, but more content. I feel lucky about the major things in my life. Thankful I met a wonderful spouse and we are a great team together and support each other lovingly. Thankful we both got good lifelong educations, are both healthy, have good work/saving habits, strong/resilient professional skills, and got our fair share of lucky breaks in life. Even though we weren’t born into families of means and probably won’t ever be among the super-rich in our lifetimes, we’ve learned to build wealth, financial and otherwise, with our own hands. We are content with what we have and we’re happy.

Several commenters have mentioned the feeling of standing on the edge of a cliff, waiting for the impending market drop.

I feel the same way. I find myself now daily checking the ups/downs of all the Vanguard and other funds my various accounts (three 401(k)s and one deferred compensation account) are currently placed in.

I’ve been worrying about this since late last year. Each time an account dips 6K or 10K, I think I should have already shifted everything into a bond index fund or a “2020 retirement” fund or something else relatively safe from an equities crash.

Then a few days or a couple of weeks later they creep back up and hit another all time high, and I’m glad I haven’t yet pulled the trigger.

But it is worrysome. 3 of 4 are flying at +23% YTD (my wife’s 401(k) has crappy options and is only around +15% YTD). Every week I think about pulling out into something safer, but haven’t, yet.

Thanks for the thought-provoking post, Sam.

In 2007 I was in high school and was aware of the stock market but didn’t know much about it. I always thought it sounded interesting and since I grew up in a rural area I found NYC intriguing.

10 years later I’m working as an equity analyst in NYC. I have kept a large chunk of my savings out of the stock market to diversify my investment risk away from my career risk.

My theory on the market is that everything is becoming so complex that people just want to invest in stories and themes. It’s too difficult to follow every small piece of news (because there are thousands of sources these days) so people focus on high level themes. And as long as these growth stories continue to deliver, people will keep buying them up. Valuations will continue to be irrelevant, until a given theme starts to change.

The one caution I would call out is emerging markets growth. A lot of US companies are putting up strong growth numbers that are bolstered my huge growth in Asia. If that changes for some reason, valuations will start to matter again. This could be the catalyst, in my opinion.

I like your points on happiness stemming from your expectations. I also went to public schools and I never thought I would work in investment banking or stock picking in NYC. And It’s noticeable to me that I appreciate it a lot more than others who were groomed for this from the start. I think it also makes me more willing to give it all up once I’ve hit my goals. Since I was raised outside of this world, I know what it’s like on the outside. To private schooled kids the uncertainty can be a lot more intimidating.

Great wrap up of all the life lessons you learned in the past decade. It’s so true that when times are good, it’s easy to forget that you have to hedge for bears as well as bulls. As humans we tend to think good times will last forever when things are going up, and that recessions will also last forever whenever everything is plummeting. But in reality, nothing goes up forever and nothing is bad forever. It’ll be okay in the end. If it’s not okay, it’s not the end.

Congrats on discovering the real meaning of life–friends, family, and having enough.

I found Financial Samurai relatively recently and want you to know how much I’ve appreciated your articles and information. You stay on top of relevant recent financial topics, while also touching back on fundamentals. In addition, your posts have personal relevancy for me (and others in similar situations). Thank you!

Super interesting article. In 2007, I got my first salaried job and was very excited to start investing in my 401k. I was training for a marathon so my health was great. I was dating a really great guy. I was happy – I had everything I could want.

In 2017, well I have 50x the money I had in 2007. I’m in a different career. My health is probably the same. I’m single. I really try to be happy.

Hmm I thought this would be a more triumphant comment. I will have to think about how to put a better spin on this. Maybe it’s just less impressive because I was doing ok in 2007?

Not sure. The only hint I have from your comment is “I’m single. I really try to be happy.” 50X more money is HUGE! Congrats on that front.

Perhaps your comment is another example explaining how money doesn’t buy happiness?

One of my main points in this article is that family is BY FAR so much more valuable than all the money in the world.

Sam,

Your love of family over money is what I love most about your ideas. In 2007 I had just inherited about 3 mil. I am down to about 600k in assets. age 62 with MS. 1 son. 3 grand kids 2 with special needs. I just emptied my stocks at a good time to invest in a house to be close to kids. my son is single dad. Am I scared? Sure, I am. But thru these down turns I haven’t been able to get a lot of income. I always had to keep a high reserve of cash so wouldn’t have to sell on down turns. I loaned out money to individuals using their homes as security. that was the best passive incomes. I only have one left maturing in 2021. I could have been less giving to my family. My son has struggled because of his bad decisions in his early 20’s. Now he’s on the right path. I am hoping for the sale of one of my properties at the end of this month as I took cash to buy the house down the street from his. Its looking good for a closing. I just don’t know what to do with that cash of about 250k when I get it. I have gifted him 100k for his home, so he could afford to get a mortgage and we can live in a nice middle class area on the same street. No, we could not live together. I need some private time for my life. I would like to see the 250k bring in a 4% return . I don’t worry about the tax consequences at this time. And yes, I would do most of it all again, with just a few wrinkles ironed out…hindsight is 20/20

In 2007, I was 50 and now in 2017, just turned 60 in October. Lot’s of changes during this 10 year period. In 2007, our daughter was 9. Now she is 19 and in her Freshmen year in college. In 2007, I was deep into the corporate world as a senior level sales executive. Now, I’m retired and on to a second career as a budding Entrepreneur. In 2007, out Net Worth was about 3.5M and we were aggressively saving and investing. Now, it is just over 9M and I’m focused on how to “preserve and protect” and what to do about the pending tax implications of our tax-deferred investments. In 2007, I was very focused on myself and our success. In 2017, I’m much more focused on how I can give back and help others. I’m also working on a better balance in my life around faith, family, fitness, volunteering, mental/emotional changes, and overall outlook on life, etc.

We/ve been very blessed over the last 10 years and I hope the next decade is just as good or even better. It certainly will be different!

Loved this article! I quit my job a couple of weeks ago and will be going to another one soon. This time off helped me think about my next target and sure thing, early retirement it is. The reason for deciding to retire early is spending more time with my daughter and wife, living a healthier life. Now it is more or less clear to me what financial steps I need to take to secure my early retirement.

This article resonated a lot with my thoughts. Thank you, Sam!

Vahan

Great read! Many takeaways for me. But I think the best is the adage “Don’t confuse brains with a bull market”

10 years ago I was closeted and had just taken a second job to pay for the cost of applying for grad school. I was living in a crappy apartment with my best friend at the time in a small town I liked. I had less than $500 in the bank. No investments. Now, I have my second degree and a business doing work I value highly for the good it brings the world. Now I have an IRA and am working on getting out of educational debt. I am living my life in a city I love and openly as a lesbian. All of these things make now so much better for me than then. I’ve learned a ton about PF and am actively pursuing more knowledge so that I can continue positioning my life into what I’d prefer. My goal is to stop working for others in the next five years and only work for my own business.

Hi Sam,

Hope everything is going well for you. I have been reading your blog for the last three years and will like to meet you this summer and pick your brains before enrolling to an MBA

Currently, I am applying to few MBA programs ato enroll for the fall of 2018. Specifically, I am applying to Columbia, Cornell, NYU, Ohio State & Penn State. My focus will be in finance.

Two years ago, I graduated from Penn State with a bachelor degree in accounting. Throughout my time at Penn State, I have been involved in many leadership roles. I was an orientation leader for two years, a peer mentor for an English class and the student government Financial Manager. Currently, I am the President for the Chi Alpha Epsilon National Honor society and a member of the accounting association club on campus. Finally, I was involved with the learning center at Penn State to tutor students in accounting.

I love learning about finance and enjoy meeting people like minded as yourself. This summer I will head to San franscisco, California, and it will be a dream come true to meet you over lunch or coffee, while I am there.

Please feel free to reach me via email to set up something this summer.

Best,

Yaya

Your best post in month! Well done!

Time definitely does go by faster as you age. In 2007 I got married and time has flown since then. So much has happened good and bad. My goal for the next 10 years is to drive as many things to goodness as possible :-)

Great post Sam. I love the lessons embedded within it. For being so young, you’re a wise ‘ol Man!

I worry a great deal that what we have directly in front of us is similar to the dot.com boom & bust. Recently, I’ve had several financial consultants ridicule me for having so much held in cash & ultra-short term bond funds (40% cash allocation) and having so little equity exposure (20% allocated to equities) for such a young age (51 years old).

At the end of the day, I sleep better, I have peace of mind knowing that I may be giving up the last 5% of upside in order to save myself the 25% downside risk. When the next Bear Market hits (right around the corner is very plausible), I’ll be laughing my way to the bank while others will be crying in their soup.

Kirk

Hi Kirk,

I have similar thoughts and worries about what lies ahead, but that’s perfectly normal in a bull market like this. This is one of the most hated and feared bull markets ever and big names like Howard Marks and Einhorn are turning bearish. I’m not sure I agree with the comparison to the dot com boom, where you had IPOs every day for companies that were valued based on eyeball views, and having .com in the company name, not profits or even sales. You had taxi drivers and hairdressers handing out stock tips and family members bragging about trading profits. That boom was absolutely euphoric and hysterical compared to this one.

Right now individual investor stock ownership is at generational lows – understandable given the two busts in the past 20 years. Aside from possible mania in cryptocurrency, not seeing the usual warnings signs are flashing red. The yield curve is not inverted (although it is flattening). Junk bond spreads are very tight to investment grade bonds. Low stock ownership as mentioned. Manufacturing, services, employment, and retail sales are all growing and we’re starting to see wage inflation. Valuations look high on the surface, but corporate earnings are growing at 10+% year over year and this is accelerating, adding upside pressure to stock prices (especially overseas which are cheaper and unloved to begin with). FANG stocks are valued rich, but plenty of other stocks are unloved and could be bargains. What specifically causes you to think there’s only 5% upside left?

The opportunity cost you are facing is that by sitting on the sidelines, if we get another 30-50% gain, even if we then get a “typical” bear market of 30%, you won’t see equities cheaper than they are right now. And how will you know when to time your entry anyway? You’ll have to time it perfectly to laugh your way to the bank.

Anyway, just challenging you a bit here. I feel the urge to raise cash as well but not 40% haha. If allocating more to equities would cause you to stress out and lose sleep, then that is reason enough not to. But I urge you to reflect on what exactly would cause you to lose sleep.

Best of Luck!

In 07, I just became a Sales Executive for a very large financial services company. It was a newly created position full of challenges. It was rewarding and I had several good years. In the end, I wound up with 2 lunatic bosses. I left in April of 16 relatively secure at age 50. Stomach problems gradually (very gradually) getting better.

As for the markets, I took my daughters 529, education savings account and extra money set aside for college and went to straight cash. That was over a year ago and I don’t regret it for a second. My younger daughter still have some allocation to stocks but in the 529, the glide path is decreasing that %. I am not far away from making her very conservative either.

As for my own accounts, we are somewhat protective but still invested. I have enough cash set aside to ride through hard times. My wife’s funds about 75% of our spending needs and the passive income covers most of the rest. On net, we are still savers since she maxes her SEP.

I would guide people towards being a bit more protective but not out of the market. If you are young starting out, the 401(k) is a great option. $ cost averaging with a match. Hard to beat that. After taking advantage of the match, open a Roth IRA. So many benefits down the line. Always take advantage of the 401(K)’s match first. Don’t worry about the markets. If you have a lump sum of, say, $20,000, perhaps $ cost average in an equal amount over 5 or 6 quarters. That decreases your risk should a market correction occur.

In 2007 I was in my junior year of college for mechanical engineering. All of the engineers in the classes ahead of me where getting multiple offers with big signing bonuses. I was an above average student so I felt that I was going to have it made when I graduated.

Oh how wrong I was. Once I started to my last semester, January 2009, I started looking for jobs. I could not find anything close to what I was hoping for. Almost no one was hiring people with zero experience. If they were it was low wages and not for an engineering role.

With no acceptable jobs to be had I took the GRE and went to grad school. Turned out to be a blessing.

Hopefully this next down turn will work out as well.

* Learn when to cash in your chips by setting goals. You made these goals because you decided how much was enough. If you’ve somehow found yourself way beyond your goals, then absolutely focus on using your profits for a better life. The saddest thing is losing a massive lead or having to start over.

This one is the most difficult one for me. I don’t like having money on the sideline so it’s tough. The goal keeps moving and more money is always better… I’m going more conservative now than in 2007, but we still have a lot of money in the stock market and real estate. It’s unnerving. I’ll try to be more conservative next year.

I used to be on the 100% index fund bandwagon common in the fire community until earlier this year when I took some money off the table. Of course the market has kept going up, but I have felt pretty comfortable with it.

Maybe getting older and taking a mortgage/having a child has something to do with it, but the wisdom from a certain older samurai may have also been involved.