When it comes to maximizing tax-free income and withdrawals in retirement, understanding what retirement portfolio withdrawals is considered income or capital gains is important. By understanding there difference, you can better manage and possibly reduce your tax liability in retirement.

When you take required minimum distributions (RMDs) from your 401(k), the distributions are taxed as ordinary income, not as long-term capital gains, regardless of how the account grew or what investments were in it. Here’s why:

401(k) Withdrawals Is Ordinary Income Tax Treatment

Both the contributions you made (if they were pre-tax) and the investment earnings in the account are tax-deferred. When you withdraw funds from a 401(k), including RMDs, the entire amount is taxed as ordinary income.

The tax rate depends on your marginal income tax bracket for the year.

If you still don't understand why 401(k) withdrawals are taxed an ordinary income, think about withdrawals as deferred income. You never paid taxes on it in the first place, so IRS wants its money in the back end.

No Capital Gains Treatment For 401(k) Withdrawals

Even if the funds in your 401(k) grew through investments in stocks, bonds, or mutual funds, the growth is not eligible for long-term capital gains tax rates. All distributions from a traditional 401(k) are taxed as ordinary income, regardless of the underlying assets.

Roth 401(k) Exception

If you have a Roth 401(k) and meet the conditions for qualified distributions (e.g., the account has been held for at least 5 years and you’re over 59½), the RMDs would be tax-free, as long as you roll them over to a Roth IRA before being forced to take RMDs starting at age 73.

State Taxes Must Be Paid On 401(k) Withdrawals

RMDs are also generally subject to state income taxes, depending on the rules of your state of residence. Some states exempt retirement income or provide partial exclusions.

Planning Tips for RMDs With A 401(k)

Strategic Withdrawals: Consider withdrawing funds strategically before RMDs start to spread out taxable income over several years.

Charitable Contributions: Use a qualified charitable distribution (QCD) to donate up to $100,000 directly to a charity from your 401(k) or IRA, which can satisfy part or all of your RMD and exclude the amount from taxable income.

Tax Bracket Management: Monitor your RMDs to avoid unintentionally pushing yourself into a higher tax bracket.

Convert Money To A Roth IRA: To diversify your tax liability in retirement, you can do Roth IRA conversions during low tax bracket years. You can also do a Mega Backdoor Roth IRA, by contributing after-tax money after you max out the 401(k) for the year with pre-tax dollars.

What age does required minimum distributions start for 401(k) holders?

Required Minimum Distributions (RMDs) for 401(k) holders generally begin at age 73 if you turn 72 after January 1, 2023, thanks to the SECURE Act 2.0. If you turned 72 before 2023, your RMDs would have started at age 72.

However, there’s an exception: if you’re still working and don’t own more than 5% of the company, you may be able to delay RMDs from your current employer’s 401(k) until you retire. This rule does not apply to 401(k) accounts from previous employers.

Roth 401(k)s are now exempt from RMDs starting in 2024 under the SECURE Act 2.0, aligning them with Roth IRAs.

How is IRA withdrawals considered? Ordinary income or long-term capital gains?

Withdrawals from a traditional IRA are generally also taxed as ordinary income, regardless of how the investments within the account performed. This applies to both your contributions (if they were tax-deductible) and the account’s growth.

For a Roth IRA, qualified withdrawals (those made after age 59½ and meeting the 5-year rule) are completely tax-free—no ordinary income tax, no capital gains tax.

Why aren’t IRA withdrawals taxed as capital gains?

The tax-deferred nature of traditional IRAs means you’re taxed on the full amount withdrawn as income, not based on how long the investments were held or their gains. The tax advantage comes upfront when you deduct contributions or enjoy tax-deferred growth.

How are withdrawals and sales from a taxable brokerage account consider considered? Ordinary income or long-term capital gains?

Withdrawals and sales from a taxable brokerage account are taxed based on the type of income or gains generated by the investments. Here’s how it breaks down:

1. Taxes On Capital Gains

• When You Sell Investments: The profit (or loss) from the sale of stocks, bonds, mutual funds, ETFs, or other securities is taxed as a capital gain:

• Short-Term Capital Gains: If you held the investment for 1 year or less, the gain is taxed as ordinary income, at your marginal tax rate.

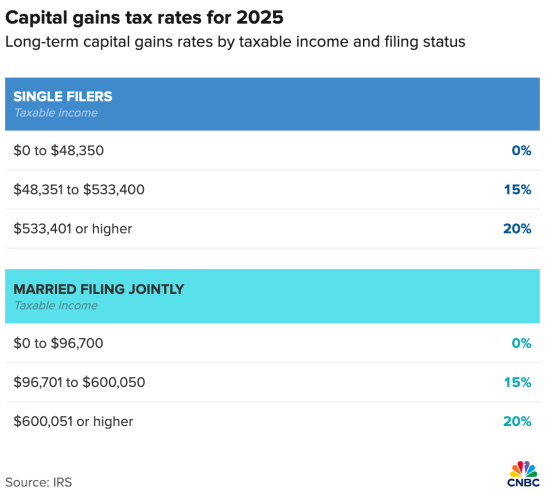

• Long-Term Capital Gains: If you held the investment for more than 1 year, the gain qualifies for preferential tax rates of 0%, 15%, or 20%, depending on your taxable income.

• Losses can offset gains, and up to $3,000 of net losses can reduce ordinary income annually.

2. Taxes On Dividends

• Qualified Dividends: Taxed at the lower long-term capital gains rates (0%, 15%, or 20%), if the holding period and other criteria are met.

• Ordinary Dividends: Taxed as ordinary income, at your regular tax rate.

3. Taxes On Interest Income

• Bonds, Savings Accounts, or Money Market Funds: Interest earned is taxed as ordinary income, unless it’s from tax-advantaged securities like municipal bonds (which may be tax-exempt).

4. Other Considerations

• Reinvested Dividends or Gains: If you reinvest dividends or capital gains, they still count as taxable income for the year.

• Cost Basis: Your tax liability on sales depends on your cost basis (the original purchase price plus adjustments). This is subtracted from the sale price to calculate gains or losses.

• Wash Sale Rule: If you sell an investment at a loss and repurchase it within 30 days, the IRS disallows the loss for tax purposes.

Tax Treatment Summary Of Sales And Withdrawals From Taxable Brokerage

Example Of Tax Treatment From Selling In A Taxable Brokerage Account

• You bought stock for $10,000 and sold it a year and a day later for $15,000:

• Long-Term Capital Gain: $5,000 taxed at 15% (assuming you’re in the applicable income bracket).

• You sold another stock within 6 months for a $2,000 profit:

• Short-Term Capital Gain: $2,000 taxed at your marginal ordinary income tax rate (e.g., 24%).

So long as the gains are under the 0% income tax threshold of $48,350 for singles and $96,700 for married filers, then there will be 0% capital gains taxes to pay.

Example Of Taxes Owed If Total Income Above The 0% Tax Income Threshold

If your total income (including both your W-2 wages and capital gains) exceeds the threshold for the 0% tax rate on long-term capital gains, then the portion of your capital gains that pushes your total income above the threshold will be taxed at the applicable capital gains rate (typically 15% or 20% depending on your overall income).

Let's calculate your tax liability for 2025 with the updated long-term capital gains tax rates you provided:

Step 1: Taxable Income Calculation

We will assume you're a married couple filing jointly, and we'll subtract the standard deduction of $30,000 from your total income to calculate your taxable income:

- W-2 Income: $110,000

- Long-Term Capital Gains: $50,000

- Standard Deduction: $30,000

So, your taxable income = $110,000 + $50,000 – $30,000 = $130,000

Step 2: Ordinary Income Tax Bracket Calculation

Your ordinary income ($110,000) will be taxed at the applicable ordinary income tax rates. The 2025 tax brackets for married couples filing jointly are:

- 10%: Up to $22,000

- 12%: $22,001 to $89,450

- 22%: $89,451 to $190,750

- First $22,000 taxed at 10% = $2,200

- Next $67,450 ($89,450 – $22,000) taxed at 12% = $8,094

- Remaining $20,550 ($110,000 – $89,450) taxed at 22% = $4,521

So, the total tax on your ordinary income is: $2,200 + $8,094 + $4,521 = $14,815

Step 3: Long-Term Capital Gains Tax Bracket Calculation

Now, let's calculate the tax on your long-term capital gains ($50,000). Based on the updated tax rates:

- 0% tax rate: Up to $96,700 of taxable income

- 15% tax rate: $96,701 to $600,050

- 20% tax rate: Over $600,051

Since your total taxable income is $130,000, the first $96,700 of your taxable income (after the standard deduction) is covered by the 0% capital gains tax rate. Since your taxable income is $130,000, and you already have $110,000 in ordinary income, $20,000 of your capital gains fall into the 15% tax bracket.

- $20,000 of your capital gains taxed at 0% = $0

- $30,000 of your capital gains taxed at 15% = $4,500

So, the total tax on your long-term capital gains is: $4,500

Step 4: Total Tax Liability

Now, we can calculate your total tax liability by adding your tax on ordinary income and tax on long-term capital gains:

- Tax on ordinary income: $14,815

- Tax on long-term capital gains: $4,500

Total tax liability = $14,815 + $4,500 = $19,315

If you earn $110,000 in ordinary income and $50,000 in long-term capital gains as a married couple in 2025, your estimated total tax liability would be $19,315.

Consult With An Accountant For Retirement Tax Optimization

As you can see from the examples above, retirement taxes can be complicated, and it's easy to make mistakes or misunderstand tax liabilities from different types of retirement portfolios. That's why it's always best to consult with a CPA or financial professional for personalized advice.

While I'm not a tax professional, I am a tax enthusiast who has done my own taxes and studied the tax code since 1999. However, for any specific tax questions, always consult a tax professional.

Check Out The Best Financial Planner: Boldin

Withdrawing retirement funds in a tax-efficient way can be daunting, but the Boldin Financial Planner makes it much easier. Built specifically for retirement planning, Boldin offers the best tools to help you navigate this critical stage.

One standout feature is their Roth Conversion tool, which helps you determine how much to convert to potentially save the most on taxes. A snapshot of the tool is below.

If you’re serious about building wealth and retiring comfortably, sign up for Boldin’s powerful financial tools. They offer a free version and a PlannerPlus version for just $120/year—far more affordable than hiring a financial advisor.

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Your shares, ratings, and reviews are appreciated.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009. Everything is written based on firsthand experience and expertise because money is too important to be left up to the inexperienced.