Making six figures a year is a lot of money. However, depending on where you live, making six figures may still not make you feel rich! Due to higher cost of living and inflation, making six figures is no longer a guarantee for high living.

One of the great things about America is freedom. Tired of feeling like death living in Chicago, New York City, or Boston during the winter? Why hello San Diego, Miami, or Honolulu!

Not feeling there are enough job opportunities for advancement in Detroit? Then come on down to San Francisco! Thanks to the growth in technology and artificial intelligence, well-paying job opportunities and investment opportunities are abundant.

Tired of eating healthy food in San Francisco that costs an arm and a leg despite having a six figure salary? No city can beat the wonderful soul food of New Orleans.

Geoarbitrage is a term where one can earn and save money in one place and move to a cheaper location to maximize their money. If you happen to own an internet business, then your ability to geo-arbitrage is greatest.

I've often thought about just relocating to Thailand for several months at a time given friends say they live extremely well off $2,000 a month for two. Given one of my goals is to take 100 hours of intensive Mandarin lessons, I may very well be writing to you from some lower cost country in the future.

In Search For More Riches Online

70% of the audience comes to Financial Samurai through a search engine like Google. They have a financial problem they are trying to solve. This is huge because it takes initiative to come to grips with one's finances.

But what I've noticed over time is that besides the middle class getting pissed off about the widening wealth gap, upper-income earners making six figures or more are also feeling some angst as well. During a bull market, the rich get richer given the rich make and have the most.

Over 50% of singles readers and 74% of household readers make over $100,000 a year based on my Financial Samurai income poll (14,000+ so far down below). As a result, I'd like to delve into analyzing how a “typical” $200,000 a year household spends their six figure income.

A six figure salary can range from $100,000 to $999,999. So I figure I'd start on the low end for two people. $200,000 is a comfortable household income, but I don't think it can qualify as rich. With inflation running at 40-year highs, households need to earn more to run in place.

Making $200,000 A Year And Still Feeling Average

Below is a chart that shows how making six figures a year is pretty average in a city with a child. Expenses really add up. And these include investment expenses as well.

This lovely family of three living in San Francisco, with two working parents making $100,000 each (hooray for income equality!) are left with roughly $5,700 a year in disposable income after expenses and 401k contribution. Given their total cost is $121,700 after tax a year, that's roughly $10,000 a month they're spending.

Here in San Francisco, if you make $117,000 for a family of three, you can apply for low-income housing. When looking at six figure incomes, it's important to always compare living costs.

I can hear the detractors now. So let me preempt your complaints by addressing them up front. Just know there are families making $500,00 a year and scraping by! Let's review some of this family's expenses.

Mortgage: $36,000

This six figure income family took out a $640,000 mortgage at 3.75% after putting down $160,000 for a two bedroom, two bathroom single family home in the outer regions of San Francisco. Their payment is $3,000 a month, or $36,000 a year. 70% of their $36,000 mortgage is interest. Take 70% X $36,000 = $25,200 a year in interest they are paying which is deductible from their $200,000 gross salary.

The family now has $18,000 (401k) + $25,200 (interest) in deductions. To make math easier, let's just take the $25,200 in interest and multiply it by their federal marginal tax rate of 30% (they straddle the 28% and 33% federal income tax bracket) to get $7,560. In other words, when they file their taxes they should get roughly $7,560 back on top of the $5,700 left over they are saving.

This family now has roughly $13,260 in disposable income after maxing out their 401k after they file their taxes. For every year they work, they can save a little over one month in living expenses before they feel great strain. Their effective tax rate is probably closer to 27% than the stated 30% in the chart.

Childcare: $24,000

Yikes! Childcare is expensive. The average cost of center-based daycare in the United States is $11,666 per year ($972 a month), but prices range from $3,582 to $18,773 a year ($300 to $1,564 monthly), according to the National Association of Child Care Resource & Referral Agencies (NACCRRA).

OK, so my $24,000 childcare estimate is high. But it is high because I also asked five friends in San Francisco who have kids in childcare and that's what they say they pay. Remember, averages don't properly estimate the true costs in many departments. Besides, I haven't even included the cost of private school tuition as an option!

If you get a night doula for a newborn, expect to pay $5,000 – $10,000 a month! It's costly, but the mother will love it. Alternatively, you may go the less expensive route and get an au pair.

With an au pair, you provide the person housing and food versus a nanny who just comes to your house during the day.

Two Vacations A Year: $8,000

Damn, Gina! What kind of vacations cost $4,000 each for a family of three? How about a good old fashion staycation, or camping in the woods for $200 bucks instead?

I'm a big proponent of staycations and road trips, especially now that gas is so cheap, but this is a hard working couple who only have four weeks of vacation a year. Their time is so valuable that they want to live it up and yolo when they can.

Let's see, three roundtrip tickets to Maui from San Francisco costs around $750 each during peak season (goes up to $1,200 actually). That's $2,250 on airplane tickets right there. Lodging costs $300 a night after tax for something very average. That's $2,100 for a week's hotel stay for a total of $4,350.

Meanwhile, the family hasn't even eaten or paid for any type of fun activities yet! The total cost of a two week vacation to Hawaii can easily go over $6,000.

A More Frugal Vacation

Let's say the family decides to be a little frugal for their remaining two weeks of vacation by renting out the one bedroom portion of my two bedroom condo in Lake Tahoe this summer. The price is an internet low $195 a night (vs. $250+) + the $25 Resort fee, cleaning fee, and taxes.

The total price comes out to $1,708 for check in July 9, check out 7/16 for seven nights. Now let's add on $50 for gas round trip. Add on $600 for food and fun and we're talking only $2,358 for a week in one of the most beautiful places to go during the summer.

Car Payments: $6,000

What a waste! But a $500 a month car payment (after tax and fees) is so common for many Americans nowadays given the median price of a new car is $32,000. I was considering leasing a $41,000 Jeep Grand Cherokee Limited for ~$500 a month, but decided to go for my dream car, a $19,025 pre-tax 2015 Honda Fit instead.

A $500 a month car payment (based off a $5,000 downpayment, another big waste of money) allows one to drive a BMW 3 series, Mercedes C-class, Lexus IS250, Audi A4, and a Jeep Grand Cherokee.

These cars are definitely a notch more luxurious than your Honda Accords and Toyota Camrys ($21,000 – $26,000) and so forth. But a $40,000 – $50,000 BMW 3 series is pretty common for a family making $200,000 a year, even though

I recommend a family should spend no more than $20,000 for a car. Just read the 500+ comments in my post on the 1/10th Rule For Car Buying Everyone Must Follow and see for yourself.

$4,800 a year on gas seems high now that gas prices have plummeted. So let's say the $4,800 includes all transportation costs, including bus fare, taxi rides, Ubers, and gas.

Related reading: How To Make Over $100 An Hour Driving For Uber

Student Loans: $0

A lot of readers who make a $200,000 six figure income level have pointed out in the comments that this couple is lucky because they don't have any student loans. They are right! They paid for their education along with the help from their parents.

Taxes: 30% effective

A 30% effective tax rate may be several percentage points higher than reality. The six figure income married couple is at a 24% marginal federal tax rate as of 2018. If they were to only pay federal taxes, the effective tax rate is closer to ~22%. But they live in California, where they face a state income tax rate of 9.3%!

But, oh yeah, they also have to pay FICA tax on wages up to $147,000 for 2022. That's another 6.2% for Social Security + 1.45% for Medicare = 7.65%. It's easy to see how the total effective tax rate is about 30%.

Thank goodness they have $25,200 a year in mortgage interest they can use to lower their taxable income by that same amount.

Property Taxes: $8,000

The $200,000 six figure income family lives in San Francisco and pay a property tax rate of 1.24% on the assessed value of their property. They bought property for $650,000 a year ago, and the city has assessed the property at $667,000.

Due to Proposition 13, property values can only be assessed by an index that rises no greater than 2% a year, even if the property might increase in value by 20%. If they were to sell their property now, they could probably get $700,000 or more since San Francisco prices have continued to go up.

If you want to invest in real estate more surgically, I recommend checking out Fundrise, the best real estate crowdfunding platform today. They are a great way to diversify your real estate holdings, especially into the heartland of America where valuations are much cheaper and net rental yields are much higher.

I've personally invested $954,000 in real estate crowdfunding to simplify life and earn a higher income in early retirement. It's great to earn income 100% passively! Fundrise is a long-time sponsor of Financial Samurai and Financial Samurai is a six-figure investor in Fundrise funds.

Healthcare Expenses: $$$

Employers generally subsidize your healthcare premiums through a group health insurance plan. The cost can range from $0/month – $800/month for a family. It all depends on how generous your employer's benefits are.

College Savings: Whatever is left over

Another missing item from the spreadsheet is college savings. Like most families with young kids, they aren't putting aside a specific amount of money yet because they've still got 10-15 years to go.

They've decided to just focus on saving for their retirement first in their 401k and after-tax brokerage account. Parents should also consider contributing to their child's 529 College Savings plan as soon as they are born.

Note: contribution limits for 529 plans vary by state and can change each year. Some follow the Federal gift tax exclusion amounts, but best to check with your plan's sponsor for details.

When the time comes for their kids to go to hopefully public school, they'll draw from their savings and brokerage accounts to pay as they go. Parents should also consider using a 529 plan for generational wealth transfer purposes.

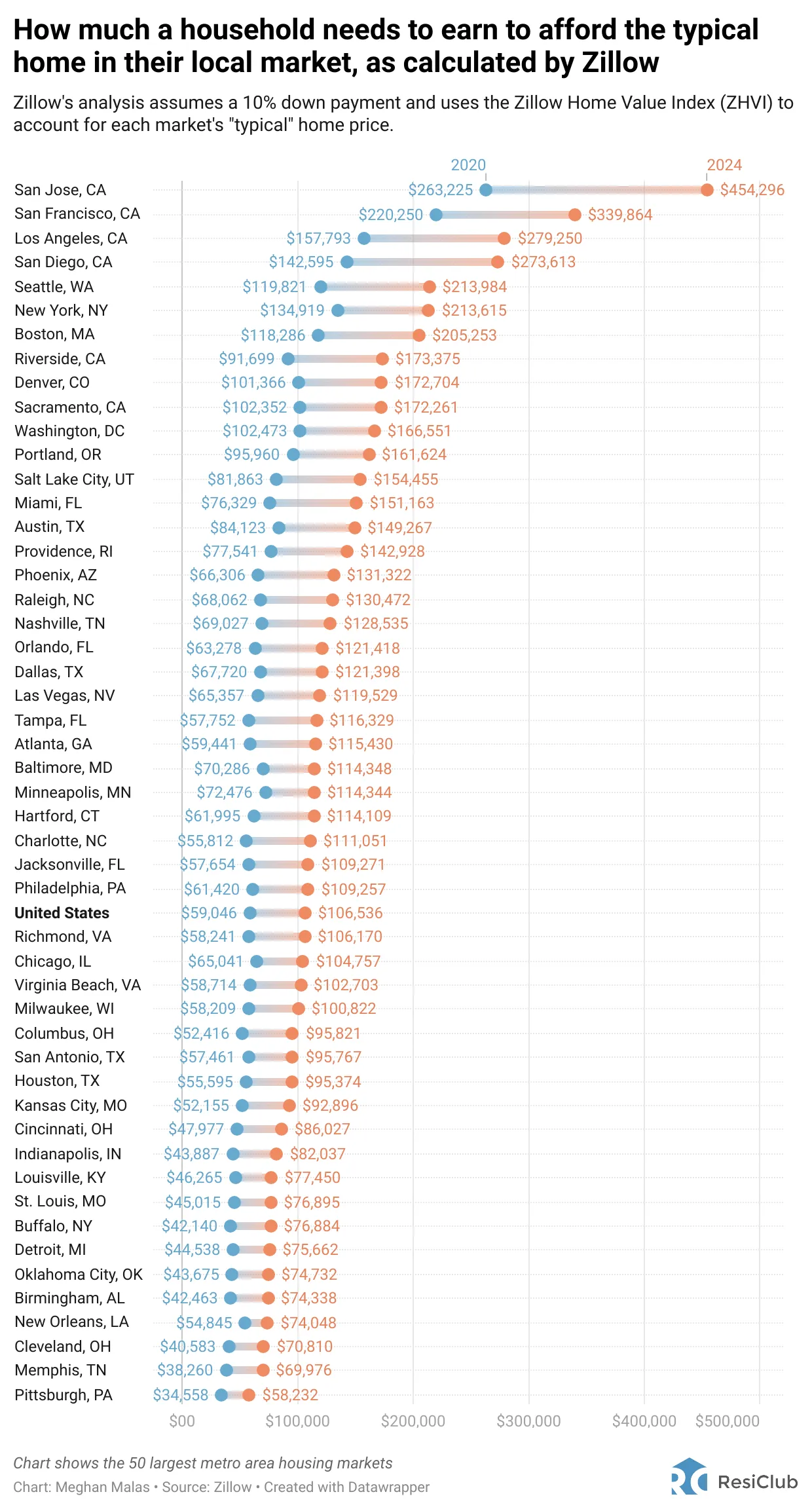

You Can Make Six Figures And Not Feel Rich In These Cities

For 2024, Zillow came out with an insightful study on income required to afford a typical home in the largest 50 cities. For the entire United States, $106,536 is required to buy the median priced home in America, which is currently around $420,000.

Based on the analysis, if you live in San Jose, San Francisco, LA, San Diego, Seattle, New York, Boston, Riverside, Denver, Sacramento, Washington, DC, Portland, Salt Lake City, Miami all the way down to Milwaukee, you will NOT feel rich making six figures in these cities.

The reason is because earning six figures is REQUIRED to simply own a typical home in the city. And feeling rich means feeling like you've got more than others.

Don't Let Money Rule Your Life

I read some study that in order for you to feel rich, you have to make 3X as much as you currently make, no matter what you make. So if you're making $50,000 a year, $150,000 a year in income will make you feel like making it rain at the clubs.

But if you're making $150,000 a year in income, you won't feel rich until you make $450,000 a year. In other words, human beings don't ever seem to be satisfied with what they have.

What we like to do is project our emotions onto other people. So for all those people making less than $52,000 a year, it's easy to say any household making $200,000 a year should feel rich and should shut the hell up about paying a progressive tax rate.

Making as much money through non-wage income (W2) is what it's all about.

The family in my example is going to live a nice and comfortable life, no doubt. After 20 years of work, they'll likely have saved over $500,000 in their 401k, and perhaps another $100,000 in after tax investments and savings, even if their $200,000 income stays static.

Nobody is going to cry for them. I just don't think this six figure income family will ever feel rich, just comfortable since they have to keep on working and paying an ever increasing tax rate.

Diversify Your Investments Into Real Estate

One of my favorite ways to get rich is through real estate. The combination of rising rents and rising capital values is a very powerful wealth-builder. Mainly thanks to rental income, I was able to leave my day job in 2012 at age 34.

In 2016, I started diversifying into heartland real estate to take advantage of lower valuations and higher cap rates. I did so by investing $954,000 with real estate crowdfunding platforms.

Take a look at the two best private real estate platforms

Fundrise: A way for all investors to diversify into real estate through private funds with just $10. Fundrise has been around since 2012 and manages about $3 billion for 350,000+ investors.

The real estate platform invests primarily in residential and industrial properties in the Sunbelt, where valuations are cheaper and yields are higher. The spreading out of America is a long-term demographic trend. For most people, investing in a diversified fund is the way to go.

Fundrise is a long-time sponsor of Financial Samurai and Financial Samurai is an investor in Fundrise funds.

Manage Your Finances In One Place

Get a handle on your finances by signing up with Empower. It is a free online platform which aggregates all your financial accounts in one place so you can better optimize your money. Even at a high income, money escapes like water from a leaky bucket if you don't carefully track where it all goes.

Before Empower, I had to log into eight different systems to track 30+ difference accounts. Now, I can just log in to see how all my accounts are doing, including my net worth. I can also see how much I’m spending and saving every month through their cash flow tool.

The best feature is their Portfolio Fee Analyzer, which runs your investment portfolio(s) through its software in a click of a button to see what you are paying. I found out I was paying $1,700 a year in portfolio fees I had no idea I was hemorrhaging!

There is no better free financial tool online that will help you build your wealth for financial freedom.

Our household income falls into the $200,000 mark. It hasn’t always been that high, in fact much lower until the past couple of years. We have been in the same house for the last 13 years and never went out and “traded up” as our income grew. We have one car payment of $200. We are paying off our mortgage next month. Our house is now worth over $600k thanks to Austin’s booming market. I max out my 401k to include the extra $5k a year. On top of that we save $4-5k a month and can still take a yearly trip to Europe and live quite nicely. Our net worth is now over $2M. (I just turned 52). The point is not to brag but to show that by living responsibly and below one’s means, one can accumulate wealth quite easily. If one has to maintain a certain image and drive new cars it will be a tough slog.

My dad worked 2 jobs to raise a family of 5 on $32,000/yr near the DC area. No BS, his one job paid $26k and the part time paid $6k. We all turned out fine, no there was no college savings for us, no private school for us. My brother and I got scholarships and went to college for not a nickel nor dime.

And I make $155k/yr now. Living in the same area. I feel just as rich, as we did growing up with my min wage job. Moral of the story is, as long as you have your loved ones, with food on your table and roof over your head, you are rich.

This is awesome to hear! And also must mean that raising children isn’t as expensive as people make it out to be.

These are called HENRYs (high earners not rich yet). The fact there is an acronym for this demographic just yells how much of an epidemic this is. Unfortunately, this demographic is driven by three things, location location location. In New York the average rent is $50,000 which is close to the average American salary. And in San Francisco, if you make less than $100,000, you are classified as lower class. Unfortunately, these areas make it almost impossible to improve your finances. I think we should remind people that you can live off $40,000 better in most places within the US than $100,000 in many of our cities.

Live in LA now, from South Bend Indiana originally. I bought a super nice three bedroom house with a two car garage in a great neighborhood there when I was making 38k a year. I make 150k now and the thought of buying a house out here is comedic. I’m still paycheck to paycheck, in the midwest I’d be living like a god on this salary.

I’m happier here with the sun and beaches and creative types everywhere and will never gove a dime to a red state again if I can help it, but I’m definitely paying for the luxury.

ok

I really have to laugh at all these comments here. Most of you should come to Western Europe and experience what it’s like to have super stagnant wages in pretty much every field imaginable and get taxed for roughly 50% of what you make with fast-rising living costs. Nobody from the states or Canada I ever met was able to really make it work here and everyone is always complaining about the states. LOL. Seriously, get some perspective and get outside of the states every now and then, it might help. You all got it good over there and if you f up it’s due to your own choices.

My wife is from Western Europe- the child care is $500, college is $0, health care guaranteed and minimal. You might not have jobs – but you have a far less hard nosed, be poor and die environment. The states is hard core – we’ve had countless friends move back to France, Germany, Spain, and Italy if those coming in didn’t have PhD, or high tech degrees.

Maybe see the gaps in between that aren’t in focus. Arguing about this is ridiculous.

You need a job though. Not much you can do on state aid.

Im new to this site, but interesting article. You dont address a topic that affects many–divorce. Im 50yo and make $225k/year in Wash, DC. I divorced 5 years ago, but due to antiquated divorce laws on the east coast pay I pay $45k a year in perpetuity to my ex-spouse. The legal bills totaled $200k and depleted most savings outside of our retirement plans. I have 2 kids in college that im doing my best to keep from student debt. I purchased a townhome that is too small for the kids when their home, but at least I do not have a mortgage. Without going through the rest of the details I live paycheck-to-paycheck with living expenses. Although I will build enough savings that I could afford retirement, the fact that I will continue to bear the alimony obligation until death will prevent it.

thank you for this perspective. I’m 28 and will do everything in my power to protect myself financially when I get married. On first dates, I say, Im a huge prenup guy.

That was your takeaway lol. Try taking your time to pick a spouse, making sure you share the same values, know marriage is hard belt getting into it and forgetting about getting divorced for “irreconcilable differences” and to end on a financial note also remember, “it’s cheaper to keep her”

Also….you rent paying 30% of the entire 182K income. they should only be paying 30% of that tax bracket.

$0–$9,700 10% of taxable income

$9,701–$39,475 $970 + 12% of TI over $9,700

$39,476–$84,200 $4,543 + 22% of TI over $39,475

$84,201–$160,725 $14,382.50 + 24% of TI over $84,200

$160,726–$204,100 $32,748.50 + 32% of TI over $160,725

so the numbers arent super accurate.

This article would be more accurately titled “how to be so spoiled and entitled that you think driving $150,000 cars and taking multiple vacations a year makes you ‘average.'” You make good money, can afford a home in an expensive market, and don’t even have student loans to worry about because you were born with a silver spoon in your mouths, and you still want to bitch about money? Give your damn heads a shake. I make less than these people, get by on a single income, and actually paid for my own higher education. Not once have I ever thought that I’m “average” just because I can’t afford a side of caviar with my steak.

Most people who make low six figures are working at jobs that don’t enable them to take even one, let alone two, $4,000 vacations a year. I work 60 hour weeks, on average. I’m lucky if I can get away for a weekend trip (~$500-700) and haven’t had time for a real vacation in nearly 4 years. I also drive a used Honda because I’m not dumb enough to incur unnecessary debt when I can afford to buy a perfectly adequate, reliable car with cash. How much do you have to spend on a car to be paying $6,000 a month in car payments?? You’re driving TWO Ferraris?? And if you’re really THAT bad at financial planning, what the hell are you doing having a child?? Grow up and learn to adult before you try to raise another human being, FFS.

I wonder if it would help if I added the word “annual” to the spending budget. I didn’t realize people would see my chart and think the $200,000 number was per month.

As a teacher, Even if all my students understand except for one, I am failing. So your feedback is helpful to help me make my writing and my charts clearer.

I understood the article perfectly unless it has been edited. The 6k was Annually not monthly. 6k a month car payment should not even seem likely to anyone unless it was the abovementioned “Ferrari” even then….buy cash no financing .

It’s up to you whether you want to believe me, the writer of the article or not. $200,000 is an annual baseline assumption as are all other expenses.

I was worried about reading this but also kind of relieved. I am currently a student at an In-state University studying Aerospace Engineering and due to a few mess ups my undergraduate degree is actually taking 6years to complete overall and not the expected 4 years which is adding at least $50k in debt overall once I graduate. I am extremely worried that I will be paying for these loans for the rest of my life. I’ve already sold my brand new car and paid off what I owed to stay out of the debt hole. Any advice as to how I should go about deleting all of my loans as quickly as possible once I graduate?

Honestly it depends on what your rates are. If you have rates that are lower than what you can earn by investing, etc., then sinking as much cash as possible as quickly as possible into paying off loans doesn’t make sense. One big mistake I see people make is dumping all their cash at once into paying off loans or buying vehicles without considering the time value of money. Spreading yourself thin to pay off those loans and leaving yourself no out should an emergency come up isn’t doing you any good when it comes to financial security.

Secondly, you’re going into Aerospace Engineering, which means a close to 6-figure starting salary at worst. You’ll be in no danger of defaulting on your loans, so stressing yourself the way you are just isn’t necessary. It’s already lead you to taking whatever massive depreciation hit you experienced by selling that new car and paying off the principal and interest right away, with the difference in what you got and what you owed on it coming out of pocket. Maybe you negotiated some miracle sale price, and if so congrats, but otherwise you panicked yourself into an unnecessary loss.

I don’t know your exact situation, but what I can tell you is that unless a decision will make or break you staying in your home/apartment, being able to eat the next day, etc., you shouldn’t be rushing financial decisions. You’re still in school, which means that odds are you can find professors and resource personnel on campus who can advise on these things and give you the whole picture to look at. If you had an engineering issue that meant there was a potential failure on the horizon would you rush to a solution or what you evaluate the entirety of the situation, apply the knowledge you have, look elsewhere as needed, and draw conclusions based on a complete as possible understanding of the situation? Your finances should be no different.

You don’t read very well do you…

Agree 200k does not “make you rich” if you define reach as being able to throw money on whatever you want. My wife and I live in LA and we make over 200k a year, we are both late 20’s and do NOT have children.

Do we feel rich? personally I do… it is a matter of perspective. I mean we live so comfortable, we have access to virtually anything we want. Do I feel like going skiing? sure I’ll go buy a pair of skiis and go skiing. feel like mountain biking? sure I’ll go buy a mountain bike. Trying out food from anywhere in the world? sure let’s go to a Thai restaurant!. How is that not being rich? did you know 99% of the world population won’t even ask themselves these questions? You people are whining too much, and think that you deserve the world in the palm of your hands. Well hello, consider yourself fking lucky to spend EIGHT THOUSAND DOLLARS A YEAR!!!!!!! ON VACATION.

So what’s the catch? yes… no kids… but life decisions man… we went to Spain last year for 2 entire weeks and spent 2.5k (including tickets), while eating out every single meal. We splurged big time!. Spain is crazy cheap and you can rent beautiful apartments on AIRBB dirt cheap and way nicer than hotels. We even rented a car and drove around the southern country. Hell people, why are you going to Hawaii!!! it is a rip off my man! go to the Caribbean, go to Dominican republic, mexico, anywhere literally NICER and WAY CHEAPER get out of your white american bubble.

College savings. I mean… if I want my future children to have the life I have, they need to go to top 10 schools. Right? WRONG!!! My wife works for NASA and I work as a lead Data Scientist for a huge corporation. We both went to state college, so we have no student loans. I got my old company to pay for my grad school (at state school) and my wife got a research scholarship that paid for her grad degree too.

Cars. We bought a used Toyota corolla with only 25k miles on it a few years ago. Why? because that car is build to be amazing, safe, and cheap!!! paid up front, no loans boom, it is just practical. Yes we did splurge on my dream car when I got my last job, a brand new jeep wrangler. But I got the most basic version, just what I need, paid more than half up front and took a 3 year loan that I paid really fast in 7 months. At this moment we have 0 car loan payments, a brand new wrangler, and a solid Toyota corolla.

We go out to eat a lot, we go camping a lot, we go on weekend trips and stay in AIRBNBs or small inns etc… We splurge every now and then, but we do it in a smart way. For example I am into mountain biking, and those things can be expensive! but hey, I am by no means a professional rider, so I don’t need a 5k bike! so I bought a 1k bike that does great!.

It is all about life choices and perspective. Be grateful for what you have and stop whining. Yes I understand children add a lot, and we know things will get a little more challenging. But we are rich, most people making this much money in the U.S. are rich. We just think we deserve the world and are privileged af.

Good perspective.

But having kids will certainly make you feel poor if you stay in a expensive city.

https://www.financialsamurai.com/eight-takeaways-on-being-a-stay-at-home-dad-for-two-years/

I think you should tell your reader about the danger of stockbrokers. They always make you broker and the benefits of a financial planner. I also think you should write about the guy who dropped out and had a wonderful life playing and being irresponsible. We all end up in a bone yard so what the ….

Check it out:

Questions To Ask Before Hiring A Financial Advisor

Hire A Financial Advisor Or Lose Money All By Yourself

Much discussion going on about middle class and how much money does a person need to be rich. This is my yardstick.

If a person has a closet he/she is upper middle class. If the person has a closet with extra clothes and shoes he/she is rich. If you don’t believe me, travel outside of America.

It’s all relative. Feeling rich or not has more to do with your perspective than your income. A few years ago I was making $220K/yr and I felt rich! Now I make $450K/yr and I don’t feel rich. 2 kids, a bigger house, more ambitions…they changed my perspective. That’s not to say I’m not grateful or happy, just feel like I need to manage my finances better.

Yeah, kids will do that to you. I didn’t believe it til I had one. They definitely live better than I did as a child.

I did not see any utilities or phone in the budget: Heat, electric, water, cell phone, etc. Was it embedded somewhere?

I live in East Bay across the bridge from san francisco . I’ve been here for 4 years. Prior to that, I lived in Los Angeles.

Overall, Sam’s post is a good stab at the ‘average’ living in the bay area.

It really tries to address cost of living of hte area, but also acknowledges that entitlements that I see prevalent in my community.

However, below is an outline of what I’ve personally done to increase my wealth in the Bay area, which I hope will serve as inspiration for those struggling to live here:

1. home ownership- the average selling price for a home in SF is 1.6 mill as of 8/2018. That’s a whopping ~7000/month mortgage= 96000/year.

Even if one decided to live in a decent low crime suburb, homes are still AT LEAST 700-900k (3300- 4300/month or 40k- 50k/year). And that doesn’t even include home insurance, repairs, ect.

Depending on the area, renting usually might not be any better FOR EQUIVALENT UNITS. And i personally know plenty of people who are paying the above.

But here is where I’ll go on to the idea of personal entitlement. I think there are some people in the audience who make the assumption that they are entitled to live in a nice cozy home/ apartment in a safe neighborhood. And if you fall in that category, it’s totally fine, but really its not- because it’s probably costing you an arm and a leg. There are plenty of living situations in the bay area that can be had for less than 3k a month. I live in one of them with my girlfriend, but we definitely needed to take austerity measures to stay in this situation (one bathroom, two bed in a questionably mixed location). And before anybody starts poking fun about what ‘questionable’ means, i just want to remind everybody that there are plenty of people living my our neighborhood, and to put me down for this living arrangement is to put my entire community down as well; so let’s just keep it positive and say that my neighbors and I make the best of the situation and environment. As we share a room, my girlfriend and I pay 1000 of the 1900/month rent shared with a roommate (12k/year). even though I’m not gaining equity in this situation, my rent is probably about or less than property tax and home insurance (sunk costs anyway), so I feel like this is a good deal.

So going back to my friends paying 3300-7000/month in mortgage/rent in the bay area, and complaining about it: consider searching for a less desirable setup if money is tight. It’s out there.

2. $8000/year vacations-

This figure is accurate for many of my friends, but again, it touches upon the idea of entitlement- “I deserve a good 2 week vacation every year”. I grew up with parents who came to America with $20 and a suitcase full of clothes. A “vacation” meant going somewhere local, staying with relatives or a motel, packing food, etc. you get the idea. Some people in my network are convinced that they are entitled to spend a minimum 3k on a 2 week vacation. Again, for those intending to increase wealth, it’s not a good idea.

Even when I started making over 150k a year and tried a “fancy “ 1 week vacation to Hawaii, I kept my expenses (including airfare) to less than 1300 for TWO people (a combo of good airfare and hotel hunting, and frugal eating habits). Note how I took a ONE week vacation, and not 2. That is also something to consider.

I’m not saying that vacations aren’t important. But to assume that 2 weeks a year is necessary will also cost more money. If you are really interested in finding relief from stress, I find that stress relieving habits/activities THROUGHOUT the year applied to the workplace and home setting are much more effective than any relief a vacation can provide.

3. Food/going out- this is probably going to be my favorite section.

If it’s one thing I learned growing up poor, do not underestimate the power of food.

Some people find it acceptable to spend upwards of $150 on “date nights” every 2 weeks on restaurants. I totally agree that going out is important for any relationship/group, but my girlfriend and I make it a point to spend less than half of that, and actually do fairly well with that (even when we go out with friends).

Anything labeled organic may just be a marketing strategy. No research proves that paying 20% more on organic products will improve your health.

What IS proven, however, is that caloric restriction may actually be good for your health as a productive individual in society https://www.sciencedaily.com/releases/2018/03/180322141008.htm

So 2-3 times a week, I intermittently fast, which I’ve been doing for going onto 2 years now. Skipping meals saves me about 5% on my grocery bill.

In the process of transitioning to a fasting lifestyle (and this occurred naturally to my surprise), i found myself craving more vegetables from being 50/50 meat/everything else to a 20/60/20 meat/vegis/carb diet. So guess what happened? Spending less on meat = spending less on groceries- about a 5% reduction in grocery cost.

One last benefit is that my stomach had shrunk as well, so I end up eating less overall (instead of eating an entire portion at a restaurant, I eat half, and save the other half later). Slap another 5% savings.

Before you make any assumptions, I’ve been checked by my physician and he and I concur that I have not lost any meaningful muscle mass, only fat. In fact, I get a ton of complements now having lost about 20lbs since starting the regimen. Also, I can personally say that I’ve never felt so physically good in my life since implementing intermittent fasting.

If the above seems extreme, it was meant to be examples to challenge the entitlement to food I see so often around me. The point I’m trying to make is that SIMPLE healthy dietary habits can save money, but they may be the most difficult to IMPLEMENT if one subscribes to any type of entitlement to meat/sugar/fat. Trust me, for the average american, there are more than enough calories that can be cut, and, IF CUT CORRECTLY, will lead to saving money and even improve one’s overall health and well being; and who knows, maybe reduce healthcare costs down the line (as obesity is linked to money wasting and quality decreasing chronic diseases such as diabetes, kidney disease, and heart disease; i personally know from my own extended family). Just food for thought (no pun intended)

Anyway, my savings are real and tangible.

4. Car payments- I had a friend that decided that it would be a “wise” investment to buy a tesla model s for a bargain 75k, trying to convince me that the gas and maintenance savings alone would pay for the car. I drive a honda civic that was a little less than 17k out the door brand new, which i will use as part of this example. In my analysis of my friend’s statement, I asked myself, “will an all electric car at that price really save money?” so I did a thorough analysis of gas savings in an electric car, electric costs to run the car, insurance cost of the model S over that of a Civic, maintenance cost of both the model s and the civic, and a risk adjusted estimated loss of a catastrophic failure of an electric engine (specific to electric cars) vs that of a honda civic’s gas engine, and what I found is this: the model S is still more expensive. The increase in insurance premium alone negates any savings in gas costs that the tesla might save over a honda civic; and the risk adjusted failure cost of the model S drivetrain out warranty (as my friend stated that he will drive it for over 5 years, and will eventually have a period of non coverage) was more than the entire risk adjusted engine failure cost and maintenance of owning a civic.

The point is, as Sam implied, any vehicle over 20k is a LUXURY car, and any luxury car, in general, will cost money.

Clothes- I spend at most 500/year on clothing. I frequent thrift shops and repair my shoes. for those that feel entitled to spend up to 5000/year, it’s costing you money.

Charity- charity is great, but to be a realist, if your other expenses are overwhelming you, the biggest act of charity you can do to society is not getting into more unmanaged debt.

I personally donate to good causes, ONLY BECAUSE I AM NOT IN ANY UNMANAGED DEBT.

And consumer debt- I gave you my life habits above, do you really think I have any? Frugality is a lifestyle, and practicing it in one part of life will often times transcends to other parts of your life. So the answer is no, i do not have any because of HABIT.

You got this far onto my post. 1.Iis all the above worth it where I live? and 2. how does this have anything to do with FinancialSamurai’s post?

1. In the past 2 years, I have been able to consistently save and invest on average of 40% of my income a month (150k income last year, and expected income of 200k by the end of this year). In just 2 years, I’ve been able to save 120k (does not include what I made investing it.) AND ALL THIS WHILE LIVING IN THE BAY AREA with an average income of 175k. and

2. Saving money and investing it correctly has everything to do with FinancialSamurai, even if Sam’s figures and opinions in this post may be debatable.

So for those who live in the bay area and feel victimized by the cost of living which you believe is astronomical and unique only to this region of the country, stop being the victim, and challenge that assumption. IT IS, TO A CERTAIN DEGREE, AS EXPENSIVE AS YOU MAKE IT. The sooner you accept personal accountability in your own cost of living, the better off you will be in this area. Evaluate your own entitlements and accept that some austerity is OK.

The reality is, most will reject any notion of what I’m writing, some will accept some aspects of it, and maybe one or two will make drastic life changes that will lead to wealth and prosperity. Good luck, I hope this gives some insight on bay area living.

One last note: To be fair, I don’t have a child. However, after doing the math. Even if I did have a child, I’d still be saving 25-30k more a year than what Sam had estimated if my girlfriend simply had a child, gave it to me, and left me to care for him/her myself. However, that is highly unlikely. If we had a child and she decided to be a stay at home mom, we would save upwards of 40-50k a year more with our current habits. And if she decided to work, she would add an additional 100-120k a year to our income, which would totally negate the cost of child care in my original equation. So yes, those with children still have hope.

I love how all these people are judgmental about how this couple spends their money. We all have different values and how much we spend on childcare or schooling for children is not up for the rest of you to debate. They’re NOT your kids so if these parents choose to drop $24k on childcare or private school then that is them choosing to put that money there instead of investing. They’re not complaining about it, they’re saying “this is what we value” so we pay for it and for those reasons what is left, is minimal.

We live in Minnesota – one of the HIGHEST taxation states. Combined we make just shy of $250k combined with 2 kids. I just registered for my employer health benefits and all that. $21,600 is coming out of my check for all the employer subsidized benefits. Then of course we both max out our 401k. We also contribute about $8k annually to our kids 529 plans.

We have a 2012 mini van that is paid for. we also have a Honda that is only $200/month

We take lunch to work every day and make our kids lunches every day. They go to private school and day care so yes we spend $24k on that annually.

One child has a medical issue that usually lands us in an ER 3x’s a year. We have no debt and we haven’t gone on a vacation in a while because it can’t bear to pay the outrageous airline prices with such bad service these days. Our shopping is primarily done at Costco – buying in bulk is best, our wardrobe for work is filled with the same clothes we’ve been wearing for 5 years+.

We pay hefty taxes and yes we give to charity. By all means we are not rich. Sure we go out to eat once a week but that’s usually to some kid friendly place like Pei Wei or the Grocery Store Cafe. Nothing fancy.

We save as much as we can but still we’re not rich. I can’t go buy a BMW or Mercedes. Despite what people may speculate about families who make over $200k. I will say that at work, my employees make the same as me. Therefore, I know my peers are making WAY MORE than I do. I just want to put that into perspective for you all. It is not difficult to make $200k HH income these days with 2 white collar workers in the household. The challenge is being able to reduce our AGI and actually keep more of our money.

Good perspective, and thanks for sharing! Hope you stay warm in MN now that winter is coming!

You may enjoy this follow on post: Scraping By On $500,000 A Year: Why It’s So Hard To Quit The Rat Race

This is so clearly a case of people making their own hell through poor choices.

You mean the high income earners or the low income earners who are subsidized by the high income earners?

I have spent 80k (progressive fees depending on salary) on medical in the last 5 years. Still making monthly payments. Now we are facing college tuition. I think we can swing paying 100% cash by eliminating vacation, using state school, etc – but darn, no tax breaks or subsidized loans are even available! My parents both lost their health (one died) at my age, so why shouldn’t I want to have a few nice things to enjoy if I earned them? I certainly wouldn’t begrudge you for buying something frivolous with your own cash! Good thing we have decent 401, but I will have to downgrade the house because it won’t be paid off when we retire. Your welcome.

And this is why I haven’t moved to the San Francisco Bay Area. I could make twice the gross pay I make in my state. However, state taxes would take out a chunk of that increased paycheck (I pay none in my state). I would be in a higher tax bracket, so I would pay more in federal tax as well. The cost of living would be substantially higher. In the end, I have more disposable income with the lower rate of pay in this state than I would in most areas of California.

The author’s numbers are off, and highly skewed.

Even in 2015, a married couple with $200k income, no health / dental insurance premiums, and 3 exemptions (including their one child) would only have $32,243.50 withheld for taxes. That’s a 16.12% effective federal tax rate, not 22%, until you add in Social Security and Medicare. However, the narrative text added it in again.

While they likely should save more than 9% of their income (and likely do if they receive any matching money), it points to the fact that they’re not necessarily “pressed” for every dollar.

Furthermore, they somehow have a $500 per month car payment, and $100 per week for gas. That’s an expensive car that doesn’t just guzzle gas, it opens its throat and shotguns it based on current gas prices.

Add 2 $4k vacations per year, and $8k in “charity, consumer debt, and miscellaneous” expenditures, while still having more than 10% of the median household income left over, and they’re clearly not hurting (just whining).

The Personal Exemption amount ($4050 per person = $12,050) is money that is not taxed. As stated in the article, $25,200 is mortgage interest that is also federally tax-exempt (deductible). Add that to the state taxes (probably around $15,000, which is deductible on Schedule A, and you have a federal deduction totaling $40,000 or so. The effective tax rate is thus, nowhere near the 30% that the author claims. It is closer to 15% for federal and about 6% for state.

Given that, the “What’s Left” line should look closer to $20k. And if you pull out all the excessive and egregious spending (like two $8000 vacations lol), the bottom line to the savings account should look closer to $30k.

I make $200k and live in Silicon Valley. My taxes is $30k federal and $10k state. Oh, by the way, when you first start out, I recommend donating all $2,000 to your favorite charity… YOURSELF! But you should donate when you’re older, the kids have gradated college, and you’re settled down and fat and happy.

Two vacations for a total of $8K is by no means egregious. Flights alone can cost $3-4K. Add food, accommodation and transportation for 7 days for a family of 3-4 and it easily adds up to $8K for one week of vacation.

A flight for $3-4k?? Are you serious? Please find me one. Unless you are specifically interested in vacationing at whatever remote village in a Congo is the absolute most expensive to get to, you will be throwing away money to pay *half* that. You are shockingly out of touch.

I’m pretty sure he meant $3-4k for the whole family round trip

$900 pp to Europe easy.

How in the hell did you leave out health insurance? Don’t forget the huge deductible too!

Right? Can count on their companies to pay for healthcare.

It’s game over for this family! :)

True words..

I live in SF, and I earn six figures a year (lowest end).

I have no kids or anything like that. Life is really tough.

I feel like I’m earning so little after all the bills and rent.

I feel the pinch everyone is talking about, and I hope it will ease up some day.

Any thoughts?

I would find a company that allows you to telecommute from a cheaper location in America. It’s becoming for more popular and you can make close to San Francisco money but cut your costs by 70%.

Identify what in SF is crucial to your happy life and find those things elsewhere. I’m serious. When I moved from Los Angeles, I missed all the ethnic restaurants, but soon realized those restaurants were the element that made life in L.A. bearable. They were unnecessary to my happiness. What I really miss are the long evenings that come from being in a more southerly location than I am now. Lots of southerly locations in the U.S.!

We are a family of 4 living in Southern Ca. My husband works full time making 60K a year, about 42K after insurance, 401K and taxes! and I go to school full time. I take night classes to avoid child care costs. We go one two $500 “vacations” a year. not very fancy or long but nice local getaways. Each child has one “activity” which costs us about $1000 a year total… My point is there are ways to cut the fat! We spend less on “vacations” and less on “child activities”… We are able to save 5K a year without any debt! If we can do it anyone can! and honestly, I don’t even feel “poor”. I feel rich! i live in a safe home, I eat healthy foods, my children are healthy, no our home doesn’t have new wood flooring, or chic color pallets, but it is filled with 4 people that love each other very much!

Of course there are. But the point is that if you earn a good salary, it’s still normal to want to do extra things with what you earned. When you are younger, I think it’s easier to sacrifice because you have your whole life ahead of you. Then when your kids get college-aged, you realize that “oh crap,” I have to try to start my bucket list! But you really can’t because you can still ‘trim the fat’ to help subsidize …(name anything but your own desires).

All of those expenses seem so plausible and as though cutting them a little wouldn’t make much difference. It makes me grateful I don’t have and don’t want children.

We earn a similar amount to this couple, and live in a similarly expensive city (Sydney, Australia), but our budget works out much better, mainly because of not having kids:

Income: pretty close to $200k (I earn $130k and my partner alternates between $60-120k depending on whether his job has enough funding to pay him full time or half time). So say $200 total as an average.

Taxes: $55k

So net income = $145k

Mortgage payments = $24k (Sydney has a median property price of around $1 million, and ours was $900k, but we had a good downpayment, so the mortgage repayments are low).

Mortgage interest = $8000

Home maintenance = $3000 (we had to buy a fixer-upper to get a below median price house, so there are a few biggish expenses each year)

Property rates = $4000

Home insurance = $1000 (we have a large deductible to keep this low)

Electricity = $1200

Water = $800

Car insurances & registration = $2000 (only 3rd party person & property)

Car maintenance = $1000 (we have an old beater, so no payments, but it always needs maintenance)

Fuel = $1200 (Because it’s Sydney, we live a long way from work (in opposite directions each so we can’t exactly live closer): my husband drives and I take the bus or cycle, depending on weather)

Bus/train fares = $1500

Bicycle maintenance = $300

Food = $8000 (we only eat out about once a month, take lunches to work, etc but we do like things like cheese, wine, and fresh produce, which are not cheap in Australia).

Clothes = $300 (we mostly thrift shop)

Travel = $5000 (our families live in different countries so we have to visit them at least once a year, plus we try to have a (cheap) vacation once a year as well.)

Medical expenses = $2000 (private health insurance + a few expenses it doesn’t cover)

Gym membership = $1000

Phones = $600

Internet = $800

Subscriptions = $180

TOTAL = $56k, leaving around 90k per year in savings (minus miscellaneous costs which seem to average no more than a couple of thousand per year).

The difference between us and this couple are: we don’t have childcare payments; no children’s classes or meals; less in the way of insurance cost; cheaper vacations; no car payment; no consumer debt; less property tax; less on clothes. On the other hand we don’t get any mortgage deductible in Australia.

I would love to only have $2000 cost for medical for my wife and I. Count your blessings.

Wait, if 401K is 18K that means this budget is based on one earner and not two or else 401K would be 36K. If so not sure if child care should be 24K. On the flip side child classes of 5K might be too low once we take into account of summer camp.

This looks very much like our family’s budget.

We live in Seattle, where the going price for a house is $400 per square foot, or $800k for a 3 bedroom, 2,000 square foot house. (pretty basic)) Our mortgage is $3,500 with taxes.

We have two kids – infant and toddler. Infant daycare is $2,000 per month, and $1,500 per month for toddler in Seattle, so we decided to pay a nanny at $18 per hour for full time – about the same at $3,500 per month.

That means just our house payment and childcare is $7,000 per month….leaving about $3,000 for everything else, food, healthcare, utilities, two cars (we both work in outside sales and need a car).

We don’t go on vacation ever! Not luxurious.

Good thing you are long and strong Seattle, one of the hottest real estate markets in the world!

Related: Why Is US Property So Cheap?

Late to the party, but $24k/year for childcare??? I *wish* I could find such cheap daycare. I’m using a “cheap” McDaycare facility near my home in Boston that only costs $35,000/year. It doesn’t offer any special program, no foreign language, nothing – it’s just a run-of-the-mill daycare. A “quality” daycare here would be in excess of $40k/year. Maybe I should move to SF to get that sweet low cost of living :)

* – of course, this is largely offset by higher salaries, but it’s fun to complain…

Glad you chimed in and can help provide your Boston data point to the other naysayers who think childcare isn’t so expensive.

San Francisco is the cheapest international city in the world. Come on over!

Wow – adjusted for taxes, you need to make $50k (well over median personal income and close to median household income) just to cover daycare costs. Is it really worth having two income stream or can one spouse work from home?

My 200k/year of the last couple years looks like this for wife and I (will be ~250k this year and ~300k next year – mortgage will be going up as we’re building a new house but otherwise expenses will stay the same:

Gross Salary: 200,000 (one income, no kids)

Income taxes (including FICA): 50,000

401k: 12,000 (can’t max – company doesn’t meet safe harbor rules)

NQ Def Comp: 25,000

Mortgage (including taxes/hoa/insurance): 13,000

2 Cars (loan/taxes/insurance/maintenance): 11,000

Gas – 2,000

Student loans: 7,000

Other Debt: 6,000

Food/Bev: 12,000

Wife’s clothing/makeup/hair budget: 5,000

Utilities: 3,500

1m life insurance = 400

Misc = 3,000

Dogs = 1,500 (including insurance)

Vacations: 10,000

Gym: 1,000

Cable/Internet/Cell: 2,500

Gifts: 2,000

Life happens: 5,000

Healthcare: 3,500

Roughly 175k-180k a year in expenses, including ~40k in 401k/def comp. This is Charlotte area. Expecting to have all debt but the mortgage paid off in the next 18 months.

“Wife’s clothing/makeup/hair budget”…PRICELESS!

“adjusted for taxes, you need to make $50k (well over median personal income and close to median household income) just to cover daycare costs. Is it really worth having two income stream or can one spouse work from home?”

This is a good question, but not so simple. Leaving the workforce for 5 years to take care of a child until they go to kindergarten can have a really detrimental effect on one’s ability to find comparable work from what they left, and they will be more likely to re-enter the workforce at the level (or below) from when they left. So even if all your income goes to childcare, it may still be worth it.

Also, working from home with a child is not an option (unless you don’t actually plan on working). Can save some childcare costs if you don’t have to pay for care while commuting to an office, but any parent will tell you that kids don’t sit quietly for 8 hours while you do your work…

The example provided doesn’t even included telephone/cell, internet service, television provider, gym membership, etc. I’m assuming these things weren’t meant to be covered under home maintanenance becuase that would leave no room for utilities, which I’m sure aren’t cheap in SF. There is also auto maintenance, gifts, etc. I also think $12,000 for food for a family of three in SF is very conservative. Perhaps if the family never eats out (only buys groceries at Walmart) and never enjoys a Starbucks it would be possible. The example also only has one of them maxing out their 401K (18K). Based on recomendations I repeatedly read here, this couple should be able to add another 18K to their 401K (max out both) and save an additional 20-75% of their net income (20-75% of 109Kish). Obviously this is not feasible even if they were living on ramen. I’m thinking that maxing out 401K (36K) and saving an additional 20-75% of net (22-82K) would require a family to make at least double (400K) or certainly not live in California.

I think $12,000 per year is totally doable for food. My family of 3 lives just outside SF and we spend $700 per month on groceries (Trader Joe’s and Whole Foods mostly) and another $200-300 on lunches, eating out and coffee. I only eat out at work once per week and usually at a place with salads and sandwiches for $10 or less. And date nights are more likely drinks and/or an inexpensive dinner, not often steakhouses and trendy places. But it doesn’t feel like too much of a strain. Certainly not ramen!

Good article

Just goes to show that feeling rich is more about your mindset rather than how much money you have. There should be another study to ask people what they actually mean by “rich”

it means so many different things to different people that its almost become pointless as a word.

If both people are working why are they not putting $36,000 into their 401K? That would lower their tax bill. Does it really cost $2000 a month for one child in childcare?

Yes, the chart shows taxable income declining by the amount of their 401K contribution.

Yes, it does cost $2,000 a month for one child for childcare in places like SF and NYC.

Related: Abolish Welfare Mentality: A Janitor Makes $271,000

Looks like Trump is actually raising taxes on 200k earners! The 33% bracket kicks in at 112k, screwing over middle class earners in expensive places like the Bay Area.

Looks like it is an attempt to get rid of the marriage penalty. 33% bracket kicks in at 112,500 for singles, and 225,000 if married. Exactly twice the single level. The standard deduction goes up almost 250%. Some tax cut but not as much as I was hoping for. Might be time to hitch up and save!

Good observation, and you’re right. I can’t see how the middle class $120,000 – $200,000 income earner has to pay a 5-8% increase in taxes. I don’t think his tax regime will pass.