Since I started Financial Samurai in 2009, I have been on a mission to help readers achieve financial freedom sooner rather than later. And one of the core strategies I keep coming back to is encouraging readers to get neutral on real estate by first buying a primary residence. Once you have secured your primary residence, you no longer are at the mercy of ever rising rents. Inflation is too difficult a beast to defeat.

Once you get neutral real estate, you can eventually get long real estate by adding rental properties over time. Owning more than one property is the only way to really benefit from appreciation, unless you sell your primary for a profit and downgrade to a cheaper home.

But while I have been on this crusade since the housing market crashed in 2009, there has been an equally loud, if not louder, crusade against homeownership. I'm not sure why.

Perhaps it is the lingering psychological aftermath of the global financial crisis, where it is always easier to be against something after it has declined in value. Or perhaps it is because roughly 40% of Americans do not own homes, and most of them skew younger, with louder voices online.

I understand the skepticism. It is completely human to be against something you do not own. But when it comes to building wealth, the market does not care about your opinions. It cares about numbers. And for the average person, I genuinely believe it is easier to make more money on real estate than stocks.

Let me show you exactly what I mean comparing two exciting examples between real estate versus stocks.

Making Millions On A Home Is Easier Than You Think

I have a hobby that most people find a little strange: I go to Sunday open houses. Not because I am always looking to buy, but because it keeps me connected to the market, given ~40% of my net worth is in real estate.

I get a feel for pricing trends, pick up remodeling and interior design ideas, and get my steps in walking through neighborhoods I appreciate. It is one of the more enjoyable and educational ways I spend a Sunday afternoon.

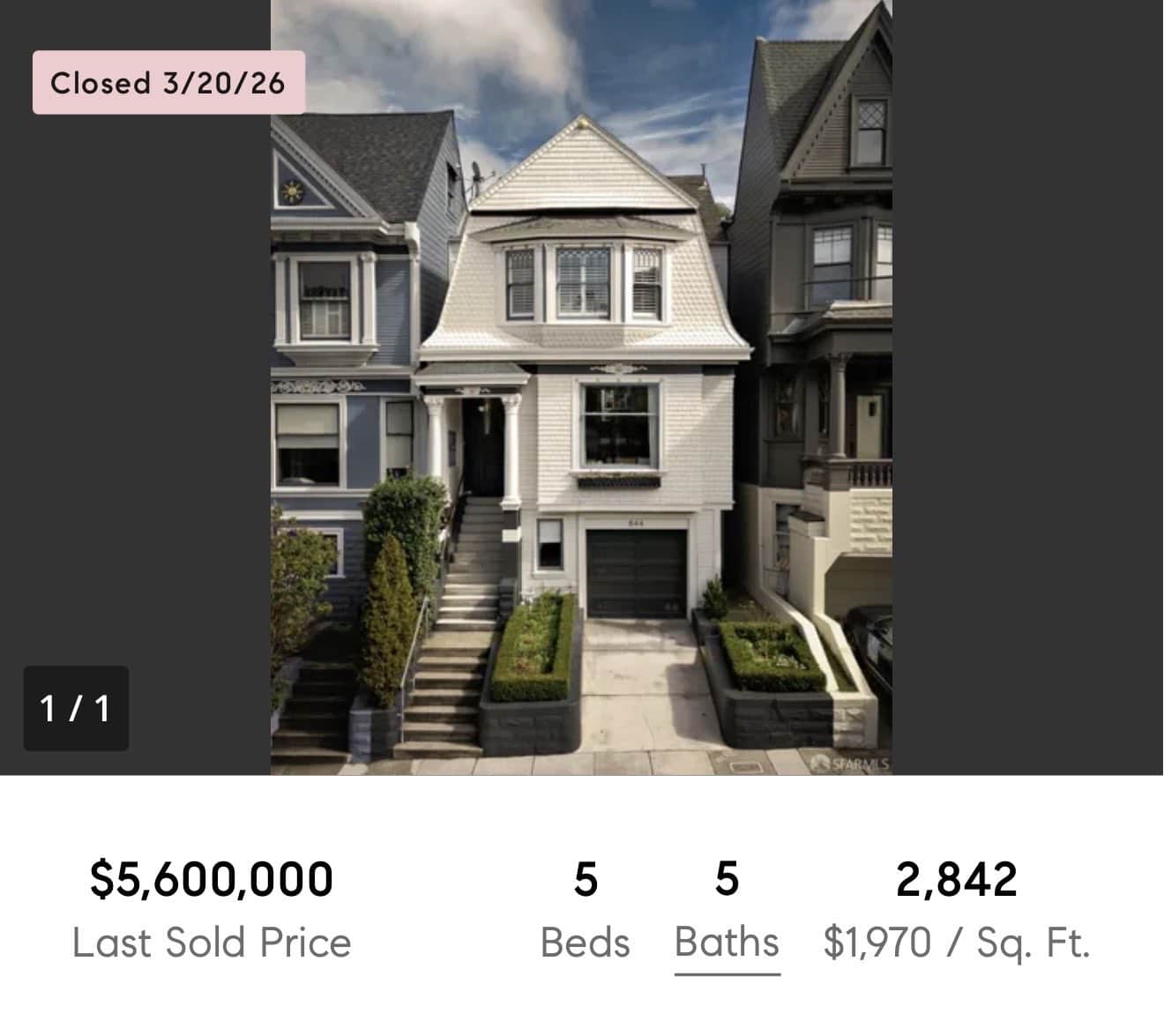

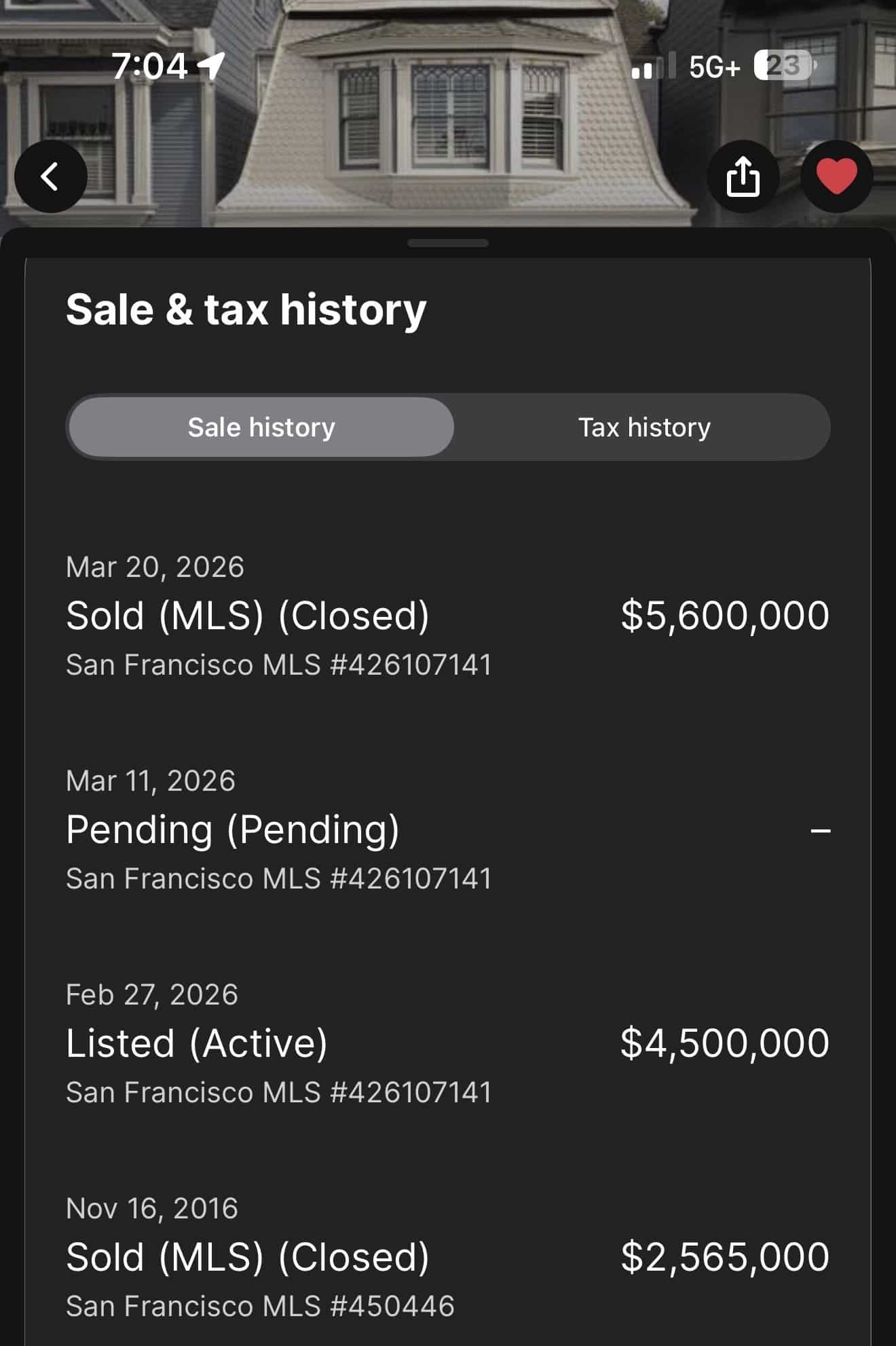

On one of those Sundays, I toured a single-family home in San Francisco listed at $4,500,000. It was a beautifully remodeled five-bedroom, questionable five-bathroom property with about 2,842 square feet – the kind of place my family would happily call home.

The downsides were it sat on a busy street between Cole Valley and Ashbury Heights, and the primary bedroom faced that traffic while offering only a three-quarter bath with a shower and two sinks, but no soaking tub or toilet. I've never seen that before, as the toilet was down the hall.

I made a mental note of it to check back in a month. Here's the history.

Tremendous Price Appreciation

The buyer purchased the home in late 2016 for $2,565,000 with 20% down, putting $513,000 in as a down payment. Over the following years, I estimate they invested another $300,000 into a thoughtful remodel, opening up the downstairs layout, remodeling another bathroom, and adding a quarter bathroom upstairs. The work was done well.

Total cash invested: ~$813,000.

Ten years later, the home sells for $5,600,000. After real estate commissions, transfer taxes, and paying off the remaining mortgage balance, the seller walks away with approximately $3,600,000 in cash proceeds.

That is a 4.43 times multiple on invested capital and a 16% internal rate of return over ten years.

Let those numbers sink in for a moment.

The Numbers Get Even Better

Here is where homeownership starts to look genuinely extraordinary compared to almost any other investment.

If the sellers are married, they qualify for the federal capital gains exclusion on primary residences, which allows them to take up to $500,000 in profits completely tax free. That is not a loophole or a workaround. It is a benefit Congress deliberately built into the tax code to encourage homeownership, and it is one of the most powerful wealth building tools available to everyday Americans.

But the math gets even more interesting when you factor in the cost of living.

Over those ten years, the family had to live somewhere, which is why I say you're only neutral real estate if you own a primary residence. If they had rented a comparable home in San Francisco instead, they would have spent somewhere between $2 million and $2.5 million in rent over that decade, money that would have disappeared entirely with nothing to show for it.

As a homeowner, the cost of the mortgage, property taxes, insurance, and maintenance was largely offset by what they would have paid in rent anyway. In other words, they essentially lived in a beautiful San Francisco home for free for ten years while their net worth quietly compounded in the background.

They raised their children there. They hosted dinners, celebrated birthdays, and built memories in a space that was entirely their own. And at the end of it, they walked away with $3,600,000.

How is that a bad investment? Please, feel free to tear up my argument if you're against real estate.

The Confidence To Make A Large Investment

One of the most underappreciated aspects of real estate investing is the power of leverage. When you put 20% down on a home, you are controlling a $2,565,000 asset with just $513,000 of your own money.

In this example, the home appreciated by roughly $3,000,000 over ten years, before accounting for any remodel. That appreciation accrued entirely to the homeowner, not the bank. The mortgage lender got their interest payments. The homeowner got the wealth.

Try doing that with stocks. Under Reg T, the maximum margin allowed in a standard brokerage account is 50%, meaning you would need to put up $1,282,500 of your own money and borrow another $1,282,500 at steep margin rates, often 10% or higher for years. And that is assuming your brokerage will even extend you that much credit. More importantly, that borrowed money comes with no patience.

Margin calls in 2018, 2020, and 2022 forced countless investors to sell at exactly the wrong moment, locking in losses they never would have suffered if they had simply been able to hold. With real estate, the bank cannot call your mortgage because the market dropped 30%. With margin, your brokerage absolutely can, and will.

In practice, most people looking to deploy $2,565,000 into equities have the full amount in cash, precisely because of that volatility. The structural leverage advantage that real estate offers everyday investors simply does not exist in any other mainstream asset class.

Stocks Are Far More Volatile, Therefore Harder To Go All-In

This is why I have long argued that real estate is less risky than stocks, even with leverage. It is far easier to commit to a large down payment and leverage it 4x when you are buying something with tangible utility. Worst case, the home's value drops, but you still have shelter for yourself and your family.

Stocks offer no such consolation. When they tank, you are left staring at red numbers on a screen, wondering why you didn't take profits sooner. This is why few households that decide to buy a house and raise children will have a 100% equity position. A more appropriate 80/20, 70/30, or 60/40 equity/fixed income split would be more likely.

The Forced Savings Element

You have probably heard some version of this argument: renting is smarter than buying because you can invest the difference and come out ahead. On a spreadsheet, under ideal conditions, with perfect discipline, this can sometimes be true. The math is not wrong.

The human beings running that math, however, almost always are.

In theory, someone who rents and diligently invests the difference between their rent and a hypothetical mortgage payment for 30 years will accumulate significant wealth. In practice, the money gets spent. Lifestyle upgrades, vacations, a nicer car, private school.

The discipline required to execute that strategy perfectly for decades is extraordinarily rare. I have been writing about personal finance for 17 years, and homeowners in my readership consistently come out far ahead of renters who planned to save and invest the difference.

Homeowners, meanwhile, build wealth almost by accident. Every mortgage payment is a forced savings contribution. You do not decide whether to make it. Make it, or you lose the house. That behavioral constraint, which feels like a burden in the early years, turns out to be one of the most powerful wealth-building mechanisms available to ordinary people.

Not Everyone Can Buy In San Francisco. And That Is Okay.

The example above involves a $2,565,000 home with a $513,000 down payment and $300,000 in renovations. I am fully aware most Americans cannot replicate those numbers. That is not the point.

The point is the structure: leverage, forced savings, tax advantages, and utility all working together over time. That structure works in Columbus just as well as it works in San Francisco. It works in Raleigh, Austin, Nashville, and Boise. The dollar amounts change. The mechanics do not.

That said, I will make one ambitious argument.

You live in America, a country people spend years trying to reach, and you have the freedom to live and work anywhere within it. That freedom is worth using strategically. If you want to maximize your earning potential and your real estate appreciation, where companies are being built, where venture money is being deployed, where jobs are being created.

If your career and net worth are not growing the way you hoped, the answer might simply be geography. America gives you the freedom to change that.

But They Could Have Made More Investing In VCX!

Since I cherry-picked a top tier single family home sale in San Francisco, it is only fair to highlight a top tier equity investment with deep San Francisco roots: VCX, whose top three holdings are Anthropic, OpenAI, and Databricks, all headquartered in the city. Fundrise is a long-time sponsor of Financial Samurai and Financial Samurai is an investor in Fundrise products as our investment philosophies are aligned.

On paper, if that same $813,000 had been invested in VCX before its NYSE listing on March 19, 2026, the returns would have dwarfed the already impressive 4.4X real estate multiple.

But here is the thing. Nobody would have had the courage to put $813,000 into VCX right before the listing. Even fewer people had heard of Fundrise's venture fund at all. Fewer still would have the discipline to hold on rather than sell after a double, triple, let alone a quadruple. And even fewer are able to sell at the top.

Buying A Single Family Home After Having A Baby Is Normal

Think about who actually buys a $2,565,000 home in San Francisco (about 37% above the median price back in 2016, and ~20% above today. They are a couple that likely earn between $400,000 to $700,000 a year, have significant living expenses, a net worth of around $1 – $3 million, and perhaps $300,000 left to find a remodel.

Earning $400,000 – $700,000 might sound like a lot, and it is. However, 23-year-old college graduates working in big tech earn $200,000 a year. If they marry another big tech colleague 10 years later, they are likely earning far more. And we have tens of thousands of these jobs here in the SF Bay Area.

To want to buy a single family home after getting married and wanting to start a family is absolutely normal. A majority of couples have this plan. Heck, I sold my old home, which turned into a rental for three years, for a similar amount back in 2017 to a couple with a one-year old. I wanted to simplify life because managing the property was a PITA and we had just had our first child.

Meanwhile, paying a 37% higher than median price for a single family home back in 2016 is still in the frenzy zone, where demand is elevated because so many people can afford up to the median price plus 50%.

Going All-In On A Venture Fund Is Abnormal

Conversely, investing the entire $513,000 down payment into a venture capital product you read about on Financial Samurai would be completely abnormal. Let me show you why.

First, you would have to have found Financial Samurai and kept reading until you read one of my articles about Fundrise's venture product between 2022 and February 2026. Generously, that is a 10% chance. Most people find Financial Samurai through a search, read the article, and never subscribe to my newsletter or return on their own.

Then you would have to have had the conviction to invest in VCX before the listing based on my rationale. Given that the vast majority of people read but never act, call that a 5% chance.

Finally, you would have had to have invested a significant enough amount to generate $1 million or more in returns, as the homeowners did with their real estate. Even at a 10x return, that means putting in $100,000 to get $1 million, and $300,000 to match the homeowner's return of $3 million and then actually selling at the right time. Fewer than 1% of readers had that conviction.

The math does not lie: 10% x 5% x 1% = 0.005%. One in 20,000.

A More Realistic Amount You Would Have Invested In VCX

The standard recommended allocation to alternative investments like venture capital is no more than 20% of a portfolio. So in practice, a couple in this position might have had the conviction to put $50,000 into Fundrise's venture product before its NYSE listing, but highly unlikely.

More realistically, they would have prioritized buying a home and living comfortably, putting perhaps $100,000 into the S&P 500, and maybe $10,000 – $20,000 into the venture product instead. Remember, they need to set aside $300,000 for remodeling. They either have most of it, or are saving their cash flow until they get it.

I say this as someone who has followed Fundrise's venture product since the beginning in 2022. And even after thinking carefully about what the NYSE listing could mean for investors, I could only bring myself to invest $12,000 beyond my existing $1,000-a-month auto-invest for the past two years and my previous lump sum purchases.

With bombs flying, oil prices and interest rates rocketing, and the S&P 500 melting down, my conviction was lukewarm. The value of a stock or equity fund could drop by double-digit percentages overnight.

No couple takes their entire home down payment and redirects it into a single alternative investment instead of buying a home to raise their family in. That is not how human beings actually make financial decisions.

The Wealth Building Stack

Here is how I think about building wealth, in the right order for most people.

First, buy your primary residence as soon as you can reasonably afford to while maxing out your 401(k) and IRA. Negotiate hard, write the real estate love letter, use every edge available as I've shared in my archives. Every year you delay is a year of compounding you never get back.

Second, once your home is secured and your financial foundation is stable, aggressively rebuild your taxable brokerage portfolio. Continue maxing out your 401(k) and IRA throughout.

Third, as your brokerage portfolio grows over the next two to five years, consider adding a rental property. The combination of rising rents and appreciating prices, while costs remain largely fixed, is one of the most powerful long term wealth building engines that exists.

Fourth, once you have the core foundation in place – primary residence, maxed retirement accounts, a healthy taxable portfolio, and at least one rental – you can begin diversifying into passive real estate funds like Fundrise. This gives you exposure to markets beyond your backyard without the headaches of direct property management.

Fifth, if your foundation is strong and you have capital you can afford to be patient with, consider an allocation to venture capital funds. Private companies are staying private longer, therefore, it's only logical to allocate more capital to private markets. Only if you are extremely wealth (net worth equal to 50X income or more) should you consider angel investing in individual companies. Most will lose all your money.

This is not a get rich quick stack. It is a get wealthy inevitably stack, built on boring, proven mechanisms that work for ordinary people in the real world. Skipping the first four steps to go all in on venture capital is highly risky. Build the foundation first.

The Bottom Line

The San Francisco home in our example was not purchased by an investing genius or a lucky speculator. It was purchased by a family who made a straightforward decision to buy a home they wanted to live in, improve it thoughtfully, and hold it for a decade.

The result was $3,600,000 in cash proceeds, a decade of free housing, $500,000 in tax free profits, and a lifetime of memories built inside walls they owned.

The anti homeownership crowd is welcome to poke holes in this argument. I genuinely mean that. The comments section is open.

But the numbers are the numbers. And after 17 years of writing about wealth building, I have yet to find a more reliable, more accessible, or more behaviorally sustainable path to making millions for ordinary Americans than buying a home, living in it, and letting time do the work.

Have you made significant money on a home? Or do you believe renting and investing the difference is the smarter long term play? Why do you think there is a growing voice against homeownership? I would love to hear your experience in the comments below. Again, Fundrise is a long-time sponsor of Financial Samurai.

Keep In Touch And Lend Some Support

If my writing has helped you financially over the years, the best thing you can do is pick up a copy and leave a positive review on Amazon for my books, Millionaire Milestones and Buy This, Not That, and leave a podcast review on Apple or Spotify. Every review means a lot.

And if you want more real-time thoughts on markets, real estate, the economy, and investment opportunities throughout the week, join 60,000 other subscribers and sign up for my free weekly newsletter. I have published three times a week since July 2009, when I helped kickstart the modern-day FIRE movement. Everything I write is based on firsthand experience.

40+ years of real estate investment & we always avoided equities until cashing out a lot of properties when we entered our 70+ years. Since 2000, everything we & our kids owned was free & clear & no debt. I was lucky to invest the property selling cash into AMZN & now sell OTM covered calls on it all, bringing in a nice 5-figure return every 3 months. Admittedly, I’ve had some close ‘calls’ on being exercised, but nothing like the sleepless stress of watching a stock portfolio drop 20-30%.

Most of our family members are equity proponents, always telling us we are doing it wrong. BUT instead of chasing dividends & single-digit MMkt returns, the many notes we hold on the properties we sold provide a consistent 10-12% passive income stream.

I’ve invested in single family homes and apartments. I’ve invested in the California and the Midwest. Held over a long period of time (10 years), I absolutely lost my shirt in the Midwest and made a ton of money in CA. For the last 4 years (since interest rates starting climbing), I’ve made no money in real estate. I’m barely hanging on as my mortgages (all commercial loans are ARMs), taxes (including bus license, property tax, inspection fees) insurance and repairs increase. Insurance companies and governments are mandating new electrical panels, soft story retrofits, appliances, roofs, etc. while rents are mostly flat. I go through on average two evictions every year where tenant lives at my property rent-free for 6 months (because its CA). Real estate is NOT easy money and it is NOT steady cash flow.

I agree a primary residence exempts you from all the landlord problems. But if you lived in the Midwest where prices have been flatter, you’re better off investing money in the stock market.

If you live in SF where appreciation is stronger, yes you can go all in on a big house and all the accompanying expenses (bigger house means more maintenance cost, more furnishings, more cleaning, etc.), or just buy a house that’s the right size and buy Apple stock 10, 20 or 30 years ago. Heck, we are picking selective examples of investments in hindsight, why not?

My own home has been an incredible investment. I bought it for $750K 23 years ago and now it’s worth $2.0M. I had a down payment of $150K. Had I just paid down my mortgage over time, I would have ton of equity in the house…doing nothing for me as an investment. If you go with the house as a financial investment strategy, you need to constantly do cash out refis (at hopefully low interest rates) so you can reinvest the proceeds, which is exactly what I did.

However, that strategy has come to an end. I have a $1M mortgage at 2.375% for 30 years. I have a $1M equity in the house that I can’t unlock except through a HELOC (not likely to use at 6.5% to 7% rates).

Thanks for sharing. ” I go through on average two evictions every year where tenant lives at my property rent-free for 6 months (because it’s CA).” That is BRUTAL.

How many rentals do you have? If I went through even one of those experiences, I would sell that one particular property immediately. Life is too short to deal with that.

Mr. Samurai!!!

I like the RE vs stock discussion. I’m 39 and have about a 2:3 ratio of RE:investment portfolio. I’m grateful I bought great properties for my jobs at a good price at the right time and developed solid equity over the past 12 years. I’m currently not working and the only city that’s calling is SF, so moving from Boston to SF is a huge deal to me mentally. I love my current home that’s on the water, but there’s 500k equity and I feel like renting it is too much of a risk (HOA, renovations, etc.). Putting that equity into my investments sounds more attractive to me (with potentially renting in SF).

It’s surprising to hear how many people tell me to rent it out, but when you’re able to identify a solid growth company with a valuation lower than the S&P e.g. GOOGL last year, it’s hard to not want more money to thoughtfully invest rather than sit on a property with so much risk when renting. 500k, if invested well, could get me a property with that next level “wow” factor down the road.

I align more with investing, but I don’t hate diversifying with properties that make sense to keep.

Keep up the good work. I hope you always write these, because I always read them.

M

Hi Sam,

Do you mind sharing the zillow listing – happy to share how I usually do the math on buy vs. build to get your feedback?

Alternatively what would be most useful is 1- the estimated real estate taxes paid by the owner and 2- the z-estimate for renting. (Taxes in California real estate is a huge cost in the balance of buy v.s rent).

Thank you, Sam!

Hi Ben, all the details you need are in the post because you can back out the property taxes based on a 1.123% rate. And then you can also see how much it cost to rent a place like that over the years and make the calculations.

I think homeownership can be a great investment, but only under certain conditions. It tends to work best if you stay in the home for a long time, usually 10+ years, and you are willing to put in the time or money to maintain it.

In my case, the outcomes have been mixed. The first condo I owned essentially broke even after a large special assessment that was about a third of the value of the property. The second home was purchased a few years before the Great Recession and sold about nine years later with only a modest gain. I have built meaningful equity in my current home over the past 10 years, but that has come with ongoing costs, maintenance, and unpredictability.

Even recently, I had an issue with a fairly new roof that turned into a bigger problem than expected. Situations like that are part of owning a home, but they do add up over time.

At this stage, as I look toward retirement, I am thinking more about flexibility and how I want to spend my time. I would rather unlock the equity and use it to support early retirement and a more mobile lifestyle. I want the option to spend extended time in different places and be closer to friends and family, which is harder to do when you are tied to a house.

I also think it depends on where someone is in life. I have a friend in her early 50s who rents and has chosen to stay in one place while her child is in school. She is getting pressure to buy, but it does not align with what she wants right now. Renting gives her stability without the added responsibility and cost of ownership.

So for me, homeownership has been a useful tool, but it is not automatically the best choice forever or for everyone. It really depends on your goals and how you want to live.

Best,

E

I’ve been following your blog for about five years now. During that time, I was able to invest a small amount into Fundrise, but I ended up missing the VCX opportunity. At the time, I was hesitant and unsure how the market would react, especially since many companies tend to drop in price shortly after going public.

Lately, I’ve been thinking more about the San Francisco real estate market. I’m curious are there any properties going into foreclosure there? I remember hearing that, in certain areas, at least one home enters foreclosure each year, and I wanted to see if that still holds true today?

No worries. There is always another investment opportunity.

I am sure there are properties going into foreclosure every single month here in San Francisco. It’s the same and City. You just have to go find it as well.

This is the beauty of investing. If people make the effort, they can sometimes succeed. There’s no stopping you or anybody from looking.

Great article! We are happy to have fundrise through you. Question: what price will our innovation fund be listed at when it was converted to vcx?

Response:

Hi Sam, this is another great post!

Funny thing is, the way you broke down how to get wealthy eventually is pretty much exactly what I did over time. Plus, I’ve only once made over $100k in a year to create ~$3M net worth by age 54.

At age 54 I lost my job and at that time, I was transitioning to a plan to purchase turnkey properties out of state. I live in CA and homes are too expensive, as you know, to have positive cash flow. So, now I have 7 properties and 8 doors in Arkansas, Texas, and Tennessee. My job now is to manage my portfolio since I can’t even get an interview these days. However, I don’t think I could handle working a W-2 job in an office anymore since I’ve tasted the sweetness of FIRE. I miss the interactions with co-workers and the excitement of the weekends, but it’s so nice to be able to do what I want when I want.

Since my experience with buying turnkey real estate, I wrote a book called Turnkey Real Estate Investing. In a nutshell, I wrote about what I did to get to 5 doors; at the time, I only had 5 doors. I’d love to send you a free signed copy of my book, if you’re interested. Let me know where I can mail it and I’ll get it out to you right away. My email address is cstevens21@gmail.com.

For your readers, if they’re interested in my book, the e-book is on Amazon right now for only 99 cents. Readers can get the Kindle version for free if they have Prime! Here’s the link: https://www.amazon.com/Turnkey-Real-Estate-Investing-Strategies/dp/B0DMTJF8NF/ref=mp_s_a_1_2?crid=1I6NZ22DPFA0Y&dib=eyJ2IjoiMSJ9.aNUsI1BtTR76p_fHmfm_2-rJTG8U3uPLBH60VAxX-fgpF3R1yQmFigXZFtUmh-Wv3lPwDyY1MrQ-zWND7kAAc_kVXhfn1ba9uEhrbOwn8acN9JIUfKMcJWsWCe75bJT3r9jcrZ0eKcFxj7eOmMdoUCsfx_Bzl9Ktyt7HFMJs5CAGu0MnHS0Tq575lW5qG6BKbr77HE1fZuLJea3n_jtQQQ.JCNNzaFPwOGnJ372hYBL2_xgpkVAxdLDgoXGX8vS1KI&dib_tag=se&keywords=turnkey%2Breal%2Bestate%2Binvesting&qid=1774800845&sprefix=turnkey%2Bre%2Caps%2C192&sr=8-2&th=1&psc=1

I enjoy helping people grow their wealth, too, which is why I wrote the book. It’s not a money maker, but it sure was fun to do and publish.

If any of your readers read this and also want a free signed copy, I’ll send out copies to the first 20 requests I get in my inbox, as long as they’re in the United States. Postage to other countries is SO expensive. It cost me $17 to mail one to a podcaster in Canada! It’s only ~$4 sending them thru media mail in the U.S. I can absorb that, but not internationally.

I’d love to get reviews on Amazon. You know how hard it is to get reviews, so it would be greatly appreciated. I’m at 63 and I’m trying to get to that magical 100.

Thanks, Sam! Keep up the terrific work.

Sam, greatly appreciate the research on VCX. Invested 35k pre-listing and will reexamine after lockup expires. Decided to buy 100 shares in a Roth at $90 average, sold@525. Not bad for 4 days work .

Not bad! Feel free to share some of your good investment ideas as well so the rest of us can make some money too. Thanks!

I will say that once you learn option strategies (things like LEAPS and synthetic longs) and understand when to buy (not at all time highs but upon dips) the leverage can be remarkable. You can control hundreds of shares for a fraction of the price, and sometimes with no margin interest at all. While real estate is probably more realistic for the average person, this newsletter is for the above average person! (Right?). Options, done smartly, are way more powerful. And I also own real estate properties so I get it.

I thought I read somewhere on one of your recent blog posts that you were looking to deploy new money into the S&P if it hit 6500. Right now it’s just under, curious if this is still your current plan? Holding cash and it all feels so volatile right now but also don’t want to sit on too much cash, not interested in bonds, gold, bitcoin or vcx (for now).

Yes, buying the S&P 500 here, especially for my kids’ custodial accounts.

Thanks for writing out your view on your “Wealthy Building Stack”. I know you talk about the ideas in lots of differently articles, but it is good to see if written very concisely/simply.

Great article. I’m younger than you and make way less (also much lower COL), but most of my NW has been from live-in flips. The fixed-rate, 30-year mortgage has got to be the greatest benefit to the working-class American of all time. Even at 7% rates, you won’t find a better deal anywhere else, and if you can find a lendable house that needs some TLC, you may have just hit the jackpot. USA!

Thanks for the article, I am fortunate enough to followed the steps above (by luck?). I have been working for 30+ years. I live in a coastal city, but I have had a few rentals in non-coastal cities (phoenix and atlanta). Appreciation is ok, lived through the 2009 crash, the two I have left are cash positive. It’s been a journey, in my view real estate over the long term in non-coastal cities are about income then appreciation. I do feel for the younger generation though… things seems a little bit out of reach. I feel that I am the last generation that can start from nothing and end up ok… I am really struggling to see this for the next generation. Any thoughts?

With so much wealth accumulated by the Boomers and Gen X, I think the younger generations will be OK so long as the older generations share the wealth and assist.

Hi Sam, thank you for the many insights over the years. I am the 20 something year old tech employee you mentioned in your post who just recently became a homeowner. As of today however, my pre-IPO VCX shares are now worth more than all my other assets combined. It is surreal looking at the statement but it also makes me uneasy that my wealth is so concentrated into one single symbol. I am long AI and see its revolutionary potential everyday in my occupation, but I also feel eager to lock in profits in 6 months so I can diversify into rental property and other equities. Curious what you’d say to 25 year old Sam, if in a single week, a stock exceeded the value of all the assets he’d worked diligently for his whole life.

Hi Michael, congrats on your investment success so far. How did you discover VCX?

Having a proper asset allocation is key as you age.

Here’s a post about net worth asset allocation by age and work experience that’s worth reviewing.

This is precisely why the current market value is completely unsustainable in the medium term. If anything, the experience of watching the huge life-changing numbers they have been looking at and daydreaming about evaporate into a mirage before their eyes while enduring Iran-induced cost of living increases and AI displacement dread will cause tens of thousands of small investors to bring out the pitchforks. I would be very careful on your cheerleading at this point, Sam, lest you become one of the targets.

Target for what? Trying to find a way to protect my family from AI’s potentially disruptive effects on the labor market for my children?

Are you getting displaced by AI? If so, what are you doing about it? It’s always good to try and find solutions to problems.

Sorry I should have been more clear. I was specifically referencing the financial & likely professional profile of the median locked-up VCX holder, who maybe had $20k at pre-IPO and yesterday was staring incredulously at a $500k figure on a screen that now forms the bulk of their net worth and can lead to unhealthy dreaming. When that disappears before they have a chance to realize their phantom gain, as market and intrinsic value converge over the next 5.5 months, there is going to be massive disappointment. Inflation and potential job losses are background noise to this and will just serve to increase anxiety and (eventual) rage. At Ben, at you, at Galloway, etc. It feels like a real risk. You have caveated it well so far, but need to be careful IMO.

As shareholders pre-listing, hopefully most of us have conservative expectations.

I’m assuming you are a shareholder which is why you’re commenting. If so, what are you doing with your Shares, the unrestricted ones?

My philosophy is to stay conservative and make it known that you could never lose if you lock in a gain.

https://podcasts.apple.com/us/podcast/the-financial-samurai-podcast/id1324765509?i=1000757460508

Good pod, even if it took you 20 minutes to get to the rub. It also throws up challenging allocation rebalancing issues, not just risks around immediate spending commitments off the back of illiquid appreciation. I would also acknowledge the absolutely asinine implied valuation at Wednesday’s peak, shown best here. How do you decide when to do a pod vs post?

Cool, if you have a podcast, I’d love to hear it as well. I’m always looking to improve my speaking. The good thing about the podcast is that it’s easy to skip around and increase the speed.

What are you doing with your shares of VCX?

You’re selectively choosing examples. We all know San Francisco real estate has been expensive and has seen some of the strongest appreciation over the past decade—so yes, this person made money. But by that logic, what if they had put the same money into something like Nvidia stock (also a cherry-picked example)? The returns could have been significantly higher.

That’s why the argument that “it’s easier to make a million through real estate than stocks” doesn’t really hold up. In reality, far more millionaires and billionaires have been created through equity investing than through buying homes.

Thanks for your thoughts. Curious if you read through the article talking about the probability of a couple with a baby wanting to buy a home versus the probability of investing the same amount in Nvidia or any other speculative investment.

I used VCX as the cherry picked extraordinary equity example to counteract the real estate example.

Where do you live and how is your real estate market over the past 10 years? If you could check out some of the points, can you bring up that I have written in the article, I think it would make for a great discussion. Thanks.

One important aspect of making mistakes with Stocks: Checking Every minute, day, minute, getting excited, Depressed with ups & Downs & Making 1 mistake can wipe out Entire profits, portfolios which is a common thing with mos tof the investors.

Indeed. The liquidity of real estate and the difficulty to sell can save many homeowners from panic selling at the wrong time.

Think about how many times we’ve sold stock only need to watch it continue to go up up and up.

I am so thankful I wasn’t able to easily sell my home my own back in 2012. I signed in agreement to list it and I couldn’t find any reasonable buyers because it was still uncertain times post the global financial crisis. Five years later, due to circumstance, I was able to sell it for much more.

What do you anticipate VCX’s (thus far very successful) listing has done to the value of Fundrise. They’ve allowed investors to

buy a portion of the company (Fundrise) a few times. I haven’t heard or seen anything estimating how this might impact the overall value of Fundrise the company. Any thoughts?

It’s a great question. The success of the venture product should provide a dramatic boost to Fundrise’s company valuation. It managed about $2.8 billion in real estate AUM and $550 million in venture AUM pre-listing. The current value of VCX is now 10X-20X that, so they’ve proved they can create public venture capital as an asset class.

So if Fundrise were to create another VCX, and go about fund raising and investing in the same way, I’m confident it could easily raise another $500 – $1 billion in capital immediately. The challenge will be finding new winning investments.

If Fundrise becomes the Sequoia or Benchmark of public venture capital, then it could be worth a fortune. Redefining an asset class, and now must grow and execute.

Anything is possible.

I like both real estate and stocks and for different reasons. Growing up my parents made it sound incredibly hard to invest in either one and a lot of that was due to their lack of funds but also their lack of knowledge and experience. So I feel fortunate that I didn’t let their doubts stop me from getting educated, not being afraid to do hard things, think outside their box, and continually try to learn new things about personal finance from sites like yours. And wow SF real estate and VCX continue to amaze me. The examples you shared are crazy mind boggling.

Hi, Sam. I found Fundrise because of you, and, on a lark, invested a a bit ion VCX. Right now, it looks insane. We’ll see in 6 months. I admit I did not do a search for prior posts on rental property, but I won a rental in Florida. It’s a pretty nice place. Not only has it gone down in value, but new roof, new retaining walls, new this, new that, has made it even worse. So, for me, the rental real estate has been a money pit where I have zero positive cash flow over the last 5 years, and the value has gone down by $100k. So, how does one make money from a rental (and, by the way, I inherited the place and have no mortgage, which make this even worse)? What’s the secret?

Sorry to hear about the rental property. If you inherited it, wouldn’t that be considered immediately profitable though, unless it was underwater on a mortgage?

I’ve got a ton of property buying posts in my archives if you search in the field. Here’s one: How To Correctly Value And Analyze Rental Properties

what do you think vcx will be priced at after the 6 mo lockout period?

It’s anybody’s guess at this point. Have a listen to my latest podcast out on March 26, 2026.

Anything above $100 I think would be a huge win. But I could see international demand and the entire retail universe want to invest, which could keep the price elevated even higher. Only SpaceX will likely go IPO this year, leave all others in a high demand position. And if SpaceX doesn’t great, then demand for the other privately held companies increase.

What are your thoughts and analysis on real estate versus stocks, and VCX? Are you an investor?

I’m hoping to get more perspective besides me just sharing my analysis. thx!

Another out of touch post about overpriced property in a coastal city. 95 percent of people can not relate no matter how much “you can do it anywhere” cheering from the bubble.

Believe it or not, roughly 50% of the US population lives in coastal city, such as San Francisco, Los Angeles, Seattle, New York, Boston, and Miami.

So just because these examples are not your reality, doesn’t make the reality untrue for those that do face this reality.

And my experience, those who can see things for what they are tend to be better investors who more efficiently connect the dots.

Feel free to share where you live and what you’re seeing in the real estate market. Reading different perspectives and learning from them is always great.

As much easier to wear slippers than Carpet the world.

I can only speak for myself, but as one of the 5% to 50% of the US population who does not live anywhere near a coastal city (Midwesterner), I find the magnitude of the numbers in this post to be extremely unrelatable (I purchased a home four years ago for about $250k), but I find the principles extremely relatable. The perspectives here and my experience since purchasing my home fairly well mirror each other and both reinforce the home buying decision as the correct choice. I just feel guilty for letting my sister get to the age she is and still be renting. But giving family members financial advice rarely goes well for me.

All good. If we can ignore the numbers for a bit (the home purchase and sale) and think about the fundamentals of inflation, leverage, forced savings, etc, I think the result is the same. It’s easier for the average person to build wealth through real estate than through stocks.

And I hear you on feeling guilty letting your sister age and still rent. There is insecurity involved with renting, especially as rents keep getting pushed higher where she lives.

You’ve reminded me of this post: Please Don’t Rent Your Entire Life: Housing Security Is Vital

IF it makes you feel better, less than 5% of readers listen to my advice, and I’ve been sharing my thoughts for 17 years, worked in finance, got an MBA, have written over 2,500 articles, introduced the modern-day FIRE movement in 2009, and broke free in 2012 with enough passive income to never have to work again. Oh, and then there’s the VCX investment as well.

At the end of the day, people are rational and will do what they want to do. So we can’t worry about them!

Related: You Can’t Save The World, So Mind Your Own Finances

Thanks for the post Sam, which I mostly agree with.

Looking at the property photos, unless we can see the condition of the house in 2016, the current condition looks to be freshly renovated/refurbished.

If so, given its a large house, that refurbishment looks to have cost more than $500K (and possibly in the region of $750K/$800K) as it is very high end with garden landscaping. I very much doubt that would have cost ‘only’ $300K…

I am writing from the UK so I am probably completely wrong but UK building costs for that size of house to that high specification and in an equivalent location would be eye-wateringly expensive.

It would be helpful if you could show how you arrived at the $300K figure…

Hi mate, I appreciate your skepticism. I actually toured the house during the open house and spoke to the realtor and asked what the previous sellers did. They told me they did interior painting and opened up the back. And then they installed the weird half bath with a shower, two sinks and no toilet. Then they remodeled a couple of bathrooms.

Spending about 13% of the value of a home on a remodel is pretty common. I have gutted completely two homes before and those costs were between 15 to 18% of the total value of the home.

So based on my conversations, my experience, and checking out the property in person, I came up with $300,000. And this is from 10 years ago. That $300,000 remodel might cost $500,000 today.

And I do believe more people are willing to pay a premium on remodeled homes now because they are such a pain in the butt.

Thanks Sam.

As the kitchen looks fresh, I assumed it was new (I notionally allocated $100K+ cost in my mind), however if most of the works (excluding those the estate agent/realtor confirmed were completed by the current vendors) were done buy the previous owners, then $300K current spend looks to be more justifiable.

The capital growth experienced is much more a function of the local economy GDP in SF (driven by large tech business valuations and gains). In London, the opposite story is true – house prices in the nicer areas have been flat since Brexit (2016) and the underlying (but unspoken) story is a real-terms house price correction of around 20%+.

Your key point though (which I very much agree with) is that the rental payments would have been similar to the mortgage payments, but mortgage payments allow the option to increase equity and net worth whilst benefitting from accomodation that no-one (except the bank) can take from you.

Even with flat house prices in London, the forced savings scheme (paying down mortgage debt) is accretive to net worth.

Let’s say $100,000 for kitchen, $100,000 to open up downstairs, $20,000 to build the weird tiny half bath, $50,000 to remodel another bathroom and a half, and $30,000 for random whatever.

$300,000 is in the ballpark.

London post Brexit is strange. But most voted for it right? So they have to be happy with the results and have seen benefits elsewhere?

London as a whole voted to remain in the EU; the rest of the country chose to vote Leave. Its fair to say that Brexit has been negative for the UK economy, with no practical economic benefits.

Ah, gotcha. That is frustrating. Sorry to hear. Hopefully you have and can continue to diversify away from England assets since Brexit?

That’s just one of those frustrating things where you just never know, hence why nobody should make fun of those of us who diversify.

Hey Sam! I did follow your lead and do some investigating into Fundrise years ago and am happy to say I decided to invest. I invested 33k over several years, and am very curious to see what that turns into after the 6 month lock up. Thank you for sharing these findings with us! I share them with my community too and the letters of gratitude are pouring in. They all roll up to you!

Additionally to offset the FOMO of the 6 month lock up, I invested in VCX on IPO day in my Roth IRA. What a great place for a IPO pop :)

Now whatever happens with the remaining money, I’m happy.

Congrats for being part of the estimated 0.005% who took action! It’s worth staying conservative with expectations. But seeing the $33K turn into $650K a week after listing must feel thrilling.

If you’d like to show some love, please pick up a copy of Millionaire Milestones and leave a review. Every one counts. My kids will be proud of their old man one day.

Thanks and congrats again.

One hole I’d like to poke is the fact that buying a home and affording the payments is becoming increasingly impossible for most American jobs. Sure, you pointed out tens of thousands of jobs in tech in SF. What about the majority which are everyday people such as teachers, service workers and waste management? It’s not reasonable to assume they can buy a house and outlay >60% of monthly income on the payments. So those people just have to move to somewhere affordable? Leave everything they have? This is perhaps a different question, the affordability question, but it’s tied together. If you can’t buy a house without being cash poor, it’s not worth it. I think a lot of places are becoming too expensive, so you might as well rent and save the stress. This is what the anti homeownership crowd more so points to. It’s not that they are against having a home strictly for math. It’s just better to not lock in for a decade in a place on the outskirts of town or far from your community because you have to. Nobody wants a long commute because they bought a house 1.5 hours away since it’s the only place in budget.