If you read about the 1031 exchange, you'll immediately think it's the greatest thing on earth for real estate investors. What's not to like about paying zero capital gains tax after the sale of a property? However, this article will discuss the various reasons not to do a 1031 exchange to save on taxes.

The government already taxes real estate investors through an annual property tax and a transfer tax upon sale. Having to pay capital gains tax on the way out can be very painful. This is especially true since real estate prices have surged to all-time highs in many areas of the country.

This article explores the other side of the 1031 exchange. We will talk about reasons not to do a 1031 exchange to save on taxes. As a real estate investor, it's always wise to understand both sides of the equation.

First, let's discuss what is a 1031 exchange.

What Is A 1031 Exchange?

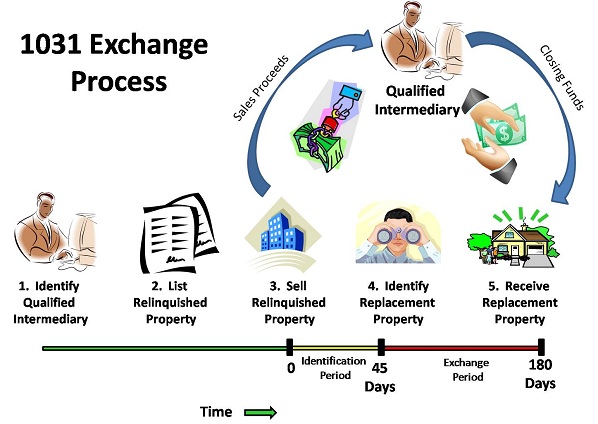

A 1031 Exchange allows an investor to “defer” paying capital gains taxes on an investment property when it is sold, as long as another “like-kind property” is purchased with the profit gained by the sale of the first property.

To do a 1031 exchange effectively, you must exchange one property for another property of similar value. Further, the purchase price and the new loan amount has to be the same or higher on the replacement property.

Why I Considered Doing A 1031 Exchange

In my case, I had to find a single family or multi-unit property worth at least $2,740,000. I could find a property worth less than $2,740,000 after I sold it. However, then I'd have to pay the capital gains tax on the difference in sale price and purchase price of the new property known as “boot.”

The property owner has 45 calendar days, post-closing of the first property, to identify up to three potential properties of like-kind.

After the properties are identified, the investor has 180 days to make the purchase and initiate the exchange OR by the due date of the income tax return with extension, whichever is earlier.

Finally, you've got to pay a Qualified Intermediary anywhere from $1,000 – $3,000 to hold your proceeds (you never get to see or touch the proceeds from your home sale) to conduct the exchange.

If you are unable to identify and buy a new property, you lose that money and all that time.

Main Reasons Not To Do A 1031 Exchange

Now that we understand what is a 1031 exchange, let's discuss reasons not to do a 1031 exchange.

1) You don't mind paying taxes

2) You haven't found the right property

3) You want to reduce exposure to real estate

4) You want to simplify your life

5) You've lived in your rental for at least two of the past five years. Therefore, you can take advantage of the $250K/$500K tax-free profits

Why I Didn't Do A 1031 Exchange

In 2017, I sold a rental property for $2,740,000 in San Francisco. As a new father, I just didn't want to deal with rowdy tenants and maintenance issues anymore. Further, rents were dropping a little at the time.

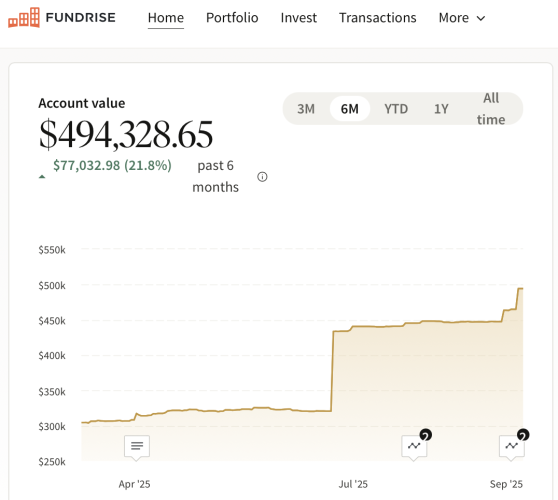

I decided to reinvest $550,000 of my sale proceeds into real estate crowdfunding to simplify life. So far, it's been a great move as the investments have returned over 10% a year. Further, all the income earned has been passive.

Trading one expensive property for another expensive property just to save on taxes wouldn't achieve my goals of simplification. After selling, I felt a little like I escaped death. I had gone through the financial crisis with a huge mortgage and came out unscathed.

With an equally expensive San Francisco property out of consideration, I looked at Honolulu property for a 1031 exchange. We had considered moving back to Honolulu once our son became eligible for kindergarten.

Given Honolulu is cheaper than San Francisco, we'd end up buying an even larger property through a 1031 exchange. That wasn't simplifying life. Or, we could buy our retirement dream home near the beach. But it would have to be rented out for at least one year, if not two years for it to be considered rental property by the IRS.

1031 Exchange Through Real Estate Crowdfunding

Finally, I asked Fundrise, my favorite real estate crowdfunding platform, whether they had any properties on their platform eligible for a 1031 Exchange. At the time my house was to close, they said they didn't, but that something was in the works.

About a month after my transaction closed, Fundrise sent me an e-mail saying they had launched their first 1031-eligible property. It was a 272 unit multi-family project looking to raise $4,500,000 in Houston, Texas. It had an 8-year holding period, and a 13% target IRR.

I'm fine with an 8-year holding period. However, with $2,740,000 million to put to work, I would take up more than 50% of the deal size. I don't recommend anybody account for greater than 10% of any deal due to concentration risk. Further, think about how stressed I would be before, during, and after Hurricane Harvey hit.

As I thought about this close call, I realized the primary purpose of de-risking and simplifying life is to minimize stress. Up until my son was born, almost all the stress I had was dealing with real estate maintenance issues and tenants.

De-risking Is About Stress Management

I already got rid of work stress in 2012 by negotiating a severance. I got rid of money stress by hitting a net worth target and reaching a passive income goal. Online work is not that stressful because writing comes easy to me. There are only a few truly thoughtless people who like to say unthoughtful things.

From a financial perspective, although the gross gain from selling my rental home was ~$1.22M and ~$1.8M hit my bank account after years of paying down the mortgage, the taxable gain is much less due to the $250K/$500K tax-free gain exclusion. Then there are selling expenses and home remodeling expenses one can deduct to lower tax liability.

For example, theoretically, I could pay no capital gains tax if I spent $600,000 remodeling the house and $150,000 selling my house. When you add the $500K tax-free exclusion, the total is $1,250,000, or more than the gross profit I received.

In this example, the negative of not paying taxes means the gains weren't much greater than the tax-free gain exclusion amounts. But at the end of the day, I'm left with $1.8M in the bank. Not bad compared to the $305,000 downpayment I first down in 2005.

I've set aside $150,000 for capital gains tax (federal + state) next year. It's been nice to not own this rental property anymore. Maintenance and tenant issues seem to always come up!

Focus On What's Most Important

For all of you considering doing a 1031 exchange, consider these reasons on why not to do a 1031 exchange.

1) If you cannot find the right property to reinvest the proceeds, don't do a 1031 exchange.

It would be foolish to try and save on taxes, but then lose principle value because you bought the wrong property at the wrong time in the cycle. You might feel a lot of pressure to identify three properties to purchase in 45 days. Then you might pay a bad price since you've got to close within 180 days.

Unless you absolutely love the next investment property, it's not worth doing a 1031 exchange.

2) Don't let your tax bill dictate your decisions.

A large tax bill is usually great because it means you made an even greater profit. I remember plenty of folks during the 2000 dotcom bust who refused to sell their stock after they exercised their options because they wanted to let things ride.

But when their stock eventually went to zero, not only were they left with nothing, they also had to pay taxes on the difference between the exercise and the strike price at the time. Only do a 1031 exchange if you've found the right property opportunity.

3) Focus on lifestyle first, money second.

Your real estate investments should serve you, not the other way around. Even if we found our dream home in Honolulu, we wouldn't move because we don't want to leave our lifestyle in San Francisco just yet.

We just finished completely remodeling our house. We have our doctors we've trusted for years and a pediatrician and ophthalmologist we like for our son. We've got a set of friends we enjoy hanging with. And we've also scoped out and applied to several pre-schools too.

4) Will you really be able to hold on forever?

A 1031 Exchange allows you to delay paying your taxes. It doesn't eliminate your capital gains tax. Only if you never sell your 1031 exchanged property or keep on doing a 1031 exchange, will you never incur a tax liability.

You can pass on your property to your children who get to step-up the value to current market value. This way they never have to pay taxes on your property either.

It's only after your assets exceed the estate tax limit ($13.61 million per individual in 2024, $13.99 million per individual in 2025) do your heirs need to pay ~40% tax on anything over. The median holding period for property in America is between 7 – 8 years.

5) Do you really need the rental income?

A 1031 exchange is exclusively for rental properties, not primary residences. Therefore, the primary reason to own rental property is for income. Income streams can change over time, as they have for us. I thought we would need the rental income forever because we never wanted to go back to work.

Little did we know that during the three years we tried renting out the house, our online income grew to the point where we definitely didn't need rental property anymore. Even if our online income was slashed by 80%, we still wouldn't need any portion of our rental income in our passive income portfolio.

That said, post-pandemic, I am bullish on rental properties. As a result, I'm actively seeking to invest in multifamily properties and build-to-rent properties on Fundrise.

A Simpler Life Feels Great

In a perfect world, I would have 1031 exchanged all the proceeds into a diversified private real estate fund that returned at least 10% a year forever, guaranteed.

Alas, I was unable to find such an opportunity. I've already redeployed over half the proceeds in 100% passive investments. The remaining proceeds will more than likely stay liquid in order to finally buy that dream home in Hawaii one day.

If you would like to do a 1031 exchange, I recommend identify a handful of rental properties you want to buy before proceeding. This way, you do the 1031 exchange much quicker without as much pressure.

The housing market will likely stay strong for a very long time. Therefore, owning real estate as part of your investment portfolio is a wise move. Just make sure you are doing a 1031 exchange for the right reasons.

Free Financial Analysis Offer From Empower

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”). Click here to learn more.

Diversify Your Retirement Investments

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution, and I want to ensure I have enough exposure—not just for myself, but for my children’s future as well.

I’ve personally invested over $400,000 with Fundrise (my investment dashboard above), and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

Reasons Not To Do A 1031 Exchange is a Financial Samurai original post. I've been writing about achieving financial freedom and investing in real estate since 2009. Join 60,000+ others and sign up for my free private newsletter today.

Thank you so much for this article. So many online talk about why to do a 1031 but no one really mentions the why nots. We decided not to do one and feel much better about it since I can take my time looking at other properties that don’t cost as much as the one I sold and have can diversify the proceeds into other investments as well.

Is there ever a time you would pay annual taxes on a 1031 that you are holding? I have one for 5 years, i’m in year 2 and don’t take dividends. Being told there is tax I need to pay on this investment annually – its a commercial property. Makes no sense to have 1031 and pay taxes — what am I missing?

Can I take the $250k exclusion as well as a1031 exchange?

You stated “…although the gross gain from selling my rental home was ~$1.22M and ~$1.8M hit my bank account after years of paying down the mortgage, the taxable gain is much less due to the $250K/$500K tax-free gain exclusion.” But, isn’t this a rental property? Doesn’t the $250K/$500K tax-free gain exclusion” only apply to primary residences? I am confused… But great article!

Not necessarily. It depends on if you own the property and lived in it as your primary for at least two of the past five years.

Check this post out: https://www.financialsamurai.com/tax-free-profits-for-home-sale-250000-500000/

You cannot turn a rental into a primary by living there two years and get the 500k exclusion. You have to pay the gain made for all those years abd pay tax on the depreciation. The only portion that is cap gains free is years it was your primary. Two years. So if you own a rental for 10 years, and move in the last two, you owe cap gains made during the 8 years. A

Correct. See: Clarifying The $250,000 / $500,000 tax-free profit exclusion rule. Rules have changed over the past decade.

Great info. I am not a RE investor, however, I own, work, and live out of a commercial bldg. I’ve owned since 1996. I am in Culver City Ca which RE is booming. I am 62 and want a simpler life. This property is my nest egg basically. In 2000 I leveled the old house and built a 2 story mixed use bldg. My S corp pays me rent. If I did 1031 would I add the price I paid in 1996 plus the cost to build the new bldg as part of the cost basis? Valuations for my place have been at 2.2 – 3 mil.

Being single my exclusion would be 250K. After reading this article, I may skip the 1031, take the tax hit, have no debt (I owe 383K now) and move out of Calif.. I have a small Fundrise acct also, for about 2 years now. Not sure i have temperament to do a 1031 or to be a landlord. Thanks

Purchased duplex in 1991 for $305. We live in the unit and rented the front for several years. Thinking of selling and moving to Oregon. Confused about 1031 or 250/500 deduct. The front unit had been vacant for two years because we remodeled and we don’t want tenants ruining our hard work so daughter just moved in. Bay Area duplex worth 1.9 now. Thoughts ?

I’m struggling so much with a decision right now, please help me decide what’s best to do! I have spread sheets, figures, calculations, and all the stress. I sold my waterfront rental property because the second home market exploded with people flocking out of DC to the coast after COVID. My profit is $167k. The sale price was $650k which means I need to buy something $650k or higher. With tightening lending rules regarding 1031 exchanges, I must put 35% down on the new investment property. I have a $767k waterfront place under contract – which means I’ll need $264k down. My whole profit above doesn’t cover that so I’ll need to pull out an additional $97k of cash from elsewhere to complete the purchase. Annual expenses on the new $767k waterfront house will be around $40k. Projected rents will be around $46k. So it will pay for itself, and I’ll have a little left over each year to set aside for future expenses. I will get to enjoy the new house occasionally as well when it’s not rented. I’m still in my due diligence period and can terminate my contract before October 29 if I choose to. Im paralyzed with indecision. I want to create passive income but I don’t know where or how to do that. Your talk about passive income sounds wonderful. But the new waterfront house doesn’t give me much passive income does it? Should I not move forward? I don’t know what to do. It’s 1:00 in the morning where I am and I can’t sleep trying to decide on this. I’m praying for guidance. Would love your thoughts.

Hi, i just bought a 1031 exchange property with only 21 percent down from the sale thatbalso covered my closing cost. Youbdont need to put 35 percent down. I went through Optionwide financial Corporation and they got it done. I got nonconventional loan and so my interest rates are a bit higher but with no prepayment penalty in 3 to six months i can refinance. So you can try talking to them.

I’m a novice too but you can consider selling your house and going into a 1031 without buying another house – many of these companies invest your money and you have a nice return, like rent, without the hassle of renters and that whole process

I have never heard about a 1031 exchange without buying another house. Please explain this. Thanks.

My husband and I own our home in Walnut Creek and our mortgage is reasonable as we purchased in 1998. As a nurse and butcher with three kids, we have depended on the income from renting our our childhood home my brother and I inherited in the Marina/Cow Hollow District of San Francisco (classic two flats on Filbert St). We finally have the top flat empty and my brother and I are tired of being San Francisco Landlords. We make a good team but our old neighborhood is no longer the Italian blue collar bastion it once was, and the type of renters we get now are pure hassle. Brother is an SFO cop and wants to buy his primary home now. However, my husband and I will miss the $3,000 a month rental income that gave us freedom to work less back breaking hours. We figure we will earn 1.3 from the sale of the Marina house. What would you suggest we invest it in? We are considering picking up two condos around $600,000 in the Concord/Martinez/Walnut Creek area. We are also considering a vacation rental condo in Oceanside or Maui in developments we like to use when we vacation. However, It seems nothing will give us the monthly income that renting the Marina house under prop 13 property tax gave us. I was thinking investing in condos would be easier than upkeep on a single family home. Any advice you are willing to share with a fellow traveler?

Sam – I was researching for a client pros and cons to do 1031 or not and I came across your article. I am a long time reader and a subscriber.

Grace – I’m licensed to sell 1031 DSTs, it’s totally passive investments. There are pros and cons doing 1031. If you would like to communicate with me; providing Sam wants to provide my email address. I’ll be glad to provide more details on the investments I currently have.

Pete

I bought a daycare for 350k 15 years ago. The city never allow me to do the daycare. So it just sat empty. The city developed and now I’m about to sell it for 515k. I would like to buy a small property as an investment and make some extra cash. If I don’t do a 1031 exchange and I buy property for say 400k, will I pay capital gain on the difference or on the entire 515k? Should I do a 1031 exchange? Please help?

I put 25% down on do a 2nd home in CA. Then realized the mistake and converted it to a rental. After two years, sold in a 1031 Exchange for two homes in AZ. After two years, sold those in a 1031 taking a bit of a boot and purchased a SFR in TN. My value went from a small cash down to buying a house all cash and it is an Airbnb. No taxes. I’ll watch the market and do it again or hold. I love 1031 Exchanges. It’s an easy way to gain wealth.

can you recommend 1031 exchange Qualified Intermediatery you worked with.

Great article! Was just in Hawaii and it is quite beautiful just make sure you spend a fair bit of time out there before the big move if you haven’t already.

I am in the process of selling 2 properties and wondering if I can combine the proceeds into purchasing 1 property using the 1031 exchange?

Also, how would that play out with the numbers if I’m selling for $320K (gain $120) and $250 (gain $150)? Do I have to buy new property for $570k or just use the gains of $270K?

Thank you!

I have completed a 1031 Exchange.

My question is now what?

Do I depreciate two properties – continuing for the remainder of the years on the

relinquished property and starting the depreciation of the 29.5 on the new property?

I’m wrestling with this as a limited partner. The sponsor is talking about selling and doing a 1031 exchange into a larger property.

I don’t have to deal with the minutiae of the 1031 exchange as an LP. I like the idea of avoiding taxes, but I’m not sure I trust that he will be able to find a good deal in a short period of time. The market seems to have peaked or be peaking, and the motivation for this deal seems to be to tie up more assets for a longer timeframe before there is a recession and a pullback in prices.

Paying record high prices for an asset doesn’t seem like the recipe for exceptional returns. On the other hand, I’m hard-pressed to think of alternatives that will beat RE. I guess it would be nice to sit on a pile of cash for when there are deals in stocks or property that I can control directly.

After a 1.2 MM 1031 exchange in 1/17 I acquired a 577k home, a 140k condo, and an 440k small apartment bldg. Fast forward to now, condo was destroyed by upstairs remodeler by flooding me out, lawsuit pending as no ones insurance will pay. I have buyer for condo. May I use proceeds of condo sale (130k) to remodel the 440k apt building? If not, do I pay the capital gains commensurate with the profit percentage and keep the difference?

I’m at day 10 of my 45 day period in finding a replacement property for my 1031 exchange and it is driving me crazy finding a place in southern CA!

I’m in a unique predicament where I just sold some farmland which my father had given me 30 years ago. I’m currently renting an apartment and my lease is expiring in a month. Since the IRS specifies that one must not live in the 1031 exchange property immediately after purchasing it, I will have to rent out the house or condo I buy. Meanwhile I’ll have to find another rental to live in.

From what I’ve read so far, the IRS doesn’t specify a time period to rent out a 1031 exchange property before it can be converted into a primary residence. The main crux is the INTENT to rent it out as income property. Thus I’m thinking of using the 1031 exchange as an AirBnB so I won’t have to rent it out full time and I can let my friends stay in it on occasion. Maybe I’ll do this for a year and then move into it. Does anyone have any thoughts on this strategy?

By the way, it’s interesting reading these posts that no one else has exchanged farmland. Of course only one percent of Americans own farms so it shouldn’t be that surprising. There is such a startling contrast between property values in Los Angeles county compared to rural middle America. I will be exchanging 300 acres of land for a 1000 square foot condo!

The 1031 Exchange lawyers I spoke to recommend renting out the property for at least one year. After that, your intent is met and you can move in.

Why did you sell the farm land? And where was it?

Interesting. I’m looking to 1031 into farmland.

Another consideration for a 1031 Exchange in California is that you must continue to update the California revenue board via your annual taxes on the property that you did the 1031 Exchange IF YOU HAD BOUGHT A PROPERTY OUT OF STATE. I currently own a rental property in California but live in Colorado. When I sell my property if there are any Capital gains in the House I’ll just pay the taxes so I can be done with the People’s Republic, I mean State of California revenue board.

My 1031 exchange ten years ago was the sale of the final piece of a three building seven unit complex exchanged for a 2% tenant-in-common interest in a day care center six states away. The income isn’t as high as the active landlord decade, but the stress of cashing the monthly checks is infinitesimal. The transaction was the fall back when none of the locally available properties suited me.

I own a company in which the only asset is a building (approx. valuation of $1.2 million) and generates net rental income (approx. $35,000 annually). Thinking of selling the building to buy another business which does not have any real estate assets only goodwill and strong income history. Basically exchanging a tangible asset with high R/E taxes and limited income potential to purchase a business with no assets and a much higher rate of return. Thoughts Mr. Samurai?

Now why would you take 1.2 million that could work for you in the bank rather than investing it in a business and then you would have to work for it? You can buy bonds or other safe investments that would generate that same income without using any of your principle. That’s if you want a peace of mind and a leisure lifestyle. But, if you want take 10% and start another business.

FS,

It would be interesting to see a post with your excellent thought process and insight on the proposed tax law changes. I read that there is proposal to change timeline to legally convert an investment property to primary home from 2 out of 5 yrs to 5 out of 8 yrs.

Ouch – that hurts my plan.

My aunt did a 1031 exchange and it worked out well. She did it because I was her niece and could be trusted as a tenant and property manager. It was perfectly timed because I didn’t want to rent a small room in a bigger house anymore and she didn’t want to immediately pay capital gains tax on the sale of her rental house.

The purpose of our money is to help secure our happiness, and you seem to be doing just that. Good job not letting the tax tail wag the dog and doing what made sense for you instead.

I did a 1031 exchange last year. We sold our condo and exchanged for a duplex. The return on the duplex was much better than the condo for many obvious reasons. Overall I am happy with the exchange.

I do find multi unit tenants to be more demanding. Single family tenants are usually very independent.

One way to minimize stress of 1030 is to extend the selling escrow. You let your buyer have a 2-3 month escrow after removing contingency. This way you lock in your sell, but give yourself and then 2 more month to close while you identify you next property. Essentially you get about 3 month to identify 3 properties. It was still stressful. In theory you can negotiate more time with the party buying your property thereby minimizing the time pressure.

I am in contract now for another tenant occupied fourplex. Seems like trouble tenants. Need to find an excuse to get out of this contract.

For my scenario a 1031 was a nice program to take advantage of.

All the “more simplicity” and “do I want to be a renter” questions had already been asked and answered.

We wanted to get out of some midwest property as we had moved to west coast and were not close enough to properly manage. We still enjoyed the benefits of being landlord and a positive cash flow.

Once here, we were able to learn market and find similiar property and terms. The 1031 exchange did allow for a more painless transition and the delay of cap gains is nice. I fully envision a lower income when we want to sell and we may even live in it for a few years to turn some gain into a tax free exclusion.

Probably would have done the transaction with out the 1031 being available, but hey – more gravy is a good thing right?

This sounds similar to Canada, except if you have a primary residence you pay zero capital gains tax at all when you sell. This is probably one of the reasons why Vancouver is now the most unaffordable city in North America (when average household income is accounted for).

That home in Kailua looks amazing- oceanfront! Is that the neighbourhood you would be looking at if/when you would move to Oahu? I hear the Diamond Head area is also very nice.

Hi Sam, did you account for all the depreciation expenses that offset rental income during the years the property was rented out? The depreciation expenses reduce your cost basis, which would increase your capital gains. You may want to watch out there if you didn’t account for it. For example, if you bought the property for $1.5 million, made capital improvements of $300k, and then rented it out for 3 years, you would have used (($1.5 million + $300k)/27.5 years)*3 years = $196k of depreciation expenses. This would add another ~$72k to your tax bill, assuming you are in the highest tax bracket (20% LT cap gain + 3.8% Obamacare + 13.3% CA state = 37.1%).

The crushing tax rate is a huge deterrent for me to sell any appreciated assets.

Indeed. But don’t forget, the depreciation expense shields taxes that would have to be paid on rental income.

Yes, the depreciation expense shields taxes during the years you are collecting rent, but eventually you pay them back when you sell the property since your property didn’t actually depreciate, it appreciated…

I have rental properties in the Bay Area as well, so I just read up a little more on the tax issue. It looks like the depreciation recapture is taxed at ordinary income tax rates, which are even higher than long-term capital gains rate (you’re probably in the 39.6% + 13.3% = 52.9% tax level). Makes sense since when the depreciation was expensed, it was saving taxes on income at the ordinary income tax rate. You actually pay more in tax than you retained in tax savings if your ordinary rate now is higher than the years you were expensing.

Financially speaking, the most optimal thing to do would be to pass the property on to heirs, who get a step-up in basis and won’t have to pay any tax. And Trump might eliminate the estate tax (of course it may just be reinstated after the next election – yeesh). This is the big reason why I find it really hard to sell greatly appreciated assets if I don’t foresee ever needing to use that money. In your case, the hassle factor may outweigh the hundreds of thousands paid out in taxes.

Indeed. At the end up the day, everybody has to ask themselves how much is enough. $10 million? $25 million? $100 million? Does having two heirs and 10 properties make sense? For some, yes. For me, no. After a certain point, any more doesn’t change the quality of your life. It actually may start to hurt. Can’t take it with you as the Egyptians said.

The best benefit of financial independence is freedom to do whatever you want, always. I hope people don’t lose sight of this message.

I wonder if the estate tax gets repealed, there will actually be some super wealthy people who will try to die before the next administration… Hmmm. Of course not. If you are super wealthy, your goal is to live as long as possible!

I guess this means you are now officially beyond the “Always be Grinding” stage of your life :-)