There’s a lot of enthusiasm for Roth IRA conversions and Mega Backdoor Roth IRAs—and for good reason. Paying taxes upfront on your retirement accounts can be a savvy move, especially if you’re in a mid-to-lower federal income tax bracket, as it allows for tax-free withdrawals in the future.

That said, thanks to the latest standard deduction amounts and income thresholds for paying no long-term capital gains tax, more Americans now have the opportunity to make larger tax-free withdrawals from their taxable brokerage accounts. For 2025, that tax-free income amount is up to $63,350 for a single person and $126,700 for a married couple. It's slightly higher for 2026.

The vast majority of Americans should be able to live comfortably in retirement on $63,350 or $126,700. After all, the median individual income in our country is about $43,000 before taxes. Therefore, don't neglect building your taxable investments!

This article will show you how to earn and withdraw six figures while paying no taxes. I’ll also provide a guide on how much you should save for retirement if these income levels are sufficient for your needs. As I'm not a tax professional, just an enthusiast for 25 years, feel free to challenge me and share some further insights if you are one.

Related: 2025 Federal Income Tax Rates And The New Ideal Income

A Taxable Brokerage Account Increases In Importance

For those pursuing FIRE, growing your taxable brokerage account is crucial, as it generates the passive income you'll rely on in retirement. Unlike tax-advantaged retirement accounts, there are no contribution limits, and no required minimum distributions. Additionally, you can take tax-free withdrawals, as you'll see below.

If you're planning to retire early, I recommend maxing out your tax-advantaged retirement accounts each year while working to grow your taxable brokerage account to three times the size of your tax-advantaged accounts. Achieving this balance can set you up for financial freedom. Since starting Financial Samurai in 2009, I've encountered many people who neglected their taxable brokerage accounts, which ultimately left them constrained.

Below is a case study showing how much you might aim to accumulate in taxable investments alongside your tax-advantaged accounts. While this may seem like a stretch goal for some, it's my recommended framework for building long-term wealth. At age 50, you likely won't have to pay any income taxes upon withdrawal with $2.4 million in retirement savings.

Related: How 401(k), IRA, And Brokerage Withdrawals Are Taxed: Income Or Capital Gains

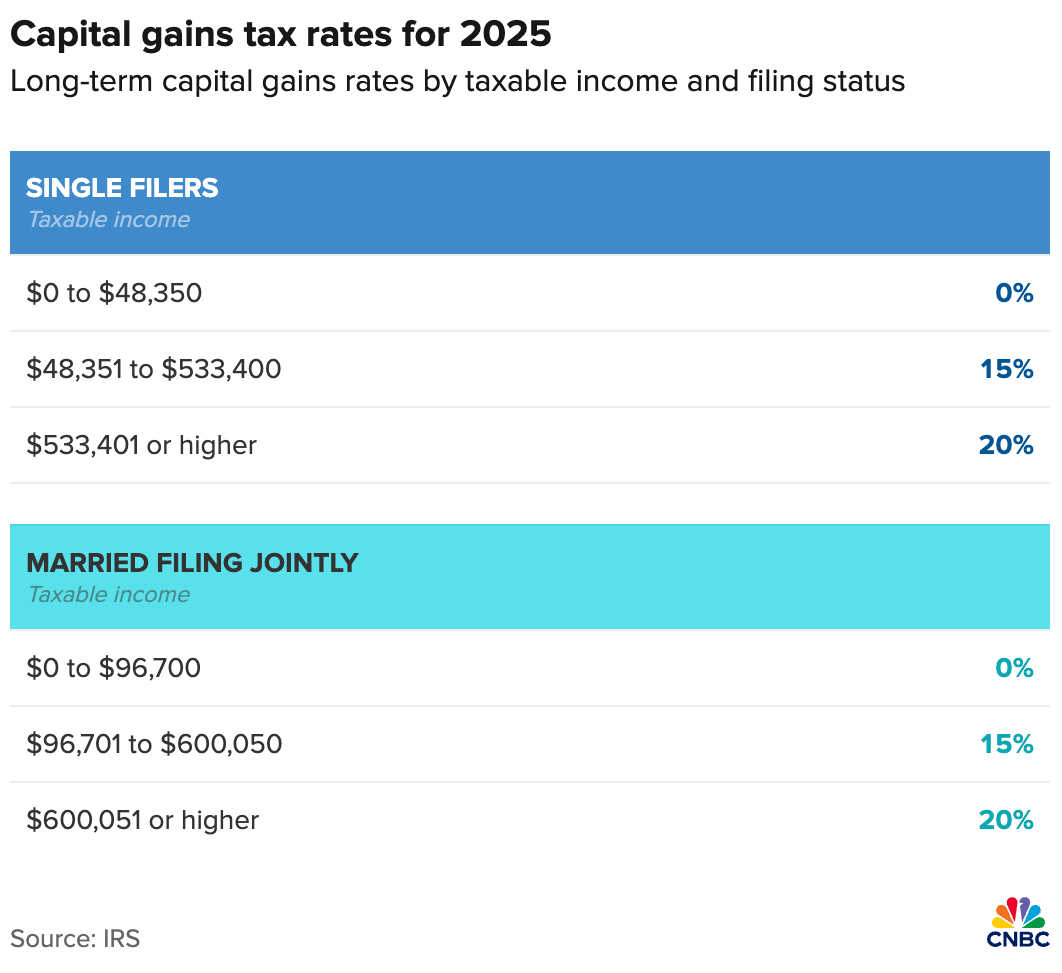

Standard Deduction Limits And Income Thresholds For 0% Tax

To understand how to achieve tax-free withdrawals from taxable brokerage accounts we must first know two key factors:

- The latest standard deduction amounts: $15,000 for singles and $30,000 for married couples for 2025.

- The income threshold for the 0% tax bracket on qualified dividends and long-term capital gains: $48,350 for singles and $96,700 for married couples.

By adding the standard deduction to the income threshold based on your marital status, we can calculate the tax-free income and withdrawal limits. For 2025, these limits are:

- $63,350 for singles

- $126,700 for married couples filing jointly

However, to avoid paying taxes on $63,350 or $126,700, the composition of your income is crucial. Let’s illustrate this with an example for a married couple filing jointly. Always check the latest standard deduction and income threshold amounts, as they change every year.

Meet Chris and Taylor – Semi-Retired And Consulting Part-time

Chris and Taylor are in their early 60s, semi-retired, and living off a mix of passive income from investments and part-time consulting work. They’ve built a $2 million taxable retirement portfolio during their working years and now focus on optimizing their tax situation to live comfortably.

How They Earn Tax-Free Income in 2025

- Standard Deduction

The standard deduction for married couples filing jointly is $30,000 in 2025. This deduction shields the first $30,000 of their income from federal income taxes. - 0% Long-Term Capital Gains Tax Rate

The 0% tax rate on long-term capital gains and qualified dividends applies as long as their taxable income (after deductions) remains below $96,700. - Combining the Two

By combining their standard deduction with the 0% capital gains tax threshold, Chris and Taylor can earn:- $30,000 in ordinary income (e.g., consulting income or IRA withdrawals), $96,700 in long-term capital gains or qualified dividends. This gives them a total tax-free income of $126,700 in 2025.

Chris and Taylor’s Part-Time Consulting

Chris and Taylor earn $30,000 from part-time consulting—a pursuit I highly encourage for semi-retirees or retirees to stay mentally active and engaged with society. This ordinary income is fully offset by their $30,000 standard deduction, meaning they pay 0% federal tax on their consulting income.

After listening to my podcast interview with Bill Bengen, the creator of the 4% Rule, they feel comfortable withdrawing between 4% to 5% annually from their $2 million taxable portfolio. This year, they sell investments, realizing $96,700 in long-term capital gains. Because their taxable income (after accounting for the standard deduction) matches the $96,700 threshold for the 0% federal long-term capital gains tax rate, they owe 0% federal tax on these gains as well.

However, Chris and Taylor reside in California, where all capital gains and dividends are taxed as ordinary income. At their marginal California state income tax rate, they owe $5,365 in state taxes on their combined income of $126,700, resulting in an effective state tax rate of 4.23%. Not bad, but something to consider.

$126,700 Tax-Free Income Is Equivalent To ~$170,000 In Wages

To walk away with $126,700 after taxes, you would need to earn approximately $170,000 in gross income at a 25% effective tax rate (including FICA taxes), assuming no state income taxes. If you live in states like California, New Jersey, or New York, where state taxes significantly impact your take-home pay, you’d likely need to earn closer to $180,000 in gross income to achieve the same after-tax amount.

For Chris and Taylor to avoid paying state income taxes entirely on their $126,700 income, relocating to one of the nine no-income-tax states—such as Texas, Florida, or Tennessee—is one solution. Alternatively, states like Illinois, Pennsylvania, or South Carolina, which tax income more favorably or exclude certain income types, could also provide meaningful tax savings depending on how their income is structured.

This gross income comparison underscores the value of saving and investing for retirement. Diversifying retirement funds through a Roth IRA or Mega Backdoor Roth IRA is another effective strategy, depending how rich you think you'll be.

However, if you anticipate staying below certain net worth thresholds in retirement, the Roth IRA’s benefits may diminish, as you could achieve tax-free withdrawals from taxable brokerage accounts regardless.

$1.5 Million / $3 Million Retirement Portfolio Threshold To Start Worrying About RMDs And Paying More Taxes

One challenge that some wealthy or super frugal retirees face is the requirement to take Required Minimum Distributions (RMDs) starting at age 73, as mandated by the SECURE 2.0 Act. These RMDs, which are treated as ordinary income, can potentially push retirees into a higher tax bracket. It's important to understand that the 401(k) and IRA are considered pots of deferred income. Since you contributed to these retirement plans without paying taxes up front, the government wants to tax you on the withdrawals.

However, if you don't anticipate retiring with more than $3 million in your 401(k) or IRA as a married couple, you’re likely safe from paying significant taxes in retirement. This safety comes from the standard deduction and the increasing income thresholds for 0% tax on long-term capital gains. Unfortunately, up to 85% of your Social Security income will be taxed if Congress doesn't change any laws. Trump has mentioned he wants to eliminate Social Security income taxes as part of his tax cut for middle class workers.

For singles, shoot for a retirement portfolio of up to $1.5 million and feel safe from paying too much in taxes due to RMDs. $1.5 million is just $100,000 shy of how much workers in their 50s said they needed to retire comfortably in a 2023 Northwestern Mutual survey. So perhaps those surveyed have a good sense of their retirement needs after all.

Given the income threshold for 0% capital gains tax is $48,350 (single) or $96,700 (married), we can calculate whether $1.5 million and $3 million are reasonable retirement portfolio target amounts. At a 4% withdrawal rate to get to $48,350 (single) and $96,700 (married), this means a single retiree needs a portfolio of $1,346,250, while a married couple requires $2,417,500 to fully optimize this strategy.

The retirement portfolio threshold amounts can be indexed to inflation over time. The standard deduction amounts should also increase over time, as will the income thresholds for 0% capital gains tax. But for now, $15 million and $3 million are two easy to remember figures if people want to shoot for net worth goals.

RMD Example With Taxes To Pay

Below is a graphical example of a retiree forced to take RMDs at age 73 with a $3 million 401(k). The calculation assumes:

- A withdrawal rate of 3.8%, as determined by the Uniform Lifetime Table calculation.

- No additional contributions are made after retirement.

- An annual investment growth rate of 5%.

If you're 73 now, you'd take your $113,207.55 RMD and subtract the $30,000 standard deduction for married couples if you don't have greater itemized deductions. Your taxable income based on RMDs alone is $83,207.55, putting you in the reasonable 12% federal marginal income tax rate for 2025.

However, with 85% of your combined $36,000 a year in Social Security income being taxable, your total taxable income is $113,807.55. This puts your income between $96,951 to $113,807.55 in the 22% marginal federal income tax rate. Your total federal income tax is about $14,865, which means you have an effective tax rate of 10% of your RMD + Social Security income of $149,207. Not bad!

By the time you turn 73, the married income threshold for the 0% tax rate will likely be higher than the RMD amounts discussed above. Additionally, the standard deduction will likely increase as well.

On the other hand, if you anticipate having retirement portfolios well over $1.5 million / $3 million, you’ll have a greater incentive to take advantage of Roth IRA conversions and Mega Backdoor Roth IRAs earlier in your career. The best time to implement these strategies is when your income is at its lowest, such as after a layoff or during an early retirement phase.

Summary Of Tax-Free Withdrawals From Retirement Accounts

To achieve tax-free withdrawals and income in retirement, retirees should stay within the standard deduction and 0% tax bracket for long-term capital gains and qualified dividends. In 2025, this means keeping taxable income under $68,850 (single) or $126,700 (married), which includes the standard deduction ($15,000 single, $30,000 married) and the tax-free threshold for capital gains/dividends.

Required Minimum Distributions (RMDs) from 401(k)s and IRAs start at age 73 and are taxed as ordinary income. To avoid higher taxes, limit pre-tax account balances to $1.5 million (single) or $3 million (married), and consider Roth conversions earlier in retirement.

Social Security should also be managed to avoid taxes. Up to 85% of benefits can be taxed if combined income exceeds $34,000 (single) or $44,000 (married). By balancing RMDs, dividends, and capital gains, retirees can enjoy tax-free income.

Worst case, if you accumulate more money than expected, you’ll just pay more taxes—not a bad problem to have!

Check Out The Best Financial Planner: Boldin

Withdrawing retirement funds in a tax-efficient way can be daunting, but the Boldin Financial Planner makes it much easier. Built specifically for retirement planning, Boldin offers the best tools to help you navigate this critical stage.

One standout feature is their Roth Conversion tool, which helps you determine how much to convert to potentially save the most on taxes. A snapshot of the tool is below.

If you’re serious about building wealth and retiring comfortably, sign up for Boldin’s powerful financial tools. They offer a free version and a PlannerPlus version for just $120/year—far more affordable than hiring a financial advisor.

Retire Early With a Severance Package

If you’re planning to retire early, consider negotiating a severance package instead of simply quitting. You have nothing to lose. A severance package provides a crucial financial cushion to help you on your next journey. My wife and I both negotiated severance deals in 2012 and 2015, which gave us the courage to leave work behind.

I’ve detailed all my strategies in my book, How to Engineer Your Layoff. The book is now in its 6th edition. Use the code “saveten” at checkout to save $10.

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Your shares, ratings, and reviews are appreciated.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009. Everything is written based on firsthand experience and expertise because money is too important to be left up to the inexperienced.

In the section tht strts this article, How they earn tax free income in 2025, another bolt on to that (that would be helpful to me, is adding in social security. I will be in that boat, making bout 75k in l/t capital gains and qulified dividends (1099 DIV), pulling about 30k from 401k and have 65k in SS between my wife and I, both at 65 yers old. That would be it for us in terms of income. Most of the articles I red don’t address all three of these income types. It looks like I would be close to $7k in taxes.

I am forced to take out $45k each year from my deceased husband’s 401k and is considered ordinary income. That $ along with my pension ($19k) and widow social security (33k) my taxable income is close to $100k. I have about $1.8M in 401k money (mine and my deceased husband’s) and I want to give my children some $ now for various reasons. I am 63 years old and currently in the $24%. If I take $ out is it considered capital gains, and how much can I take out before jumping to the next tax bracket? What’s the difference between capital gains vs. ordinary income?

Can you indulge and run through another scenario for me? The pre-RMD years are probably most important for me to get this right as well as establishing a good strategy from the jump. Not real numbers, but let’s use this scenario:

I’m single, retiring at age 60, my first year of no income from any jobs.

1.5 million in 401(k), let’s say 1 million in pre-tax, $500,000 in Roth 401(k).

1.5 million in a brokerage account

No other investments, or income, and I’m not taking social security.

Let’s say I want to have $60,000 of tax-free income from those 2 accounts above in each of my first 5 years of retirement.

What’s the play?

To clarify somewhat, I have no heirs/kids, am single and will be debt-free in retirement. My biggest retirement expenses will be a ridiculous annual real estate tax bill and any medical expenses that come around as years go by – given my situation I am considering long term care insurance as one of those things.

That said I do not anticipate needing a six-figure income post-retirement at 60 as I do not have expensive hobbies or large travel aspirations.

I am confused by the RMD example for $3 million. RMDs are ordinary income, capital gain tax thresholds are irrelevant. Only the standard deduction applies, and as you mention social security income will use that up. So at age 73 you have $113,207 of fully taxable ordinary income, not $0. What am I not understanding? Thank!

You are not missing anything. You are astute and I need to clarify! So let me do so here.

If you’re 73 now, you’d take your $113,207.55 RMD and subtract the $30,000 standard deduction for married couples if you don’t have greater itemized deductions. Your taxable income based on RMDs alone is $83,207.55, putting you in the reasonable 12% federal marginal income tax rate for 2025.

However, with 85% of your combined $36,000 a year in Social Security income being taxable, your total taxable income is $113,807.55. This puts your income between $96,951 to $113,807.55 in the 22% marginal federal income tax rate. Your total federal income tax is about $14,865, which means you have an effective tax rate of 10% of your RMD + Social Security income of $149,207. Not bad!

And if you’re a ways away from 73, the standard deduction amounts and income threshold amounts should increase. And maybe, Congress might eliminate Social Security income tax altogether based on the latest proposed middle class tax cuts.

Hey Sam,

Just wanted to thank you for writing this article. Before reading this, I was focused on 401k, 401k Roth and my personal Roth IRA as my main income streams when I retire in 8 years at age 60. I had been doing very little investing other than maxxing these things out and keeping emergency cash aside.

I recently lost my last parent and as a result will be inheriting some money, which after I pay the necessary estate taxes, will still be enough to get me started on building up my brokerage account which has been a low priority and currently sits at just 50k. Before I read this article, I was going to keep most of this in HYSA cash, but I’m realizing now that investing some of this in an S&P or similar fund with my brokerage now, post-retirement, I can withdraw a significant amount of this tax-free without even needing to start touching my 401k and Roth right at 60.

Appreciate the education.

No problem, eight years away is quite close. I would stay relatively conservative with your investments. Here is an article I wrote on how I’d invest $250,000 today.

If you have to pay some state taxes, does that mean your parents estate was larger than $13.99 million per person?

Thanks for the response and approval. I did see that post yesterday and will be taking a look. It’s not a relatively life changing amount probably around 600,000 even after I sell the house but I will be debt-free in retirement so it’s money I can invest now.

I live in Pennsylvania where siblings are taxed 4.5 percent of every dollar on an inheritance. My father was not financially savvy enough to set up trusts or other ways to avoid this so I’m having to send our state 4.5 of everything when I’m done with asset gathering. It’s criminal.

Sam, this article, among many of your others, is very helpful to me and perfectly timed since I retired last year and now I’m in decumulation mode with the accompanying need to be tax smart!

You are very helpful, knowledgeable and accurate. I want to thank you sincerely for that.

You’re welcome Eric! I face these similar challenges as well, so I figure I might as well try to understand an share solutions with anybody who cares to read. If you’d like to support my work, you can always subscribe to my free newsletter, share my work, and rate my podcast.

Thanks!

Done! My tax rate fell off a cliff for 2024, plus I didn’t stop work until 55 since it’s hard to walk at peak income. Walking last year required more discipline than anything I’ve done, other than parenting. So we share the good problem of having to optimize withdrawal strategy! Happy holidays to you and the fam.

Great article. We reached FI in our mid 40s and I cut back to part time. Spouse stays at home. 2 kids at home. We’re fortunate that we live in the Midwest, and only need about $120k pretax to live a comfortable life. You’re right, we pay very little taxes. Most don’t realize how little taxes you pay, once you cut back to part-time and your income drops.

But if you live in a high cost area, $120k may not be enough for a comfortable life. One thought is one could move to a lower cost area, once they’re reached FI.

Yes. Wish I had focused on more contributions to Roth IRAs. No one really explained RMDs to me in my 40-65 years ;(

Other than my SSA my retirement is in regular IRA. Not only Fed/state tax considerations it can significantly up one’s Medicare B/D premiums. We took a hit one year from a large capital gains on selling a rental. Our Medicare premiums for BOTH of us went from 179 to $529 something. Also Roth IRAs give your kids better treatment upon their inheritance.

BTW consider the benefits of a self directed IRA for your real estate investments for tax purposes.

Investing in Publicly Traded Partnerships (PTP) in taxable accounts can be used to generate tax-free income/distribution, based on the K-1’s, can distribute/return principle (tax free) while applying costs/losses against other income streams. Many of these PTP’s have gained in value and once held for 1+ years the LTCG tax is applied upon their sale.

examples, ARLP, ET, MPLX, EPD, WES, BSM

Sam

You are spot on! I am about 10 years ahead of you full on implementing my financial plan during retirement. Just like I needed to have a diverse investment portfolio within that plan I also needed to have a diversity of types of money (Roth, IRA, Brokerage, potential Annuity, social security and Whole life cash value). If all money is tied up in qualified money once you hit RMD age which is 75 you pretty much have zero flexibility. Actually I found trying to do Roth conversions by pulling money out of the IRA to pay taxes does not help..you need passive tax advantaged income from a brokerage account to offset the AGI increase to maintain the targeted tax bracket. It could mean several hundred thousand dollars to net worth and estate as well as impacting retirement income. Diversity in income streams with regards to estate planning is also critical. In my opinion ROTH IRAS are a must in the plan…the advantages at this stage of my financial plan implementation are so overwhelming I had to talk to my advisor several times… could not believe the benefits..What I found that is extremely important is at age 60 I needed to start implementing the plan so over the next 15 years at RMD time I am tax efficient for that day. C

If some of my mutual funds generate capital gains in my taxable account won’t that lower the amount that I can withdraw to remain tax free

I’m confused. Aren’t they capital gains generated by your mutual funds included in your taxable income in addition to those generated by selling assets

What about internal capital gains generated by your investment accounts.from your mutual funds etc Won’t those be included in your yearly capital gains that you have to pay taxes on in addition to the withdrawal from your taxable account

The capital gains tax rate approach you’re discussing is even better than you let on. Your example assumes that all withdrawals from a taxable account are done with a $0 cost basis. In reality, much of any given withdrawal will not be capital gains, but rather the gains will be reduced by the original basis. So even more “income” can be realized – it’s really the gains portion that counts as income for tax purposes.

I thought that was a key distinction as well. You aren’t simply living off your capital gains but rather your capital gains and return of principal which would not be part of the tax consideration.

Sam, my wife and I retired early and are still in our mid-50s. I am considering converting some of our Traditional IRA into Roth IRA. However, while I will benefit from tax free withdrawals down the road, I am faced with paying taxes today. While my income is currently very low, approximately $44,000 per year, and the tax rate is correspondingly low, this will greatly impact the health care subsidy I receive. My wife are on I are on the ACA for health care and get around $2000 per month subsidy. Because of the subsidy, the Roth conversion seems wrong. Thoughts?

Hi Robert,

Great question I have not encountered before because I have never been able to receive the subsidy. But if your conversions make you make too much to get the subsidy, then I definitely wouldnt do it.

The missing variable is how big of a retirement portfolio you have. If it’s less than $2.5 million per the both of you, Roth IRA conversions won’t matter for saving you money (I wrote $3 million in my post).

Sam

I’m struggling with the concept of maxing out the retirement accounts but aiming for 3x the amount in taxable accounts. My wife and I max out our 401k accounts (self employed, so no match) which is $60K. Then we max out our HSA which is $8-9K. This leaves us with about $30K to put into taxed accounts.

Right now we have about 7X as much in retirement accounts versus taxable accounts.

We are constantly feeling retirement rich and cash poor, but not sure at what point it’s worth it to reduce retirement contributions and increase taxable contributions.

Any insight here?

If you’re OK working until 60 or not withdrawing until 60, I wouldn’t change anything.

But if you’re not, then focus more on the taxable accounts.

Gret information Sam. I retired two years ago and am sitting on significant unrealized capital gains, in my taxable account. I thought I would be eating a lot of taxes for capital gains, even at 15%. I am glad to know I can cash out some of these investments, without getting killed by taxes.

I’m glad you can too! The question may become: when will you sell? It’s been such a good run that it’s hard to sell and let go.

This idea of decumulating after spending a lifetime of accumulating is hard! If you have any thoughts on the subject and have to reconcile this problem, I’d love to hear it.

What I have done in the past is to sell in January, after the end of the year run-up. Then, I pick some new investments that look fairly valued. When I worked, I had a capital gain, but I wouldn’t have to pay the taxes until the following year. It has been working great so far, but I feel like we are overdue for a correction.

As for decumulating, I’m just not doing it. My plan is to average around 10% in the market and spend 5% at a safe withdrawal rate. This should provide for inflation, if I live to a ripe old age. The market has been way up, so I have been spending 6%. When the market dumps, I will live on 4% and I have a year of money market, so I don’t have to sell positions at the bottom. You have been at it for a long time, so just let me know if you see any holes in my plan. Bret

Sounds like a good plan to me. The amount of investment gains recently have been way beyond what most have modeled for retirement planning. Hence, being able to spend a little more and enjoy the good life is certainly fine!

My greatest difficulty is actually doing the spending. I’m still wearing socks with holes in them right now! lol.

Tell me about it! I’m still wearing a fleece vest from high school and my jeans are circa 2008. But since everything is cyclical, I’m back in style again!

This is going to sound really dumb but I have never heard of a 0% long term capital gains bracket. I thought that I was going to have to pay 20% after I sold a rental house I’ve own for over 5 years. So you’re saying I could just sell a rental and not pay any capital gains taxes on the equity as long as I stay below a certain income?

Yes.

If you sell your rental property and your total taxable income for the year remains under these thresholds, you could potentially pay 0% capital gains tax on the profit from the sale.

However, a few important caveats:

1. This is your total taxable income, not just your income from work

2. The gain from the property sale will be added to your other income

3. State taxes might still apply

4. You’ll want to carefully calculate your total taxable income for the year

Ask your tax person.

would rather retire with IRMAA and net investment income tax than ACA subsidy and zero long term capital gain/qualified dividend tax rate

It looks like if I stop putting money into my 401k and wait 30 years to start taking out withdrawals at age 73 when RMDs kick in, I’ll end up with well over $3 million, assuming a 6% return. So, should I just stop contributing to my 401k and focus on building my taxable account instead, so I can retire earlier? I’m in a high-income bracket, and honestly, I’ve never really thought much about maxing out my 401k. I’ve just always figured it’s something everyone should do.

I would continue to max out the 401(k) and do your best to build a taxable brokerage account equal to 3 times your 401(k) balance.

You’ll have to pay taxes in retirement, but that’s a good thing too.

Anon,

1) You absolutely should continue 401k contributions up to any company match as that is free money.

2) Next, take advantage of HSA contributions if available, as that is the only tax plan that provides the triple advantage of tax deductibility, tax-free growth, and tax-free withdrawals.

3) Whether you should contribute to tax-deferred 401ks above the match depends upon your personal situation and marginal tax-rate. If your marginal tax rate is low (24% or especially if less), you probably want to Roth any additional savings whether through your company 401k plan (via backdoor conversion if over income limits) or your individual account up to the $7k limit. If your marginal tax rate is high (32% or possibly at 24%), then definitely continue to max out your 401k contributions.

We can never know where tax rates are heading, but you probably want your retirement savings to be spread out among all three tax buckets: after tax (where you can take advantage of low capital gains rates per Sam’s post), tax-deferred (401k and 403b where you get a match and current year tax-deduction), and forever tax free (Roth and HSA).

Keep in mind that Roth’s and HSA’s provide two other long-term advantages – no mandated RMD’s where the government controls your annual withdrawals and resulatant taxes, and tax-free inheritance.

I no longer believe that workers want to blindly max out 401k tax-deferred contributions over a long upwardly-mobile career as you can end up with tax-deferred accounts being far too over-weighted. When my wife and I retired, 90% of our wealth was in tax deferred accounts and now we are madly Roth converting to get more balance. A better game plan today is to Roth and HSA when younger and in our lowest marginal tax-rate working years.

“ When my wife and I retired, 90% of our wealth was in tax deferred accounts and now we are madly Roth converting to get more balance”

Thanks for sharing your thoughts. I see this frequently. What was the reason for not building your taxable brokerage account? Doing so is the main action take away from this post.

Thx

Sam

We burned through our taxable savings to buy a rental cottage near our two kids, fund early-year retirement living expenses to postpone both social security claiming and tax-deferred account (IRA\401k) withdrawals, and pay the huge tax bills to Roth convert every year.

We now operate essentially cash-broke within taxable accounts except for retaining a handful of 30-year capital gain stocks. We had originally planned to retain these stocks until death so that our kids can capture the tax-free step up basis. Now, the better tax and estate playbook may be to use these capital gains to pay taxes for even more Roth conversions to reduce RMDs. We had never planned on stocks increasing 250% over the last 8 years within our tax-deferred accounts.

Sam, unless all the big expenses, like mortgage, health care, cars, kids weddings, etc, etc, are payed off, then maybe one can live at your suggested income, otherwise no. Our RMDs will be high enough to negate your $$ amounts

Congrats!

Umm no, it defeats the no paying taxes bit.

What’s your solution? You still get the standard deduction if you choose.

1) people aim to pay your mortgage off before retirement or shortly thereafter

2) You should be setting aside the equiv of car payment for a new car in a taxable account each month and things like a car payment so you don’t need larger withdraws once every 8-10 years. Given the tax basis is tax free on sale and rest is 0 to 15% in this scenario, shouldn’t be that hard

3) Weddings don’t go too crazy on – my boss spent close to $1m on daughter’s wedding and the marriage didn’t last a year. I sometimes think there is an inverse relationship between spent on wedding and how long the marriage lasts.

Hi Sam

quick question, how rental income are treated in this calculation? As income? Would it be clever to sell rental to buy index fund in taxable account before retirement in order to avoid to use all the standard deduction ?

Rental income is treated as ordinary income. But you have expenses and amortization you can use to shield it.

Some thoughts on When To Sell Rental Property

Thanks Sam,

another question at this point….can we consider in your formula the equity in the rental real estate as part of the taxable account before retirement? I.e Taxable account (stocks/funds/real estate equity) = 3X Retirement account ?

Yes

Thank you for highlighting this and reminding me about the RMDs. I have been filing my mother’s taxes for over ten years now. And I remember when she first hit age 73, the tax software started asking me questions about her RMDs. She had sadly long depleted her IRA by then, so she had no RMDs to take. But as a result, I pushed RMDs out of my mind and totally forgot about they will (most likely) impact my own retirement. So thanks for this very important reminder/wake up call. I should be fine, but I do like to feel ahead of the ball when it comes to bills and taxes due. So I’ll put some thought and calculations into my anticipated tax situation when I reach 73. thanks!

Sam,

I know you are a fan of crowdfunded real estate, but have you ever done evaluations on crowdfunded farming funds like FarmTogether?

Hi Sam,

I have a question, would this strategy work with a 457(b) account? I am a firefighter and I have a generous pension, a 457 and other investments in CDs, and taxable brokerage accounts. I am currently investing > $20k a year in the 457 account. I do not currently have any Roth accounts.

Let’s say hypothetically my pension will pay $75k a year and it has a built in COLA. Could I withdrawal $51,700 from my 457 tax free ($126,700 – $75,000 = $51,700)? I would be filing married jointly and I live in an income tax free state.

I do realize I would pay taxes on $45,000 of the pension earnings.

Thank you for your years of financial education,

CJ

You don’t say your age but a big advantage of your 457 account is that there is no penalty for taking the money out before you turn 59.5.

Hi CJ,

Thank you for your question and for your service as a firefighter! It’s great to see you taking proactive steps toward optimizing your retirement.

To answer your question: $30,000 of the $75,000 pension income would be shielded by the married standard deduction, so you’d pay tax on the $45,000 of the pension earnings.

Then you could withdraw $51,700 in profits from your 457(b). But the withdrawals are considered ordinary income.

The 0% capital gains tax threshold applies only to qualified capital gains and dividends, not to ordinary income.

Given your generous pension and the lack of a Roth account, you might consider rolling some of your 457(b) funds into a Roth IRA through partial Roth conversions in lower-income years or before your pension kicks in. Doing so would allow future growth and withdrawals to be tax-free, complementing your taxable and pension income.

Living in a no-income-tax state is a significant advantage—every dollar you save in federal taxes will go further!

Thanks again for reading,

Sam

Hi Sam – great article. Wouldn’t the 457 withdraw be taxed as ordinary income (the account appears to be pretax, not Roth). Not sure what you mean by “withdrawing profits”?

You are right! Thank you. So doing some Roth IRA conversions now will help diversify tax liability in retirement.

I put together this follow up post on How 401(k), IRA, and Brokerage Withdrawals Are Taxed with some examples to help clarify. Taxes are so complicated, it’s good to review them often.

As a local government employee with a pension, I had the same question. Thanks for answering!