The main reason I can't convince anyone in real life to FIRE is the desire for more. The moment you hit a $1 million net worth, you start dreaming of $5 million. Get to $5 million and suddenly $10 million sounds reasonable. Hit $10 million and, well, why not shoot for $25 million and higher? The goalposts never stop moving on their own. You have to make them stop.

That's easier said than done when you went to college with sharp, type-A people who went on to have highly successful careers. And if you then live in a city filled with those same people, drawn from every corner of the world, walking away from a soul-sucking job becomes that much harder.

Since 1999, I've only lived in New York City and San Francisco, arguably two cities with the most gung-ho people in America. But I FIREd in 2012 because I was unhappy after 13 years and in chronic physical pain. I took one look at my bosses' lifestyles, decided it wasn't worth it, negotiated a severance, and quit the money.

A Nice Home Is The #1 Asset Go-Getters In Type-A Cities Want

One of the things people get wrong about San Francisco is assuming it's unaffordable. The reality is that it's incredibly affordable if you have the income and growing assets to pay for it.

Rents and property prices are high precisely because there are thousands of people earning high salaries and building substantial wealth through their investments. If there weren't, the prices would fall. Economics 101.

This isn't Canada, where wages are lower but property prices in Vancouver and Toronto are similarly sky-high due to government policies. This is America, where capitalism does the pricing and corruption is more aggressively rooted out.

Once the big money starts coming in, the temptation to buy a nicer home is completely rational.

We spend most of our time there. Add kids to the equation and a home stops being just real estate. It becomes the center of your whole life. And frankly, it's fun to enjoy your wealth in a way that might also make you more of it.

My Constant Desire For Owning A Nicer Home

I've felt the pull of those big San Francisco home prices myself.

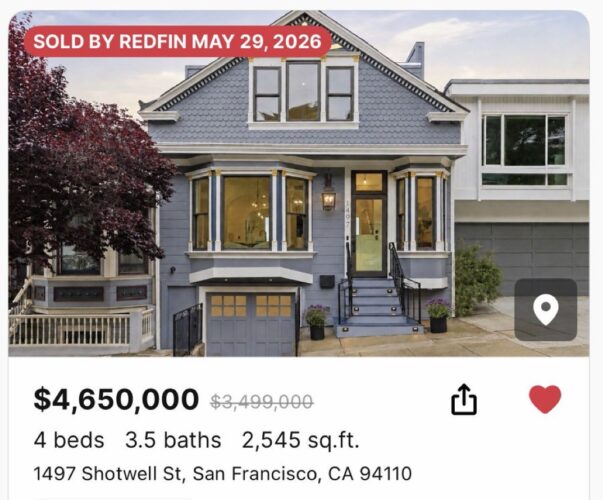

In 2018, not having a large W-2 paycheck prevented me from getting a mortgage on a highly desirable 4/3.5, single-family home. If only I were earning $1 million a year, I could have snapped up that big beautiful home for $4.5 million!

My son had been born the year before, and we had just finished an exhausting 1.5-year remodel of our fixer-upper in 2016. It was a wonderful 3-bedroom plus office, 2-bathroom home overlooking the Pacific Ocean just under 2,000 square feet. But once the dust settled, I started wanting more. Classic.

Here were my calculations on what it would cost to afford a 60% larger house in a more expensive neighborhood.

Ultimately, we passed on upsizing so we could comfortably remain dual unemployed parents and care for our newborn full-time. We didn't want to feel trapped being house rich cash poor as first-time parents. Instead, we wanted options just in case we wanted to move or our financial situation turned for the worse.

It was hard to be satisfied with what I had, partly due to my love of real estate, and partly due to ego. Did I really want to just own a median-priced home in San Francisco, and not something nicer based on my net worth?

But keeping our living expenses down helped us feel a lot more at ease, especially when COVID hit. We also got to invest more in the stock market, which continued to go up. FIRE was more important to us at that stage in our lives.

Buying A $15 Million Home Makes FIRE Much Harder

Recently, there was a lot of buzz about a home in Cow Hollow, San Francisco that listed at $7.95 million and sold for $15 million. It's a fantastic 6-bed, 6-bath, 5,725-square-foot home with a coveted enclosed front yard and sweeping bay views. Hard to beat. The oversized 4,744-square-foot lot gave it an even more grand feeling.

But here's the thing: the new buyer will likely need to sink another $1 to $5 million into the home to update it. And that's assuming no major structural surprises. At 5,725 square feet, a complete gut remodel could run $7 to $10 million. I don't think a gut remodel is necessary, but still.

Based on my guideline that your primary residence should represent no more than 50% of your net worth post-purchase (ideally 30% or less), you'd need a net worth of at least $30 million to responsibly buy a $15 million home and cover remodeling costs. But ideally, your net worth is closer to $50 million.

But big home purchases make the option to FIRE genuinely harder. A massive equity windfall and fat salary are wonderful, but they don't last forever. Equity can evaporate, especially if you are at a startup. And if you buy a fixer, the time, money, and sheer mental toll of a remodel can quietly wreck your family dynamics.

Take the numbers in my chart above for a $4.5 million home and triple them. That's what you're signing up for if you buy a $15 million house.

So in the spirit of FIRE and financial freedom, here's a different way to think about it.

FIRE With An $8.1 Million Home Instead

Over the past ten years, I've stayed in homes worth anywhere from $400,000 to $20 million.

The $400,000 option was my parents' two-bedroom in-law unit, which I spent six weeks fixing up. Cozy for four people, but it worked for two months. It would not work for a year.

The $20 million home? Paradise on Earth. Pool, jacuzzi, tennis court, basketball court. The only downside: if an axe murderer scaled the multiple security gates up the hill, no one would hear you scream. The neighbors were a mile away.

Every home has its trade-offs. My current residence falls somewhere between those two extremes, after twenty years of climbing the property ladder. I've climbed as far as I want to go after finding a home with a big lot and views.

So rather than dropping $15 million plus $1 to $5 million in renovations, for a grand total of $16 to $20 million, consider an alternative.

The Cheaper Option

Here's an example of a fully remodeled, move-in-ready 4-bedroom, 3.5-bathroom, 3,610-square-foot single-family home in Cole Valley/Parnassus Heights for $8,100,000. I play tennis on the Graton courts a couple blocks away sometimes when the courts in Forest Hill are full.

It's a great neighborhood, and it'll get a major boost after 2030 when the $4 billion UCSF expansion brings 1,200-plus jobs to the area. Always look out for local economic catalysts before buying property.

Yes, it's about 2,000 square feet smaller than the Cow Hollow home. But a family of four can absolutely live well here. Everyone gets a bedroom. Or the parents can share a room and use the spare as an office, at least two bedrooms have en suite bathrooms, and there's additional family room space on the lower level.

Saving $10 Million With No Remodeling Is Huge

The $8.1 million Cole Valley home is in a great neighborhood. It's not perched as high a hill with sweeping bay views, but you know what? You'll survive. The tradeoff is less foot traffic, less crime (crime doesn't climb), and about $10 million in savings.

At a 4% to 5% safe withdrawal rate, $10 million in invested assets generates $400,000 to $500,000 per year in income. I have done thorough budgeting for households at every level up to $1 million, and I can tell you with confidence: $500,000 a year for a family of four, with no job required, is a genuinely great life.

You take the kids to school in the morning, then play tennis at your private club for 90 minutes. Brunch with your doubles partners. Come home, shower, nap. Read, write, think. Pick the kids up in the afternoon. On volunteer days, you spend hours at school with your children, with zero pressure to be anywhere else.

Not a bad FIRE life!

Buying Already Remodeled Homes Save Marriages

As a bonus, a fully remodeled home that's already been lived in for a couple of years means the bugs have mostly been worked out.

When you buy a $15 million fixer and pour millions into it, you still have to survive a few winter storms before you know if everything actually holds. It usually doesn't. Something always needs fixing.

I cannot count how many couples I know who've nearly divorced or actually divorced over a remodel. It tests everything. Personally, I will never do another gut remodel again. I'll always buy move-in-ready homes from here on out. The premium is worth every penny.

A $3.9 Million Home Makes FIRE Even Easier

If bidding $8.1 million on a $6.5 million asking price is outside your budget, there's another option. A beautiful 4-bedroom, 3.5-bathroom, 2,826-square-foot home in Forest Hill sold for $3,908,000 after listing at $3,295,000.

Forest Hill is quiet, cozy, beautiful, and safe. It is a hidden gem. You can easily walk to the more lively West Portal neighborhood 5-10 minutes away and catch the Muni train from either station if you ever need to commute.

At about half the price of the Cole Valley home, you save $4.2 million. At a 4% to 5% withdrawal rate, that's $168,000 to $220,000 per year in gross income. If you're a couple without kids, that's enough to FIRE right now.

If your lifestyle in San Francisco requires $300,000 to $500,000 per year, you'd need an additional $3.2+ million in investable assets to get there. Doable if you've got a dual income household working in tech, finance, consulting, or medicine.

$3 – $3.3 Million Option For A Great Life

If $3,908,000 is too rich, here's a nicely remodeled 4-bedroom, 4-bathroom, 2,835 sqft home in West Portal listed at $2,995,000. I'm guessing it sells for $3.1-$3.3 million, saving you $600,000-$800,000 compared to the Forest Hill home.

Walkability is highly desirable, until you realize it works both ways. The easier it is for you to walk everywhere, the easier it is for everyone else to walk past your front door, bringing more noise, disturbances, and crime.

And if you plan to FIRE, partly thanks to owning a less expensive home, then you don't need to live near a subway stop to grind at work to pay your mortgage anymore.

There Are Plenty Of Great Housing Options To Choose From

You don't need tens of millions of dollars to FIRE and live well in San Francisco. If you can control your desire for more, you can FIRE with far less.

You'll still be able to breathe the same air, send your kids to the same schools, play on the same courts, and eat at the same restaurants with those with more wealth. The sun will shine on you whether you are rich or poor!

To anyone grinding away in San Francisco, New York, or any expensive city, believing you need to accumulate $10 to $20 million before you can stop: you probably don't. I left work in 2012 with roughly a $3 million net worth and $2 million in investments. We survived just fine as our investments outpaced our expenses.

An $8.1 million home is more than enough for a family of four. So is a $4 million home. And as someone who raised a baby for years in a home worth under $2 million, I can tell you, that was enough too.

Stop letting the perfect home become the enemy of financial freedom. If FIRE is the goal, follow my income and net worth guide for buying a home at various price points. Hit both ideal numbers before purchase, and you'll likely never have to worry about money again.

Readers, how much do you think the desire for more house, more everything, impedes people from actually pulling the trigger on FIRE? If you're sending your kids to the same schools, enjoying the same parks, and soaking up the same San Francisco sunshine as the folks in the $15 million mansion up the hill, what exactly are you still working for? And do you know anyone who's gotten into real financial trouble by buying too much home?

Invest In Real Estate Without The Headaches

If you want real estate exposure without the remodeling nightmares or debt I described above, check out Fundrise, my favorite private real estate platform. Fundrise focuses on high-quality residential and industrial properties in the Sunbelt, where valuations are lower and yields tend to be higher.

Fundrise manages around $3 billion in assets for over 350,000 investors. I've personally invested $500,000+ in their products, and my investment outlook is well aligned with their CEO's. I also appreciate the transparency and low barrier to entry they provide.

Fundrise is a long-time sponsor of Financial Samurai, and Financial Samurai is a multi six-figure investor in Fundrise funds.

Buying A Multi-Million Dollar Home Will Make It Tougher To FIRE is a Financial Samurai original post. All rights reserved. Everything is written based on firsthand experience and expertise, because money is too important to be left to pontification. To build more wealth, join 60,000+ others and subscribe to my free weekly newsletter.

The math here is hard to argue with — a $10 million difference in home price at a 4–5% withdrawal rate isn’t just a housing decision, it’s a decade of your working life. The 30% of net worth guardrail is the single most practical rule I’ve seen for keeping a FIRE timeline intact.

And the point about buying move-in-ready over a fixer deserves more attention than it gets. The premium is almost always worth it once you factor in time, stress, and the near-certainty of a remodel running longer than planned.

Hi Sam, I disagree with the desire for more. The “A folks” in cities are kidding themselves. People with real skills continue working to use skills to contribute to society. More money is shallow end of the pool do not dive in. Also many of the fire folks are not great examples of a life lived well. Too much talk of money & more stuff becomes boring. My Wife was a OBGYN & Lyme expert in town on Eastern Shore of Maryland. She did great work for all patients. She would often say I studied 27 years to help all Humans not make money. We would be out in the community and patients would hug her and say your wife is wonderful. I was a Chemist and in charge of making money. My job of 35 years was to keep the lights on in DC, MD, DE and Southern NJ, manage hazardous waste properly and be a team player with thousands of employees. We both graduated from universities with many degrees, the cost free.

Hi letro, may I ask why you left? Why not keep contributing to society until the very end?

We definitely need more doctors, and I hope your wife is still practicing. Thanks

HI Sam, We retired at 59 and 62 in 2015. You have to examine your ability to work in demanding professions and leave at top performance. Pride comes before the fall. We both were on call for 35 years.

Currently in Waikoloa Beach for six months to enjoy SCUBA, farmers markets and the SMILE life. Our 2026 visit is 35% less than 2025 by doing deals with owners. I wish you and your family an excellent Summer.

We had friends over recently and we were outside enjoying the lovely garden of our co-op apartment building while our kids played. The friend turns to me and says “so when are you going to buy a house?” (Houses in our HCOL area start at $1.5M; the apartment cost us $500k.) I didn’t want to be a jerk so I just laughed off the question but the real answer was “never, and that’s why I am about to retire at 38, while you have decades of financial industry grinding ahead of you!”

Ah hah! Nice job keeping the housing expense lower. I have to be more mindful when I ask such questions to others. I don’t wanna come across as pushy or arrogant.

Maybe a better way is to ask, what do you think about buying a single-family home instead of when are you going to buy a house?

Sam,

We have lived in different real estate worlds in the same country…. We are working to get our home ready to sell in one relatively low value real estate market (hoping to get $600-$650K for a 4500 sq ft home including finished basement on 0.23 acres) to another relatively low value real estate market ($550k new semi-custom home build of 3200 sq ft with a 0.25 acre lot)… but our home value in either case is less than 8% of net worth….

Thanks for all you do.

This was such an interesting perspective on FIRE and lifestyle inflation. A lot of people focus only on reaching a financial independence number, but this article does a great job explaining how major life decisions especially buying a dream home can completely change long-term financial goals. I also appreciated how honestly the emotional side of money and real estate was discussed instead of pretending every financial decision is purely logical.

One thing I really liked is how relatable the article feels. Many readers probably experience the same struggle between wanting financial freedom and wanting a better lifestyle for their family. That balance is rarely talked about this openly. Thanks for sharing such a thoughtful and realistic post on Financial Samurai. It’s definitely one of the more insightful FIRE discussions I’ve read recently.

No problem and thanks for reading. Since 2009, I’ve tried my best to share the ups and downs of FIRE, and how real life gets in the way of logical financial decisions.

You can sign up for my free weekly newsletter here as well. My main goal is to keep people informed so they can achieve financial freedom sooner, rather than later.

Hey Sam, do you have an opinion of condos? I would like a view but I don’t have kids so anything more than 3 bedrooms seems like a waste; the houses in Sea Cliff are too large. Some of the condos in the East Cut have nice views, but HOA fees annoy me, and it seems condos don’t hold their value. I suppose this isn’t a huge deal if I end up staying for a while, but buying a depreciating $5M+ asset seems frivolous.

With an ultra high net worth and no kids, you might as well YOLO more on yourself. Do you have a spouse?

Condo prices are also picking up again, at least here in SF. I’m happy with paying the HOA fee for mine bc they do all the maintenance work I don’t want to do.

Thanks for the info on SF real estate. It makes me feel much better about our custom home we’re building in Houston: 4559 square feet on a 9318 square foot lot. All-in cost $2M. It will represent 66% of net worth on move in day, so we’ve got some work to do. But we have 3 boys ages 7, 5, and 2, so I’m taking your other advice of having the nicest place possible while you have young children.

Enjoy! Let me know about any financial pressure you feel spending 66% of your net worth post build on a primary. What was your percentage before?

So long as you keep earning, saving, and growing your net worth, the house is going to feel more and more affordable over time. How long more do you plan to work?

I think your boys will love the extra space!

I’d like to be work optional by 60 but don’t know that I’d ever fully retire. Our current townhome is 18% of our net worth.

To be able to work at something where you have the energy to work until 60 is a blessing. How many years out is that? And what percentage of your net worth will be your new home post purchase?

I couldn’t take finance after 40, but ultimately left at 34 b/c I could get a severance package that paid for 5 years of my living expenses.

Long time reader, first time commenter!

I’d like to give a different perspective on the subject as I’m the complete opposite of what you’ve described.

My wife and I left the workforce in 2020 in my mid thirties and have zero regrets. We had a net worth around 2mm net worth and left a big city to move to a ski town. We downsized from a 4k sq ft home to a new build 1500 ft sq ft home with no maintenance and shared yard. We spend our days skiing, trail running, mtn biking and traveling

for months out of the year. We’re in the best shape of our lives and have never been happier. We left a ton of money on the table exiting the rat race so young, but I’m more confident than ever this was the right decision.

I absolutely recognize I’m the odd man out, even compared to all my closest friends.

Enjoy. Your lifestyle is my dream.

Cool beans. Rightsizing a home to better fit the number of people in your household always feels good – less waste, more utility. 4,000 sqft is a lot! I’m assuming you two are child free or no?

I used to love skiing/snowboarding, but it got boring for me after the 15th year or so. And as I got older, I got more worried about getting hurt, so no longer wanted to do the launch ramps and obstacle courses. Sad.

But we still love to go up to our place in Palisades, Tahoe several times a year to ski, hike, and bike too. It’s a nice balance.

Very cool you have the Tahoe second home, that must be great! It’s nice you didn’t sell when the market tanked.

Some more context on our lifestyle/decision making process – we do have one child, which was really the reason we decided to speed up our decision to retire. Pre child I could get my exercise fix pre/post work and spend the whole weekend climbing or skiing. After the kiddo came everything changed very quickly and I was lucky to sneak in a quick run or gym session. I got out of shape quickly and my mental health took a beating in the process. I was not the best father or husband I could be because of this. I really needed this outlet in my life for everything to work.

The 4k city home was way too big, but purchased more as a solid investment in a growing suburb. Our current home is slightly too small, we really could use another 500-1000 sq ft, but the cost to make this change in my outrageously expensive ski town would double our mortgage. Homes have doubled and raw land/building costs have tripled since we purchased in 2019. We’ve learned to be content for the time being.

Our net worth is now around 3.3mm, so maybe it’s time to make the move, but I still get nervous about making a bad decision and getting “forced” back into the workforce. Such a first world problem, I know.

I don’t have the problem of getting bored skiing or doing these activities. I think I was around 80-90 days of resort and backcountry skiing this season, and it wasn’t even a particular good year. I guess my addictive personality, which made me successful at sales, has transitioned to my outdoor passions. I just can’t enough of it, the more the better, always training and planning the next adventure. The injuries of course are a concern; there’s been broken ribs, a torn meniscus and a separated shoulder in just the last three years. Part of the game I suppose.

Thanks for all you do. I have immense gratitude for the knowledge you’ve shared over the years.

You’ve already figured out something many people never do: health, time, and daily fulfillment matter just as much as financial optimization. A lot of high achievers spend decades building wealth only to realize later they sacrificed the lifestyle they actually wanted.

At a $3.3M net worth, the bigger risk honestly may not be “running out of money,” but delaying the life you clearly know makes you happier and healthier. Your description of skiing, training, and outdoor goals doesn’t sound like escapism — it sounds like genuine purpose and identity.

Also, being present, healthy, and mentally fulfilled is probably one of the best things you can give your child long term. Kids notice energy, patience, and engagement far more than square footage.

And honestly, 80-90 ski days a year sounds like you’re already living a version of success most people dream about.

Dude! Were you my instructor at the downhill mountain biking beginner course 2 summers ago in Utah? Because he and his wife had a similar story – they left high powered corporate careers, took their gains and moved to Park City and worked as ski and bike instructors (and I got the sense they did that for fun, and didn’t really need the money).

LOL! I feel seen.

We built the home we wanted on the property we wanted in the area we wanted. We went over budget but this will be the first and last home we build and the only one we raise our children in. It will be paid off still in our 40s when we finally “retire retire.”

It slowed down not working at all by about ten years but raising kids in an ideal house and environment is worth it.

Thank you for the post, very interesting and I can relate to it very much. I always aspired to fire early in my career and figured once I hit my number, I would solve for lifestyle and be with family. However, my life has gone in the complete opposite direction! Because I always prioritized savings and the desire to fire, we always kept our housing expenses and expenses, in general fairly modest in the context of our net worth and income. However, we recently moved out of Boston to our dream location and bought a home for just under $5M. My expenses are similar to the example you provided, but slightly more as we put down just under $2M and our taxes/insurance are more expensive than the example you provided. Our housing nut when you account for taxes, mortgage, taxes, and the various service providers is around $23,000 a month or $275Kish annually. Our non-housing burn is more “reasonable”

We are worth around $8Mish (only $1Mish is pre-tax) and make around $900K annually. While our income is not guaranteed, it is fairly predictable with the business we run, and we have quite a bit of visibility that the income should trend higher consistently, at least over the next four years.

My wife and I are in our early 40s and have three kids-ages 1, 5 and 9. Given our non-housing expenses are more modedt, We could certainly live off $325Kish (using a 4% withdraw rate) a year assuming we bought or rented a less ridiculous home. However, we don’t mind working, and the situation feels too good to walk away from the income, despite much preferring to wake up without work… I can’t even imagine what that feeling would be like as we have always worked as long as we’ve known each other. We love our lifestyle and while we probably spent way too much on housing relative to our income and net worth, figure I could always downsize or sell if something adverse happens.

Put another way, I suppose I am working and have the inherent stresses of work (less time with my kids) to support such a crazy housing nut. I just feel that if I’m going to work, housing is a great way to express that and indulge and I can’t really think about walking away from the income… As much as it probably makes sense.

It does feel good to work for something you can actually enjoy, that also takes care of your family, that’s for sure.

If you don’t feel the financial strain of a ~$5 Million house, don’t feel guilty not spending as much time with your kids, and enjoy work, then that’s great. You’ve gotta do you.

As a stay at home dad, I’ve talked to so many moms who felt too guilty working after their kids were born, so they stopped. There seems to be less guilt from the dads I talk to, but maybe it’s because they feel more pressure to earn.

I can’t believe that Cow Hollow home sold for 7+ million over ask. Say what?! People are crazy.

Anyway, lifestyle inflation is a real challenge that we all have to combat constantly. Our country is obsessed with consumerism and always pushing more, more, more. And yes I do believe home purchases are definitely part of that desire for more, bigger, and better.

listing prices in the Bay Area are generally grossly under what the seller will actually accept, so these stories about massive overbids is really just that. Lower prices means more eyeballs, and (supposedly) more bids. The vacuum of knowledge of what the seller will accept encourages people to bid a bit high vs the comps. The historic low supply for SFHs supports it – wouldn’t work so well for condos.